ER fund manager series: SGH ICE Fund

Summary: The SGH ICE fund has returned seven per cent annually since its inception in 2008, focusing on franchises and companies with intangible assets. Managers employ both fundamental and sentimental analysis with the aim of identifying strong opportunities. The fund looks to franchises for their strong cash flow and ability to hold a customer base even with price rises or changes to products. |

Key take-out: For investors looking for an Australian fund manager that invests outside of the ASX100 and major sectors of the local market, like mining and supermarkets, this could be a good opportunity for your overall portfolio. |

Key beneficiaries: General investors. Category: Managed funds. |

It's hard work finding quality fund managers that are experts in companies outside the largest Australian offerings. Those that do exist often generate returns that mirror the investors' preferred yardstick, the S&P/ASX 200. Consistently getting a margin above this measure might be desirable, but that's rarely a reality.

We have identified the SGH ICE fund (ETL0062AU) as being attractive from both the perspective of the investment thesis – owning companies with a franchise, or significant intangible assets – and the ability to turn ideas into attractive returns for investors.

We have previously introduced you to the concept of owning global brands with strong intangible assets – which are also often franchises – through the IFP Global Fund (read here: ER fund manager series: IFP Global Franchise Fund, January 20, 2016), which employs a similar concept on a global scale. However, there are some differences between them, particularly as this fund has the option to solely invest in Australia, or up to 30 per cent of the fund offshore.

What's so good about franchises?

With so many different methods for identifying companies to invest in, and ways of justifying a particular theme, it's important to understand the merits of owning franchises, or franchise-like businesses. A theme is a method to whittle down the investment universe before applying valuation criteria.

The appeal SGH ICE finds in franchises lies in the fact many have a sustainable competitive advantage. This could be brand recognition or a license – which are often referred to as intangibles – in combination with a firm footing in the market share stakes.

Another way to think about the dominance some franchise businesses can have is in how easily users of a brand's product or service can switch to a competitor. For example, AMP is in the top five holdings of the fund and it has a variety of business arms related to wealth management, where client money doesn't tend to move from one provider to another very often, or with ease when it does.

AMP financial planners can recommend AMP managed funds to clients, meaning that the money invested in financial products is relatively sticky because neither advisors nor clients will be in a rush to sell and switch into another fund.

Another appealing feature of a franchise is the ability to raise prices without upsetting the customer base too much. If users are captive and there are few alternatives, it makes passing cost increases to the business easy, protecting profit margins. This is a luxury not afforded to every business and is largely sector dependent.

Given franchises often have recurring inflows of cash, it can make predicting earnings more certain compared to businesses such as those that are vulnerable to changing commodity prices or the economic cycle. Having greater confidence over profitability can make the valuation of the business more reliable, helping identify ideal times to buy and sell.

Investment process

Identifying franchises is just the start. The fund also employs its proprietary ValueActive method to make investment selections. The method is a combination of fundamental analysis and sentimental analysis, with the end goal being to try to identify market inefficiencies.

Fundamental analysis focuses on the sales, profitability, assets and competitive position of a company. It's crunching the numbers and understanding the outlook for the business over the next one to three years.

Sentimental analysis is more qualitative and tries to gain an insight into how the wider market feels about a particular company. The aim is to gain an understanding of share price trends that can be exploited by picking the right time to buy and sell.

Using the ValueActive framework, the fund determines whether a company will make a worthwhile investment. In addition to this, stocks that make the portfolio must have an expected return that is likely to exceed the fund's investment objective over five to seven years.

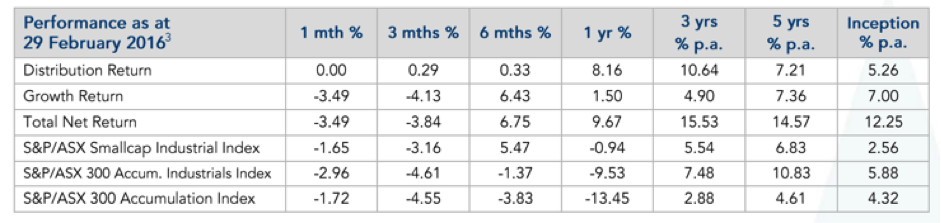

The performance

The strategy of focusing on franchises has led to impressive returns for the life of the fund, which has been running since February 2006.

While many investors favour bank shares for the lofty dividends on offer, the distribution return of the fund has been comparatively stronger than these shares. For argument's sake, looking at the ASX200 Financial Sector ETF (ASX: QFN), it hasn't paid a dividend yield of more than seven per cent and it has been an investable option since 2010.

By nature, franchise businesses tend to have high free cash flow – what's left after paying expenses – leaving plenty of cash to be shared with investors. Generating enough cash to pay out as dividends is a combination of recurrent, predictable revenue and business that can be scaled up in terms of size. For investors looking for income, this type of fund could be a viable option.

As nice as healthy cash payments are, capital growth (and preservation) is equally important. Over the past five years the fund has grown at an annual rate of a touch over seven per cent. In comparison, owning the index of the largest 300 companies has only achieved a 4.6 per cent growth rate.

The details

The SGH ICE Fund has $337m in funds under management. In comparison, some Australian share fund managers who invest in some of the biggest companies have in excess of a billion dollars under management.

But size is on the side of the fund. Once you start investing outside the ASX100, the market capitalisation of companies is around $2bn or less, making it difficult to effectively manage large amounts of money.

The size of the fund makes it nimble enough to buy the companies it wants to buy, without having idle money with nowhere to invest. Considering the size of the companies invested in, the fund will generally not own more than 10 per cent of issued capital in any one company. Having rules such as this in place helps the fund avoid any potential liquidity crunches whereby it owns a large amount of a security with a small market capitalisation, which can be difficult to sell.

The fund can own between 15 and 80 companies, allowing it the flexibility to pursue a concentrated approach - backing its best investment ideas or a range of options across the market. Currently the top five holdings make up around 15 per cent of the fund.

The fund can have up to 50 per cent of its assets in cash, which can be useful when the outlook for chosen companies over the coming year is unfavourable. It's also a way to protect investor capital and pick up some bargains if opportunities present.

A management fee of 1.18 per cent is what investors can expect to pay for an actively managed fund. The performance fee is 15.375 per cent and is only paid when the fund outperforms the S&P/ASX300.

Your portfolio

Australian managers that invest away from the largest companies based on market capitalisation complement the existing core portfolio holdings – often the major banks, miners and supermarket giants. Consequently the fund could suit investors looking for an Australian shares manager that specifically avoids these types of companies.

As always, when allocating a portion of your portfolio to a new fund, it should fit in with your overall desired exposure to Australian and international shares.