Investors set to shrug off APRA's 'clampdown'

Summary: Bank regulators have taken action to try to restrict the property investor market. Evidence as to the effect of these measures so far is conflicting. I'm not convinced that the housing market is about to top out as house price growth is not out of control over a longer time frame. Rate increases and tougher LVRs are unlikely to hit the bulk of the investor market and might have more impact for the minority of investors with lower net wealth. |

Key take-out: Cheap money will always find a home – it's just a question of where. |

Key beneficiaries: General investors. Category: Property investment. |

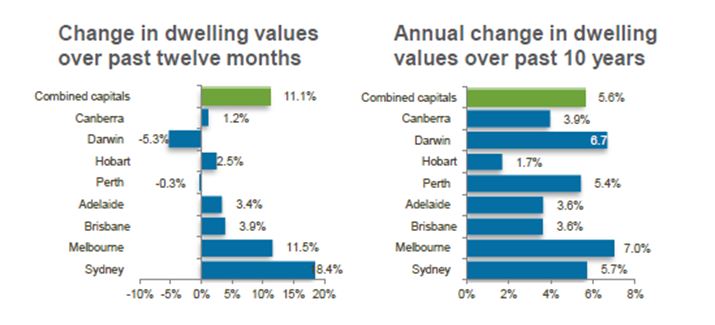

On the latest data provided by CoreLogic, house price growth continued to surge in Sydney and Melbourne, with capital growth of 18.4 per cent and 11.5 per cent respectively over the last year. Elsewhere, more modest gains were seen in in Brisbane and Adelaide, although on a total return basis – capital gain and rental returns – property has proven to be very attractive in most centres (see table 1 below).

Chart 1: House prices topping out?

Source: CoreLogic

Following a series of actions taken by regulators and the banks themselves, the question now is whether we're seeing the top of the market. More specifically whether recent rate increases on investor loans and changes to loan-value ratios will soften the market.

As a brief reminder, regulators have taken action to try to restrict the investor market. Now I wrote about this last year following moves by other regulators around the world to apply “macro prudential controls” on their markets. Our regulators have, so far, avoided outright macro prudential regulation (which I thought they would do), but what they have put in place is close enough.

So what APRA (the Australian prudential regulator) has done is flag to banks that investor lending growth that is ‘materially' above 10 per cent will be viewed as a risk indicator in considering whether further action should be taken. We don't know what ‘material' is, but lending growth to investors is already just above the 10 per cent mark.

Since then, and with a green light from the Reserve Bank, commercial banks have independently raised rates on new investor loans by between 0.27 per cent and 0.29 per cent. Many have also lowered the acceptable loan to valuation ratio (LVR) for new loan applications. Westpac has a cap of 80 per cent now, while other major banks have a cap at 90 per cent.

Evidence as to what, if any, impact these measures have had to date is conflicting. The Bureau of Statistics shows new loans to investors fell 3 per cent in May, before rate hikes came into the picture. Data from the Reserve Bank in contrast shows strong growth in total credit outstanding to investors in June. This expanded by 1 per cent in that month (or 10.7 per cent over the year) which is the strongest monthly increase since 2007.

Naturally, the true state of affairs will be revealed over coming months. I'm not yet convinced that there are grounds to think the housing market has, or is about to top out though. It just wouldn't make any sense.

First, policy makers have no desire – and more importantly no cause – to snuff the market out. System credit growth at 7.3 per cent is still very low (the average is nearly double that). Even credit growth at these 10 per cent levels is low.

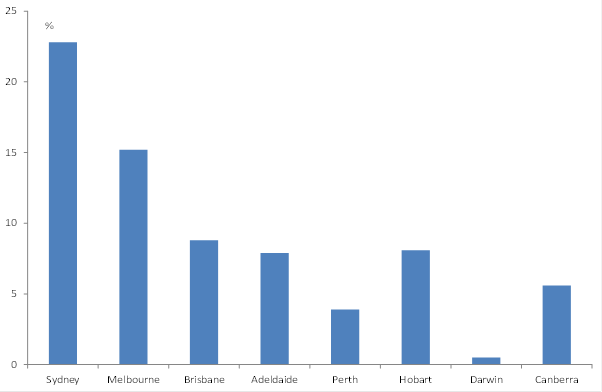

Second, house price growth, even in Sydney, is not out of control when viewed over a longer time frame. The debate in Australia is hysterical at the moment, perhaps not surprisingly when citizens are bombarded day in and day out about a housing price boom, or an affordability crisis – perception gets distorted. Chart 2 shows, however, that even in Sydney, house price growth has been reasonable. At an average annual rate of 5.7 per cent over the last 10 years, that's nothing to be alarmed about. It's markedly less than incomes growth – but it is an attractive capital return for an investor (total return between 9 and 10 per cent pa).

Chart 2: House price growth is not extreme over last decade – even in Sydney!

Source: CoreLogic

With that in mind the idea that there is a bubble is not reasonable in my view.

Against that backdrop, consider that lending rates for investors that are 0.27-0.29 per cent above what owner occupiers pay are still incredibly cheap. In most cases that would still leave a variable rate of interest sub 5 per cent – and maybe only just above on a fixed rate basis. These are still very attractive rates historically. Especially compared to the total rates of return available shown in chart 1.

Next, consider that LVRs to investors are already lower than to owner occupiers. Approximately 70 per cent of new loans written for investors are already for LVRs of 80 per cent or less. In any case, these LVR restrictions are voluntary – banks exercise a lot of discretion when approving a loan. High income earners or asset rich investors will likely still have few problems obtaining LVRs over 80 per cent – if needed. So for example, Westpac has stated that if two properties are offered as security (including an owner-occupied home), then higher LVRs can still be offered. There are ways around these rulings clearly.

This is important, because 80 per cent of investors are in the top income quintiles. They also tend to be older – about three-quarters are over the age of 40 on RBA data – and have higher net wealth.

That's why these rate increases and tougher LVRs are unlikely to hit the bulk of the investor market or if they do, maybe it is at the margin. Where they might have more impact is further down the chain – those 30 per cent of investors who are lower income earners or who have lower net wealth.

But a solid proportion of those lower income investors are actually looking to occupy (eventually). There has been a lot of press about how young first home buyers buy to rent first – and then occupy after a period of time (whether that's to take advantage of negative gearing or for lifestyle reasons).

For these people, higher interest rates and lower allowable LVRs on investment may simply lead to an earlier decision to occupy. In that segment, loans will simply be reclassified from investor to owner occupier. It's hard to know the exact proportion, though some surveys estimate 14 per cent of first time investors fit this category. In that instance, total system credit growth and the pressure on property prices will remain little changed.

All of this adds up to why I don't think recent measures (and those to come) will break the cycle. Money is just too cheap. What these measures might do to the extent they do anything is slow the cycle at the margin or redirect activity into cheaper areas (again only at the margin).

Even should other measures be put in place – and I suspect they will be – it's not even clear then that the cycle would be threatened. Instead activity would simply move across markets. So for instance you might see faster price growth in the middle tier market, or the one below that as people adjust their LVRs to price. Think of it as a trickle down. Those in the market for a $1 million investment in Sydney may lower their horizons to something in the $800,000 range – in Brisbane or elsewhere – just as an example. You get the idea.

In my opinion, cheap money will always find a home – it's just a question of where.