Gottliebsen's Week: Changes In Canberra and A Cautious Fed

Last Night

Dow Jones, down 1.74%

S&P 500, down 1.62%

Nasdaq, down 1.37%

Aust Dollar, US72c

Changes In Canberra

What a week it was. A new prime minister in Australia and a road map for global interest rates. So let's explore first the implications of the new prime minister and then look at how global interest rates are set to move.

There has been a lot said about the changes in Canberra but let me add my twist.

The Liberals are in two camps. The Christian right led by former prime minister Tony Abbott and the left led by Prime Minister Malcolm Turnbull. The Nationals are in the right wing camp so the majority of the Coalition is of the right but the left is in power.

That power grab came just as Abbott was very close to calling a snap election on the basis of the China-Australia Free Trade Agreement. If Turnbull was going to challenge he had to move quickly. Turnbull will need the Wisdom of Solomon to pull the Coalition together and avoid yet another government that is plagued by back biting and splits.

Assuming Turnbull resists the temptation to exploit his rise in the opinion polls and go for a quick election (he will certainly think about it) then his likely new treasurer Pentecostal Christian Scott Morrison will become one of the most powerful men in parliament. He is also one of the most talented.

There is no way Morrison will sit around for a year not doing much which was the plan of his predecessor Joe Hockey.

Everything will go on the table – the use of some superannuation savings by young people to buy houses, superannuation pension mode tax rates, pension entitlements via the assets test, negative gearing – the lot. GST will also be on the table but unless the states all agree it will be deferred until after the next election.

All this is happening against the backdrop of an unsustainable budget deficit and unless it is tackled it will cause Australia to lose its AAA credit rating in about five years and pay higher interest rates on the world stage.

So get set for a furious debate where Turnbull and Morrison will work with independent, Green and ALP senators to come to a package. (Turnbull has already phoned the eight so-called cross bench senators to start communication).

There will be plenty more commentaries on this subject as the year rolls on.

A Cautious Fed

Now to the US Federal Reserve.

I have been writing for many moons that while US interest rates would rise during 2015-16 the rate of increase would be much less than many in the market were forecasting. I took the decision by Federal Reserve chair Janet Yellen not to lift rates in September as confirmation of that base position.

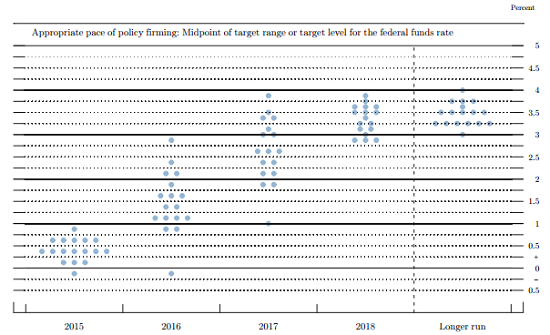

The Fed's famous dot plot: Each dot shows one member's prediction for interest rates. Source: US FOMC.

The US economy is recovering but not at a huge rate. In particular inflation remains low.

Lower commodity prices have played an important role in lowering inflation. And it is hard to see that changing especially given that Iran's production looks likely to re-join the oil market.

But there is also a fundamental change in developed countries' economies that is going to put a cork in interest rates for a long time.

The developments in technology are becoming much more significant and we are going to see large areas of white collar work forces replaced by computers over the next decade. The process has already started and it is hollowing out people on middle incomes in developed countries.

This fundamental change is going to keep the lid on prices because it will lower costs. As I have written before, as an example, most global banks are looking to halve their costs over the next decade or so, and this will spread to many industries. Companies are expecting to get their profit lifts more by cost reductions than by substantial increases in demand.

This adds up to continued low inflation which will limit interest rate increases.

There are other reasons why rates can't rise too far.

China is clearly in the midst of a substantial reorganisation and its economy might be in a worse shape than the official figures indicate. I think China will pull through but the ride could be bumpy in the next year or so.

If the US raises interest rates rise too far it will suck money out of emerging economies given this instability in China. Not only would it damage the global economy but would eventually affect demand for US products.

At the same time both Europe and Japan are anxious for the American dollar to rise so they can get trade advantages and assist their recovery. Higher US interest rates would definitely cause a big rise in the US dollar which would create great damage to many American corporations.

All these forces add up to the likelihood of fairly restrained US interest rate rises over the next two years. And this September decision not to increase rates underlines how cautious the Federal Reserve has become.

That means that those investing in interest bearing securities for the longer term are not going to be caught with substantial interest rate rises in the next year or two.

But the uncertainty in the environment that is causing interest rates to be curbed will lead to extreme volatility in equity markets. Indeed Janet Yellen underlined the risks in global economies as one of her reasons not to raise interest rates. Those risks will be translated into equity volatility and if the Chinese make mistakes all the elements are in place for a share market correction.

