Ellerston and Platinum's Asian expansion

Summary: This week's article is on two new LIC IPOs closing shortly. Both are Asian focused and trying to achieve the same result of outperforming the MSCI AO Asia (ex-Japan). This is a wrap up of the offers and not model portfolio stocks. |

Key take-out: Investors who exercise patience will be rewarded. After listing costs both LICs are expected to come on with a NTA of approximately $0.98 – investors don't need to be the first one to the party on this occasion. |

Key beneficiaries: General investors. Category: LICs. |

Here are just a few of the new listed investment companies (LICs) that have come on to the market in the last 18 months: Argo Infrastructure Fund, Ellerston Global Investments, Acorn Capital, Contango Income Generator, Future Generations Fund, Future Generations Global, two names for NAOS Asset Management, a small cap offering from Glennon Capital, two global offerings from PM Capital, QV Equities and even Perpetual have thrown their hat in the ring with Perpetual Equity Investment Company.

Brokers' ears must be red raw from hammering the phones for these capital raisings and advisers' LIC-loving clients surely are tapped dry at this point. How much money is still “left on the sidelines” in term deposits in SMSF-land? Hopefully a little bit more.

Brokers and advisers are rolling up their sleeves and portfolio managers are doing their roadshows for two more LIC IPOs. Currently out on the hustings are the Packer-backed Ellerston Capital with Ellerston Asia Investments Limited (EAI) with its general offer set to close on August 28 and the latest offering from Kerr Neilson's Platinum Investment Management, Platinum Asia Investments Limited (PAI) which closes on September 7.

An initial look at the two offers could leave the sceptical thinking these are two more fund managers looking to tap into the current popularity of the LIC market. They are ticking the right boxes: LIC yes, international yes, Asia growth story, yes. It's the easy sell right now. Unlike pushing an Australian fund where investors will look at the holdings and second guess the manager on their banking exposure or the BHP holding, you're selling a story, a theme and you're selling access to Asian markets in which few Australians would be prepared to invest directly. They've been told they should have international exposure (in our LIC model international exposure was the first thing we went after) and they know Asia will play a vital role as far as returns go but managed funds aside how else do you gain exposure?

At present your LIC alternatives providing direct Asian exposure are thin on the ground. Your options stand at PM Capital Asian Opportunities Fund (PAF) which provides our model portfolio with its Asian coverage (see PM Capital Asian Opportunity Fund looks beyond China, July 27), there is the tightly held Dixon Advisory-run LIC of funds the Asian Masters Fund (AUF), and the embattled China focused AMP Capital China Growth Fund (AGF). To me there is a gap in the market for Asian focused LICs especially from established, respected names like Ellerston and Platinum.

Firstly let us look at the similarities between the two. Offerings will be sector unaware, region unaware and will also actively manage their currency exposure.

The two portfolio managers, Mary Manning for EAI and Joseph Lai for PAI, will also take a bottom up, fundamental stock picking approach with Manning including a macroeconomic and thematic element into her filtration process whereas Lai will not include that as a specific filter and says by selecting the best quality stocks from a fundamental view your portfolio will naturally be exposed to sectors and stocks that align with positive macroeconomic trends.

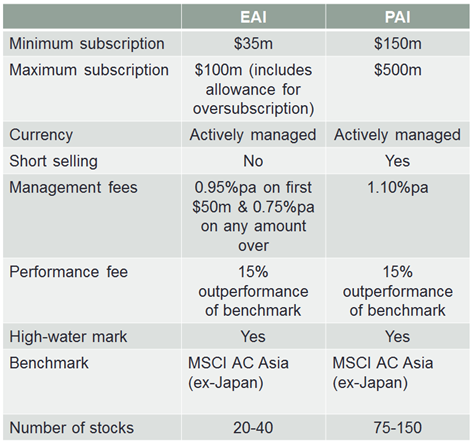

Fees

Another similarity is both LICs will have the same benchmark, the MSCI All Country (ex-Japan) ($A) and both will have the same performance fee applicable of 15 per cent of the outperformance percentage should they beat it.

Speaking of fees this is where the two start to differ. PAI will have a management fee of 1.10 per cent pa and EAI will have a fee of 0.95 per cent pa on the first $50 million in the portfolio and anything above that will have a fee of 0.75 per cent pa. Should EAI manage to hit their maximum subscription level of $100m (this is includes the oversubscription amount) the management fee would be 0.85 per cent pa. This gap would then naturally widen if EAI was able to continue to grow the balance of the portfolio. If everything else was equal (and that is a very big if) based on fees alone PAI will need to work harder to make up the 25 basis points difference.

