Everything you need to know about "smart beta"

Summary: The median actively managed fund only beats the benchmark in five out of 15 years, research shows. But the idea that all investors should exclusively use index funds is an over-simplification. Smart beta providers argue that their indices are more efficient than traditional indices. Smart beta indices can be equally weighted to capture any gains from smaller stocks, or equally weighted by sector or risk profile, or weighted based on fundamentals. |

Key take-out: Smart beta products can be used to get exposure to smaller stocks and sectors, both as a source of additional returns and as a way to reduce risk through diversification. |

Key beneficiaries: General investors. Category: Shares. |

There is a huge gap between the real world needs of self-directed investors, and the investment products typically marketed to them. It's no wonder that a wave of innovation is now moving to displace traditional funds management technology, with the movement known as “smart beta” taking hold in major global markets, including Australia.

What is “smart beta”?

Smart beta funds use a range of techniques to select large portfolios of stocks into which the fund passively invests. Unlike traditional actively managed funds, which aim to beat their benchmark by picking stocks that outperform compared to the benchmark, smart beta funds are designed to exactly track a specific index. Smart beta indices are compiled based on specific characteristics which are argued to provide efficient investment outcomes, both compared to traditional indices as well as actively managed funds. For example, smart beta indices can be compiled based on:

- “Fundamentals” (eg factors like sales, cash flow, dividends and price to book value)

- Volatility (with variations based on choosing stocks with low volatility, or with a cap on the level of volatility for a stock to be included in the index)

- Equal weighting (in which stocks are equally weighted irrespective of their value, volatility or size)

Smart beta indices and products are springing up globally and some are already available in Australia – with most of them showing actual returns which are better than the majority of actively managed funds, and also in line with, or better than, traditional “first generation” index products.

What are the merits of index investing?

The range of opinion about post-GFC investing is huge, although one thing seems certain – the days of unthinking support for actively managed funds are over. That's due to a combination of factors like high costs, weak performance and tax inefficiency. Index investing is rapidly gaining popularity such that the question now really should be “What index should I invest into?”

Broad based indices like the S&P/ASX 200 traditionally were used to compare investment performance of actively managed funds. The S&P/ASX 200 is an index based on the market capitalisation of the components, with each stock's weighting based on the proportional size of the stock compared to the overall index. In turn, market capitalisation is measured by the number of shares on issue for each component stock, multiplied by the price at which that stock is trading. Additional rules apply to discount illiquid stocks where large slabs are untraded.

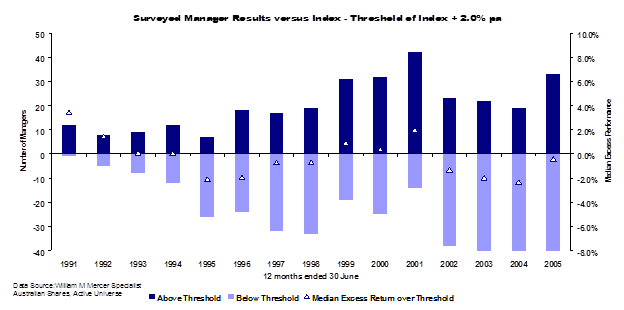

Table 1 below is a category killer which shows the relative underperformance of traditional actively managed funds compared to the S&P/ASX 200 index, with the median performing fund shown by a pyramid and with the horizontal line representing the index plus the median cost of accessing managed funds during the surveyed period.

Table 1: Performance of actively managed funds 1991 – 2005. Source: State Street Global Advisers

This type of analysis is typically used by passive index fund providers to suggest that the “best” way to invest is to replace actively managed funds with index tracking products. This is based on the observation that the median actively managed fund only beats the benchmark shown above in five out of 15 years.

The main problem for actively managed funds isn't that their managers are bad at picking stocks (some are better than others but most have their “time in the sun”). It's that they try to beat their benchmark by actively trading around it, and are forced sellers of stocks in market downturns. This problem was spotted by APRA in its seminal report on the traditional funds management industry released in 2009, which stated that:

“…the average (funds management) firm under-performed their net benchmark by an average of 0.9 per cent per year…This raises a doubt about the value of the active approach to risk management… The net under-performance of the average firm appears more pronounced in down markets.”

Of course, the idea that all investors should exclusively use index funds is really an over-simplification because it is also clear from this table that there are some actively managed funds that beat the index every year. Even so, these outperforming funds are in the minority and this outperformance is not very persistent, with less than one third of active funds still managing to beat the benchmark three years after they first do so.

The problem for traditional actively managed funds is that it's impossible to predict which of them will beat the index, or when that will happen… and it's normally too late to buy these well performing funds after they've had a good year.