But meanwhile lower interest rates make the high yields on Australian equities look more attractive as I discussed last week (see: A fresh look at the hunt for yield, September 9).

Last Week

By Shane Oliver, AMP

Investment markets and key developments over the past week

· US, European and Australian shares rose over the last week, partly in anticipation of the Fed leaving interest rates on hold. Chinese shares fell though as official support for the market was tested and the Japanese share market also declined. Bond yields were flat to up and some commodity prices managed to rise helped by a weaker US dollar. The latter also saw the Australian dollar continue to bounce.

· Fed on hold and dovish. A few months back it was widely expected that the Fed would start to hike rates at its September meeting. In the interim though uncertainty about Chinese and emerging market growth along with continued uncertainty about US inflation has clearly got in the way and the Fed has rightly opted to leave rates on hold. More importantly though, while the Fed is still leaning towards a hike by year end, the commentary from the Fed was relatively dovish with the so called “dot plot” of Fed meeting participants' interest rate expectations being revised lower and the Fed clearly taking account of the risks posed by recent “global and financial developments” – read China and the emerging world - and the downside risks posed by this to US inflation. The clear message from the Fed is that it is aware of what is going on globally and is not going to do anything to threaten global growth at a time when US inflation is below target.

· While the Fed is likely comfortable that it has seen enough improvement regarding the jobs market it still seems to lack “confidence that inflation will move back to its 2 per cent objective over the medium term.” Although Fed chair Janet Yellen has indicated that the Fed's October meeting remains “live” for a rate hike, it's hard to see enough changing by then to justify lift off. As such December is more likely for a move but there is a reasonable risk that lift off could be pushed into 2016.

· In terms of market implications, the move by the Fed to leave rates on hold and indications it won't do anything to upset global growth are positive. However, a Fed rate hike is likely still out there somewhere and uncertainty around it will likely return at some point.

· Get ready for some noise out of Washington. The US budget and debt ceiling may hit the headlines again soon with Congress needed to pass budget funding for the new fiscal year that begins October 1. This and a desire by a group of extreme Republicans to tie budget funding to defunding Planned Parenthood could lead to the usual brinkmanship. The GOP leadership knows that it will end up getting blamed by the American people if it goes down the shutdown route again, and this is something they will likely be keen to avoid given the closeness to next year's elections. So our base case is a last minute deal but no shutdown. Similarly, expect some argy bargy around increasing the debt ceiling later this year (it looks like being reached around mid-November to early December) and again another last minute deal. However, budget funding and the debt ceiling could end up getting rolled in together again and the risk of some market impact is certainly there, so it's worth keeping an eye on.

· The change to Malcolm Turnbull as Australia's prime minister won't change the current Australian economic reality flowing from the end of the resources boom, but it does have the potential to help. At the very least we should see a short-term boost to confidence as he is a more popular political leader. But more importantly, we are likely to see a better articulation of Australia's economic challenges and what we can do to address them and greater flexibility in working to help guide reforms through Parliament. So while I won't be rushing to revise up economic growth forecasts and investment market return expectations the change does provide a bit of upside risk.

· Greece could make a brief return to the headlines in the week ahead. The latest Greek election on Sunday (September 20) is too close to call with the main parties Syriza and New Democracy running neck and neck. The outcome will be the same though as whoever gets the most votes will have to form a coalition with other pro-Europe parties, Potami and/or Pasok. But while there could be a bit of uncertainty until that is worked out it's unlikely that this will have a big market impact as both of these parties have signed up to Greece's third bailout program.

Major global economic events and implications

· US economic data remains mixed and suggests that growth is continuing to trend along around 2-2.5 per cent. Retail sales data was solid with upwards revisions to previous months and homebuilders' conditions were strong. But against this, housing starts fell and industrial production and manufacturing conditions were soft. While consumer spending is fine, the strong US dollar and an inventory correction looks to be weighting on manufacturing. Capacity utilisation is also running at sub-par levels which may be constraining business investment and pricing power. In terms of the latter, CPI inflation remained low in August with headline inflation remaining at 0.2 per cent year on year and core inflation at 1.8 per cent yoy. Were it not for housing costs the core inflation rate would be just 0.9 per cent yoy. There is clearly plenty of room for the Fed to continue delaying the interest rate lift off here.

· Eurozone industrial production and construction activity was a bit stronger than expected in July, but inflation for August fell to 0.1 per cent yoy and core inflation fell to 0.9 per cent yoy, both of which are well below target.

· Average Chinese property prices continued to rise in August with more cities now seeing gains. Chinese property related risks are continuing to recede.

