Every reason to believe the banks on dividends

Summary: Amid fears over bank dividends, senior bankers have been forced to defend their payouts. But payout ratios are not excessively high and evidence suggests earnings will lift. The economy is accelerating, confidence is rebounding and business lending is picking up. |

Key take-out: Investors should have every reason to believe the banks on dividends. Attacks on dividends to create uncertainty and get retail investors to sell out are a con job, in my opinion. |

Key beneficiaries: General investors. Category: Bank shares. |

Over the last week or so, senior bankers at ANZ and CBA have been forced to come out to defend their dividends, effectively stating that recent concerns over dividend stability were wrong.

It's a remarkable turn of events, though necessary given rampant fears over bank dividends. These fears have been a constant feature of the Aussie market for about a year now. Capital raisings, weaker profits, a slowing economy. You name it – many analysts don't need much of an excuse. The way I see it though, it's just another manifestation of an extreme and unjustified pessimism that has hovered over the sector since the GFC.

Not that shorting the banks has been a particularly profitable trade. Sure, any speculator who was lucky enough to sell-short at the peak has made money. Few would have made it that far though – it was a long ride on the way up.

For long-term investors, however, even that poor price performance over the last half-year or so hasn't really been a deterrent – dividends are just too good. This of course is why attacks on dividends have been ramped up: To create fear and uncertainty and to get retail investors to sell out. It's a con job in my opinion.

Yet the call repeatedly goes out that dividends are at risk, namely because payout ratios are too high to deal with slow growth and the ensuing lift in bad debts that will bring.

Now there are a few things we need to get out of the way first when discussing this topic. Firstly – it is a simple fact that payout ratios are neither excessively high nor looking particularly fragile (on average across the banks) unless you're expecting a deep recession. To suggest otherwise is factually incorrect. In each case (for the major banks), the payout ratio has been much higher – and often sustained at that higher level – for some years.

Then consider that for each of the banks, payout ratios are already down substantially from their post-GFC peaks. There is already a downtrend in place – yet in no instance has that reduction been driven by a cut to the dividend.

This is why, secondly, it is critical to distinguish between a benign drop in the payout ratio driven by earnings growth, and a drop driven by a cut to dividends. Not surprisingly, analysts looking for a reduction in payout ratios suggest the latter. In my view this isn't looking likely at all. The reduction in payout ratios instead will continue to be driven by earnings growth.

The next wave of lending growth

In the main, much of the analysis that points to a dividend cut rests on forecasts for very weak earnings growth. This is expected to be driven by a slowing economy, a lift in bad debts and ongoing regulatory pressure.

The evidence instead suggests earnings will lift.

Consider what came of past pessimism on the banks and the housing sector – nothing. Some years ago, readers may recall, the fear was that housing and credit growth (and so banks' earnings) would be weak because consumers were already heavily indebted. It was already a bubble some said.

Wrong.

So as the housing market and credit picked up, the argument changed. Analysts now said the housing market (credit and bank earnings) were at threat because because it was all investor-led.

Wrong.

The decline in investor lending has instead been offset by a surge in lending to owner occupiers. A fact I alerted readers to some time ago.

So when anyone argues that ‘'the slowing economy'' threatens bank earnings and dividends, my eyes roll.

For a start, all the evidence shows the economy is accelerating. In fact it's now official that the economic outlook is better. The RBA Board itself noted in the minutes to its November meeting (released yesterday) that “the prospects for an improvement in economic conditions had firmed a little over recent months”.

Yes, the RBA did revise growth and inflation figures ever so slightly lower. This didn't really change the core view though, because the bank's range of possible outcomes didn't really change. Growth could still be well above trend on those forecasts – or a bit below. As it is, the RBA reckons that: “Overall, the forecast for the Australian economy remained for growth to strengthen gradually over the next two years as the drag on GDP growth from falling mining investment waned and activity progressively shifted to non-mining sectors of the economy.”

That's not a bad outlook and it's consistent with another key development in the economy: The rebound in confidence. Consumer and business confidence is clearly on the up and this is important, because weak animal spirits have kept non-mining business investment low. This in turn has dampened credit growth. That this is changing will prove a boon to the banks.

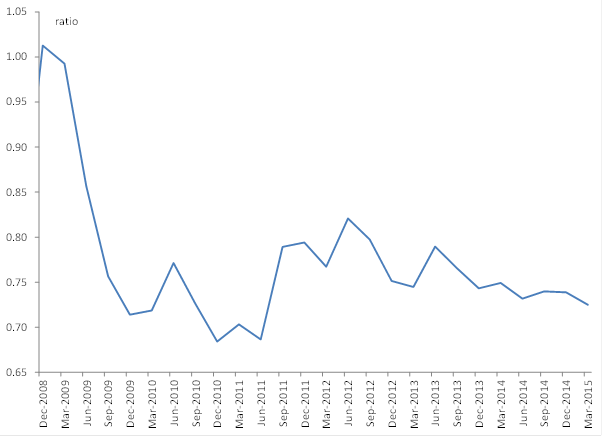

The scope for growth in business credit is enormous. We start from a position where corporate debt isn't particularly stretched. In fact it's below the average since the GFC, despite ultra-low rates.

Chart 1: Debt to equity ratio unchallenging

Now this ratio is currently above what we saw in the years building up to the GFC. Yet that pre-GFC low was driven by the stock market boom. If anything, we're seeing the opposite now. The weak equity market is inflating today's debt ratios.

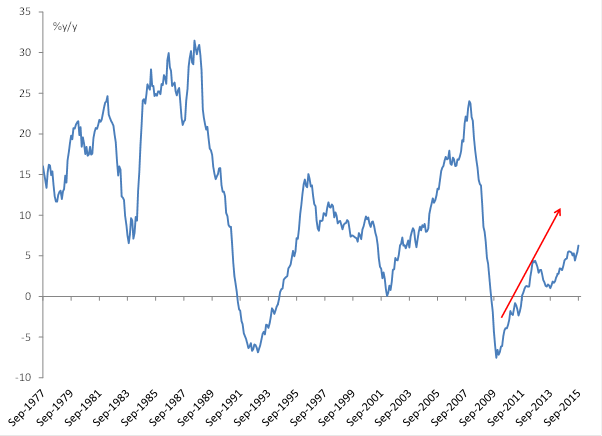

We're already seeing a marked pick-up in business lending by the way.

Chart 2: Business credit already on the up and set to get a boost

Chart 2 shows a solid rebound underway and in fact, just over the last year, credit growth to business has nearly doubled (up 1.7 times). So credit is already picking up and it will continue to do so next year as the economy accelerates and continues to rebalance. This will boost bank earnings, not weigh on them.

Otherwise, housing credit isn't going to decline. It'll keep rising as the unemployment rate continues to fall and as incomes and confidence lift further.

What about regulatory influence – the need to raise more capital and bad loans? Again, neither is likely to hurt bank earnings or result in a cut to dividends. Higher capital requirements haven't resulted in dividend cuts to date and banks instead were given the green light to lift margins.

Similarly, there is no reason to expect a jump in bad loan provisions. Firstly, because interest rates are expected to remain low for a very long time. Bad loans generally only rise as interest rates go up or the unemployment rate surges. We are years away from monetary policy coming close to a more neutral setting – and the unemployment rate is falling. In any case, loan quality is higher now than it was pre-GFC. Lower provisions for bad debts reflect that fact.

In short, investors should have every reason to believe the banks on dividends.