Smart beta aims to build indices which improve on the performance of the traditional, “market cap weighted” index in an attempt to consistently beat that index and in doing so, provide more predictability and certainty in that outperformance than traditional actively managed funds.

Smart beta – what does the evidence show?

The idea of “beta” is that it measures the performance of an overall market or index, compared to the idea of “alpha” which is the measurement of outperformance over and above an index. Smart beta providers argue that their indices are more efficient than traditional indices (which as we saw are calculated based on the market capitalisation of component stocks) – and because traditional indices tend to beat actively managed funds most of the time, the promise of smart beta is powerful.

The first smart beta index was developed in 2005 by Research Affiliates in California, based on academic research by its founders Rob Arnott and Jason Hsu. They analysed the returns of an index calculated based on stock fundamentals rather than market capitalisation, arguing that expensive stocks dominate traditional indices and that therefore, holding a reduced exposure to them compared to stocks which are better value should provide the basis for better performance compared to the traditional index approach.

The Research Affiliates “Fundamental Index” rebalances the portfolio annually and does so based on analysis of the public accounts for stocks in the index. The rules on which the index are compiled are mechanical and don't allow for subjective analysis or “stock picking” – and funds which track this index are available in most developed markets (including in Australia via the Colonial First State “REAL Index” funds and the BetaShares FTSE/RAFI ETF (ASX Code: QOZ)).

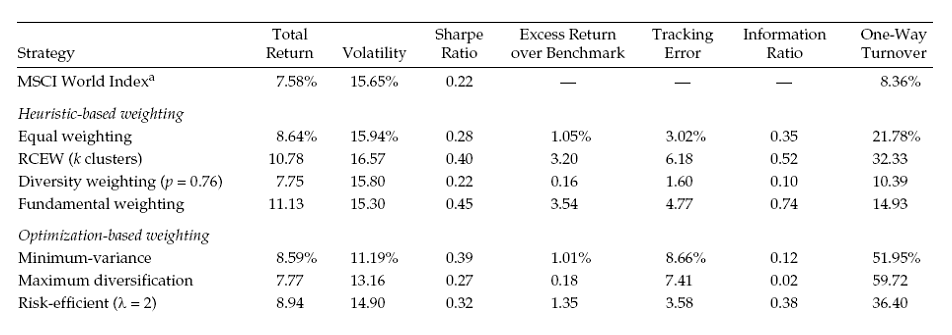

Because of the importance of this first wave of index innovation, academic studies have been quick to analyse the validity of the smart beta approach and to suggest newer ways of building smart indices. Table 2 below shows some performance data around the main types of smart beta indices (itemised in the “Strategy” column) – the key data to look at is the “Excess Return Over Benchmark.”

Table 2: Return Characteristics of Annually Rebalanced Global Strategies for 1000 stocks 1987-2009.

Source: Financial Analysts Journal, Sept/Oct 2011

In Table 2 the results use actual data and are broken into two categories. The “heuristic” category covers methods which are based on maximising actual returns, and the “optimisation” category covers methods which try to maximise returns at the same time as reducing risk.

Types of smart beta

No. 1: Equal weighting

Unlike market cap weighting where large stocks dominate and smaller stocks may each represent less than 1 per cent of the overall portfolio, equal weighting is just that – each component stock is equally weighted (by dollars invested) in the overall portfolio. The concept behind this is that smaller stocks may be less well researched and less invested in by large institutions (and hence potentially be better value) compared to larger stocks.

The prospect of outperformance of smaller stocks has been understood for decades, and the equal weight index idea is that by having a higher exposure to smaller stocks an investor has the prospect of gain as some of these (but in the real world, not all of them) are likely to perform significantly better than mature companies.

The downside of this concept is that it holds stocks irrespective of their financial performance or value, something that fundamental investors shun. Rebalancing costs will be higher in portfolios which hold a large number of relatively illiquid small stocks – and these costs can be a significant drag on net performance. Turnover in these indices is relatively high, shown above in Table 2 at 21.78 per cent pa compared to 8.36 per cent pa for the overall MSCI World index.

No 2: Risk cluster equal weighting

RCEW is an attempt to improve on the “lottery ticket” style of the equal weighting approach. Although the equal weighting approach is shown in Table 2 to beat the market cap index during the period by 1.07 per cent pa during the 22-year period 1987 – 2009, its logic is akin to buying lots of lottery tickets in the hope of holding the winner. The RCEW approach groups stocks by sector and by risk profile, and holds am equal weight of stocks from each sector or risk profile.

