Greece: Back from the brink

Summary: Greece and eurozone leaders say they have reached an agreement on a new debt deal following intense negotiations this weekend. However, the austerity measures still must be voted on by the Greek parliament on Wednesday. |

Key take-out: Even if the austerity measures aren't approved, the effect on the market will be limited when considering the other option that was proposed this weekend: An orchestrated, staged departure that would occur over many months. |

Key beneficiaries: General investors. Category: Economics and Investment Strategy. |

It looks like the EU and Greece have finally struck a deal. Certainly, the markets were reading this conclusion as your Eureka Report went into production late on Monday evening.

EU president Donald Tusk said Europe's leaders had reached a unanimous 86 billion Euro deal to offer Greece a third bailout …a move which will keep Greece in the Euro for at least the next three years.

For Australian investors the outstanding message here is not so much that Greece has done a deal... there are still key issues to be sorted out. Rather investors can now relax a little because whether Greece has finally got over the line or not (and there are still hurdles, a vote in the Greek parliament is just the beginning), the potential fallout from Greece has receded dramatically.

The most likely outcome now following conciliatory statements from both Tusk and the Greek Prime Minister Alex Tsiparas is weeks more of detailed negotiation – mostly involving the Euro's bailout fund, the European Stability Mechanism but slowly the issue should fade from the headlines.

As I've highlighted to readers in the past, austerity had to come for the Greeks whether they liked it or not, in the euro zone or outside of it.

There was simply no way they could avoid it. Not even by defaulting on their debt. That would simply have transformed the public debt crisis into a balance of payments crisis. Understanding this point is crucial to understanding why the Greek delegation finally relented to the demands of the EU and particularly of Germany.

Greece has to cut its spending. It's that simple. Unfortunately there are question marks over just how rational or competent the Tsipras government is.

What exact terms are in the final deal remains to be clarified. Moreover and on early reports there is still scope for the deal to collapse. Not least because of conflicting reports over what has been accepted.

Even if the deal does fall though, investors have gained a great deal of clarity – or certainty – on the Greek issue. Namely that deal or no deal, a Grexit, the way it has been defined in the market, is simply not going to happen.

You see, even if things sour again or for some reason fall through,Germany's proposal for a negotiated ‘temporary' exit for Greece (or a timeout if they don't accept reform measures) changes the matrix of possible scenarios. It effectively rules out the prospect for chaos that a Grexit may have unleashed.

Recall the Grexit scenario. Deal falters (for whatever reason), Greece runs out of cash, banks collapse and the Greek government is forced to issue a new currency and exit the Eurozone. Chaos ensues – market volatility spikes. At that point many argued that contagion into Italy, Spain Portugal, etc. was a high probability.

The other option: A graceful Greek exit

Why? Because think about what it is that the Europeans are offering if things regress again - its a graceful exit. This is critical, because leaving in an ordered way hadn't been an option for Greece before. It was simply austerity or an ungraceful exit - and the complete collapse of the Greek economy, social unrest and the removal of Syriza from government.

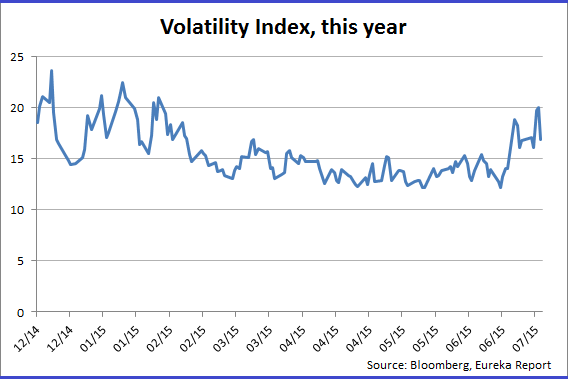

Naturally that would have led to some significant short-term volatility for the market as the fear gauge went through the roof.

What Germany's time out plan recognised, was that it's not so simple for a country to just issue a new currency. As the Chief Economist at the International Monetary Fund noted:

“The introduction of a new currency, and of redenomination of contracts, raises extremely complex legal and technical issues, and is likely to be associated with a further large decline in output. It may take a long time for the depreciation of the new currency to lead to a substantial turnaround.”

I've made this same point for a number of years – it was a key reason why I noted that a Grexit was such a low probability. This third, German option, changes things dramatically, because the worst case scenario is no longer a Grexit and chaos but an orderly, orchestrated departure that would occur over many months. As part of the package, Germany's Finance Minister proposes debt relief, while the EU President, Jean-Claude Junker, has said that humanitarian aid would also be on offer.

Combine that with additional liquidity measures from the European Central Bank and it's hard to see how it could be a major drama for the market. Uncertainty was always the fear but an orderly managed exit removes that uncertainty. It would also prevent any chance of political contagion as well.

The prospect of political upheaval is lessened because a managed Greek exit would serve as a stark warning to other political parties, in Spain or elsewhere, thinking of reneging on their agreements – that the only outcome of that is economic pain. Europe cannot be blackmailed into providing concession due to a fear of any particular member leaving the euro zone.

Hopefully this announced deal is the real thing - we'll find out over coming days. Then again it's not necessarily all that relevant for investors now. The issue always confronting investors was whether markets were going to be consistently affected by a country that accounts for about 0.5 per cent of the global economy. The answer is increasingly no. Already the market reaction has been comparatively mute, even in the face of a chaotic Grexit. Especially US markets. In the event of an orderly exit, markets would yawn.

All that said and done, things aren't looking like they'll get to that point. Assuming the Greek government is rational, a deal is the least harmful for Greek citizens.

What to watch from here

Deadlines keep moving so take these with a grain of salt but there are a few things investors need to watch. Firstly, the Greeks have been given until this Wednesday to pass measures to cut pensions and simplify (and broaden) the value added tax system.

Assuming they do that, Greece must pay the European Central Bank €3.5 billion by July 20 (next Monday). This new bailout agreement will allow them to do that. However, to get a new bailout the Greek parliament must agree to:

- Further privatisations - such as the electricity network, or failing that, establishing a €50 billion euro fund of assets to be held by an external independent fund;

- Obtaining approval from creditor nations for key budgetary or reform legislation, before passing through parliament.

No mean feat given the history of this sorry saga. As the German Chancellor Angela Merkel has often noted, trust in the Greek government is low and the Greek PM may not even last the week. Whatever unfolds in coming days, investors should take comfort in the steps that European leaders have taken to contain the crisis.