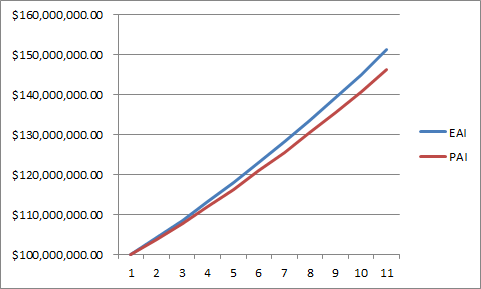

On a very simplistic level if you were to extrapolate the difference in fees, if both portfolios returned 5 per cent pa and charged no performance fees from a starting point of $100m over the course of 10 years the annualised difference in returns would be 0.36 per cent, as shown in the following chart:

Portfolio size

This leads us on to another point of difference between the two and I believe it is a critical one. PAI will dwarf EAI when it comes to the portfolio size. Mary Manning admitted when we spoke the other day: “We are not going for a headline grabbing figure with this raising”. The minimum shares issued for EAI will be 35m and its maximum if oversubscribed will be 100m. PAI on the other hand will have a minimum 150m and a maximum of 500m.

The MSCI AC Asia (ex-Japan) index has an average market capitalisation of $5,133 billion. Managing a portfolio of $50m or $500m, it is not unreasonable for you to think there will be an issue with liquidity. Where the issue with liquidity could appear, however, is when it comes to buying in and selling out of the LICs on the Australian market. Looking across the sector LICs with a market capitalisation of $100m or less have an average daily trade of approximately $13,000, compared to $210,000 in LICs above a market cap of $200m but below $500m. When recently speaking with a large cap LIC manager on the subject of portfolio size and the smaller IPOs that had taken place over the last 18 months they simply said when it comes to LICs, bigger is better.

Past returns

EAI will be a unique offering for Ellerston Capital as they do not currently offer straight out Asian exposure. They do have some Asian exposure in their global funds but as a portion of their total. Even though they currently search through those Asian markets for opportunities and portfolio manager Mary Manning has an extensive background living and investing in Asia, with Oaktree Capital (a US-based fund manager) and with Ellerston's emerging markets fund, it still does not make up for Ellerston not having a clear track record of this strategy you can point to. PAI on the other hand does have an Asian fund and this LIC is just an extension of that exact same team with the same portfolio manager in Lai.

The fund has been running since 2003 and has a history of beating its benchmark since inception by 6 per cent pa.

Since March 2003 Platinum's Asian fund run by Joseph Lai has return 16.6 per cent pa to unit holders net of fees. What they have done has worked in the past, but of course as always past performance is no indicator of future performance.

Portfolio construction

A significant difference between the two portfolios will be the number of stocks they will hold. EAI will be a more concentrated portfolio holding 20-40 stocks as opposed to PAI which will hold between 75-150.

With EAI you are looking a much more highly concentrated portfolio where they will focus on their best ideas weighted to how well each score on their conviction scorecard. The scorecard takes into consideration six key areas they are looking for: earnings per share growth, forward looking price target growth, the structure of the industry the business operates in, the management team, how well positioned the stock is within the already identified thematic trends the team see emerging and the company's environmental and social governance.

PAI will take a similar approach minus an initial screen on broad thematic trends in the region and will be looking for deep value stocks. These positions will generally be between 2-3 per cent weightings. It will be these that generate the real returns for the portfolio. The remaining stocks will consist of ideas either coming into the portfolio or exiting the portfolio.

Patience is the key

Looking at the offerings side by side it is hard to go past Platinum's option given the clear track record of the strategy and the team that has successfully deployed it. Additionally it does have size on its side. Both managers have shown the ability to keep their LICs at a tight trading range around their NTA as well. Both will have an options overhang - whether “loyalty option” or regular, options are options and if exercised will add to the size of the portfolios (and to management fees).

As always in the market investors who exercise a bit of patience will be rewarded. After listing costs are taken out both LICs are expected to come on with a NTA of approximately $0.98 (give or take pending on the size of the take up). And if we see some short term volatility there is every chance an investor could get the opportunity to pick them up at $0.95. This will give management of both portfolios a decent incentive to get the share price back up near the strike price of the options; it certainly will be in their best interest. I do not expect both portfolios to come out paying dividends of significance straight away as well as they will want to maintain their capital to keep the NTA nice and high to help the share price too.

When the dust has settled and options exercised it will come down to portfolio performance. Once again perhaps patience is best here, investors can sit back and keep track of the two LICs' announcements and read their commentary and see what investment approach resonates more. At the end of the day investors don't need to be the first one to the party on this occasion. The share price may run but these are long-term investments and in the meantime investors will at least sleep soundly.

To read about our Asia exposure in the model portfolio see: PM Capital Asian Opportunity Fund looks beyond China, July 27.