Australian economic events and implications

· There was no sign in RBA Governor Stevens' parliamentary testimony that the RBA is moving towards another interest rate cut just yet – in fact he was “pretty content”. The Governor seemed reasonably comfortable that the economy is rebalancing and that the Australian dollar was around fundamentally justified levels. However, he has left plenty of wiggle room to ease again if needed with “growth not being as fast as we would like”, an acknowledgement of global risks and APRA's measures to slow lending to property investors doing their job. While the economy is not doing as badly as many seem to have expected (and still expect) my view remains that it is likely to need more help and this will come in the form of more interest rate cuts and a lower Australian dollar.

Next Week

By Craig James, CommSec

A quiet week in Australia

· A quiet week lies ahead in Australia with few standouts. But the latest resources forecasts from the Office of the Chief Economist are due by the end of the month together with the final Budget figures for 2014-15.

· In Australia, the week kicks off on Monday with the latest CommBank Business Sales index – a measure of economy-wide spending.

· On Tuesday the ANZ/Roy Morgan weekly consumer sentiment survey is released. Sentiment levels have softened in the past fortnight although that should hardly be a surprise. Currency, commodity and share markets have proved volatile and that has affected consumer sentiment – not just in Australia, but across the globe. In addition, the Aussie dollar has slumped, causing consumers to worry about the higher cost of overseas travel and dearer imported goods.

· Still, the survey to be released on Tuesday will be the first gauge of consumer feelings following the election of Prime Minister Turnbull.

· Also on Tuesday the Australian Bureau of Statistics (ABS) issues data on home prices – the “Residential Property Price Indexes” publication for the June quarter. Not only are the figures somewhat dated, but the CoreLogic RP Data figures are more comprehensive.

· On Thursday, the ABS releases the latest population figures – the publication “Australian Demographic Statistics” for March 2015. Annual population growth has slowed to a 3½ year low of 1.42 per cent, reducing the speed limit of the economy and sustainable investment returns.

· Also on Thursday, the ABS releases the Finance & Wealth publication for the June quarter. This publication includes an array of statistics including the foreign holdings of bonds and shares, household wealth and the financial asset composition of pension funds.

Overseas: US housing in focus

· The focus is on US housing data over the week while the results of the Greek election will filter through on Monday.

· In the US, the week kicks off on Monday with data on existing home sales. Economists expect that home sales eased by around 1.5 per cent in the month.

· On Tuesday, data on home prices for July is released. In June prices rose modestly, up just 0.2 per cent to stand 5.6 per cent higher than a year ago. So demand for homes is solid, but not excessive. Also on Tuesday weekly data on chain store sales is released together with the influential Richmond Federal Reserve survey.

· On Wednesday the so-called “flash” manufacturing gauges are released in the US, Europe and China. While the survey methodology and results are doubtful, unfortunately they are watched by a number of analysts and investors. The Chinese results will be especially scrutinised.

· Also in the US, the usual weekly data on housing lending is released on Wednesday.

· On Thursday the US Federal Reserve chair, Janet Yellen, delivers a speech while weekly data on claims for unemployment insurance is issued together with new home sales and durable goods orders.

· Economists expect that new home sales may have lifted by around 1.6 per cent in August but also forecast that a key measure of business spending – orders for durable, or long-lasting, goods – may have fallen by 1.8 per cent in the month.

· And on Friday the US economic growth figures for the June quarter are released. There are three iterations of the economic growth figures each quarter – the advance, preliminary and final estimates. The final estimates for the June quarter are expected to confirm that the US economy grew at a 3.7 per cent annualised rate – well above the “speed limit” of around 2.5 per cent after a weak – but weather-affected – March quarter result of 0.6 per cent growth.

· Also on Friday, the University of Michigan's consumer sentiment survey for September is issued. The preliminary reading was down sharply, a fall of 6.7 per cent to 85.7 in line with weaker sentiment readings in other parts of the globe.

Share markets, interest rates, commodities & currencies

· The Aussie dollar has fallen sharply over the past year. Measured in terms of currencies per US dollar, the Aussie dollar has recorded the 17th largest decline against the greenback of 120 currencies monitored, down 26.5 per cent. But for travellers, that means that there are 16 currencies that the Aussie has appreciated against including the Brazilian real, Norwegian krona and the NZ dollar. A year ago the Aussie dollar was at $NZ1.1050. Today the Aussie is worth $NZ1.1320. The Aussie has lifted 30 per cent against the Brazilian real and just over 1 per cent against the Norwegian krona over the past year.

· Over the last three months the links between the US Dow Jones index and the Australian ASX200 index have tightened. The measure of correlation, or R-squared ratio, stands at 0.82, where a ratio of 1.00 would indicate that the two indexes move perfectly together. Over 2015 as a whole, the R-squared stands at 0.62 whereas in 2014 the R-squared ratio was just 0.04.

· Over the same three-month period, the R-squared ratio between the Dow Jones and Japanese Nikkei was 0.85 and the ratio between the Dow and UK FTSE was 0.87, showing that the correction has been very much a global event.