In Australia the Market Vectors “Australian Equal Weight” ETF is based on a risk category/equal weight approach. It holds 60 stocks drawn from the ASX 200 index and categorised into three groups, which are equally weighted. Its performance compared to the traditional market cap weighted S&P/ASX 200 index (as delivered by the State Street SPYDERS ETF (ASX Code: STW)) has been broadly in line as shown in Chart 1 below.

Chart 1: Performance of MVW compared to STW

Source: ASX

No. 3: Diversity weighting

This approach combines allocations based on market cap weighting along with an equal weighting approach. It does so to try to capture some of the better aspects of the market cap approach (ie, large and successful companies often have strong investment merit which underpins a proportionally larger allocation to them) with the logic of equal weighting (ie that newer/emerging companies may also warrant investment in proportions greater than would be dictated by their size). There are no funds or ETFs currently available in Australia which use the “diversity weighting” approach.

No. 4: Fundamental weighting

This is one of the most popular types of smart beta product in global markets. Research Affiliates compile “fundamental indices” for a number of countries with in excess of $170 billion currently invested into these indices. As noted above the logic behind them is that larger companies often do have greater investment merit than smaller companies but that allocating based on market cap (which in turn factors in the price of the stock) can mean that over-priced stocks represent an ever increasing part of the overall index.

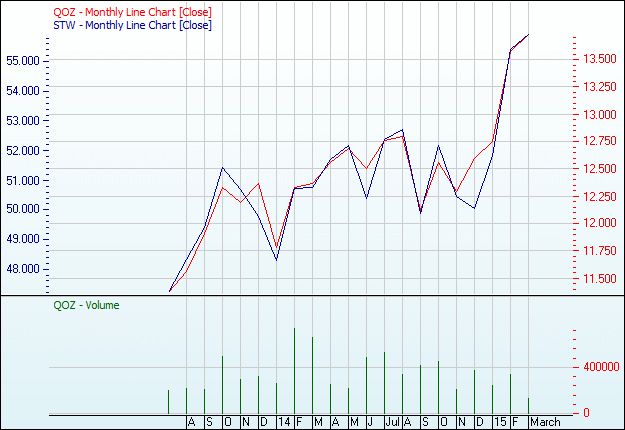

This has two drawbacks: it reduces relative yield and extends the payback period for the stock, and because expensive stocks often lose more value in market downturns, it can also detract from capital values over the longer term. In Australia the ASX listed ETF “QOZ” tracks the Research Affiliates “Fundamental Index.” Its performance compared to the traditional market cap weighted S&P/ASX 200 index (as delivered by the State Street SPYDERS ETF (ASX Code: STW)) has been broadly in line as shown in Chart 2 below.

Chart 2: Performance QOZ compared to STW

Source: ASX

Optimised portfolios: Minimum volatility

As noted above the simplicity of basic smart beta indices – whether based on equal weighting or fundamentals – is at the potential expense of ignoring the relevance of the riskiness of a stock. In turn, factors like volatility (ie how much a stock price moves over time) have been shown to do more than measure riskiness. In our Eureka Report article on the new wave of low volatility funds (see Introducing the volatility managers, February 4) we highlighted how using stock picking filters to target low volatility stocks has provided good returns compared to traditional market cap based indices, with the best return in Australia for this style being delivered by the StateStreet “Managed Volatility” fund (as shown in Table 3 below).

Table 3. SSgA Australian Managed Volatility Alpha Trust

Source: StateStreet

Using smart beta in your portfolio

Most self-directed investors prefer to own a concentrated portfolio of stocks, which are held for the long term. That can work well when quality stocks with growing earnings are purchased – unless the earnings capacity of a company becomes fundamentally impaired, there is little reason to sell a stock when this approach is used (at least, until “draw-down” when the retiree needs to sell stocks to cover living expenses).

Smart beta products can be used alongside the concentrated stock portfolio to give exposure to smaller stocks and sectors, both as a source of additional returns and as a way to reduce risk through diversification. Traditional market cap index products are normally a far better way to do this than by using traditional actively managed funds. Global data suggests smart beta should outperform traditional index products, although evidence to date is that the equally weighted and fundamental index products in Australia are performing more in line with traditional index products. More sophisticated products which target low volatility stocks seem more likely to show strong outperformance, and these could also be considered for holding alongside the direct portfolio of stocks.

One thing is certain – the menu of smart beta products offered in Australia is expanding and should continue to do so for some time.

Dr Tony Rumble provides asset consulting services to financial product providers and educational services to BetaShares Capital Limited, an ETF provider. The author does not receive any pecuniary benefit from the products reviewed. The comments published are not financial product recommendations and may not represent the views of Eureka Report. To the extent that it contains general advice it has been prepared without taking into account your objectives, financial situation or needs. Before acting on it you should consider its appropriateness, having regard to your objectives, financial situation and needs.