Household debt is a drag on the UK's recovery

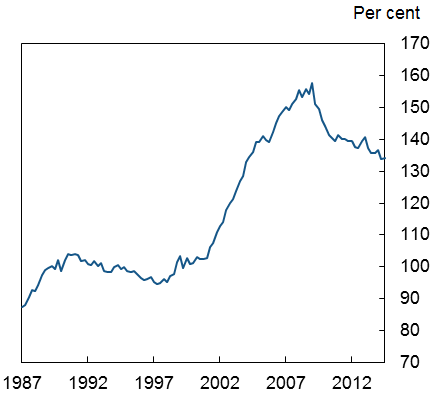

A major development in UK household balance sheets in the decade before the financial crisis was the build-up of household debt. By 2008, household debt had risen to 160 per cent of income from around 100 per cent a decade earlier (Figure 1), mostly accounted for by increases in mortgage debts.

Figure 1. UK household debt to income ratio*

Sources: ONS and authors calculations

*Total financial liabilities as a percentage of annualised total household resources.

Following methodological changes in the recent Blue Book, data used in the calculations are currently only published from 1997. Before 1997, the data are spliced with the previous vintage.

A number of US household level studies have found a link between high pre-crisis debt and weak consumption after the recent financial crisis. Dynan (2012) shows that US mortgagors with high loan-to-value (LTV) ratios pre-crisis subsequently experienced larger declines in spending (between 2007 and 2009); Baker (2013) finds that spending by highly indebted US households was more sensitive to income fluctuations than was the case for other households; and Mian et al. show that the decline in consumption following the crisis was greater in areas that had higher outstanding loan-to-value ratios prior to the Crisis. In Denmark, Andersen et al find similar evidence of a negative correlation between pre-crisis loan-to-value ratios and consumption during the Crisis. They also find that the highly indebted households who made larger adjustments in spending during the crisis had been consuming a greater share of their income before the crisis.

UK evidence

Using microdata from the Living Costs & Food Survey, we find a similar pattern for the UK of more indebted households making larger cuts in spending during the financial crisis.

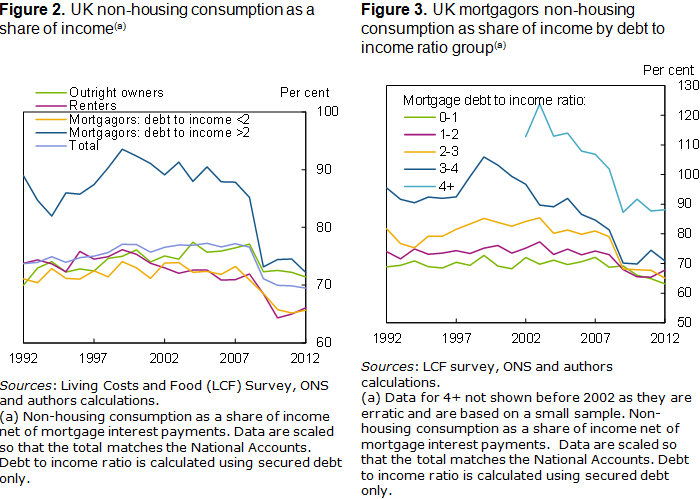

Figure 2 shows that households with mortgage debt to income ratios greater than 2 are estimated to have made larger-than-average reductions in spending relative to income after 2007. Disaggregating the data for mortgagors further, the largest adjustment in spending relative to income came, perhaps not surprisingly, among households with a mortgage debt to income ratio above 4 (Figure 3).

Regression analysis confirms that UK households with higher debt levels made larger adjustments in spending after 2007, even after controlling for other factors. We estimate an equation in which households' consumption is determined, in part, by their mortgage debt-to-income ratio and use it to estimate the impact of cuts in spending associated with debt on aggregate consumption.Those cuts in spending associated with debt are estimated to have reduced total private consumption by around 2 per cent after 2007 and at least until 2012, these effects had not unwound (Figure 4).

A larger adjustment in spending by indebted households after 2007 reflects an unwinding of faster growth in spending by this group before the Crisis. The econometric estimates suggest that indebted households added around 2.5 per cent to the level of aggregate private consumption between 1996 and 2003.

On average, that equates to a 0.35 percentage point contribution to annual consumption growth, which averaged approximately 4.5 per cent over that period. However, the effect of debt on the level of consumption falls back between 2003 and 2007, implying that it weighed modestly on growth during that period, despite debt continuing to rise rapidly.

Much of the strength in spending by highly indebted households before the financial crisis and the larger adjustment afterwards was in durables and non-essential categories of spending (Figure 5).

While there was still some fluctuation in spending on essential non-durable items, the estimated impact was smaller – consistent with the intuition that households cut back on non-essential spending first when they face financial pressure

It is difficult to prove that those more highly indebted households who made large cuts in spending after 2007 did so specifically because of their debts. However, survey evidence from the Bank of England/NMG Consulting survey -- which includes questions on households' attitudes to spending -- suggests that those spending cuts were driven by a combination of tighter credit conditions and increased concerns about ability to make future debt repayments, which is consistent with high indebtedness being at the heart of those spending patterns.

There are caveats to our analysis which need to be taken into account when interpreting the results.

The two biggest ones are:

First, the LCF Survey data that we use form a repeated cross-section, so we are not able to control for the pre-crisis debt level of households surveyed after the Crisis, only current debt.

Second, the measure of income used is net of mortgage interest payments, which means that reductions in mortgage rates after 2009 that lowered interest payments will have helped to cushion the squeeze in incomes for mortgagors.

Alternative econometric estimates that include a measure of income which is not measured net of interest, would imply a smaller (although not zero) impact on spending from debt than that described above.

New microdata evidence shows that highly indebted UK households made larger-than-average cuts in spending relative to income after 2007, although this only represents an unwinding of faster-than-average spending growth by this group before the crisis. This work adds to the growing body of international evidence which suggests that high levels of household indebtedness helped to increase the depth of the Great Recession.

High levels of household indebtedness might pose two risks to financial stability.

First, at higher levels of indebtedness, households may be more likely to encounter financial distress following negative shocks to income or interest rates, which could pose a direct risk to the banking system's resilience.

Second, highly indebted households might react to a shock by cutting spending sharply in order to maintain their mortgage payments.

That would have knock-on effects for the rest of the economy. For these reasons, the Bank of England's Financial Policy Committee made two policy recommendations actions at its June 2014 meeting to help insure against the risks from a marked loosening in underwriting conditions and a further significant rise in the number of highly indebted households.