Don't expect a rate hike in 2015

Summary: It looks unlikely the US Federal Reserve will hike interest rates this year, despite comments from chair Janet Yellen to the contrary. The answers largely depend on the US and the nature of the slowdown that's occurring there, with the official view being that the weakness is temporary. However, recent data points suggest a more protracted slowing, which will become a source of angst for the market. |

Key take-out: While US growth may be moderating, it doesn't look sufficient to threaten underlying earnings growth and the equity market on a sustained basis. |

Key beneficiaries: General investors Category: Investment and portfolio strategy. |

What should we make of the Fed's apparent commitment to hike rates this year? I'm not sure that we can make too much of it to be honest. We've been here so many times before. That they should hike is clear. Yet once again there is reason enough for them to hold off should they choose – and, despite Fed chair Janet Yellen's comments, I suspect they will hold off.

The answers largely depend on the US, and the nature of the slowdown that's occurring. That a slowdown has occurred no one disputes; it's very clear in the data with March quarter GDP coming in at its weakest in a year at only 0.2 per cent. This is only a fraction of what is trend growth (2.4 per cent).

What isn't clear is the magnitude of said slowdown and how temporary it ends up being. The official view at the moment is that the weakness is temporary – weather induced, statistical noise even. Yet that is by no means the only view. Many analysts and even Fed voters argue that the flow of recent data points to a more protracted slowing. You see it's not just GDP that has slowed – nearly everything has of late. Have a look at the table below.

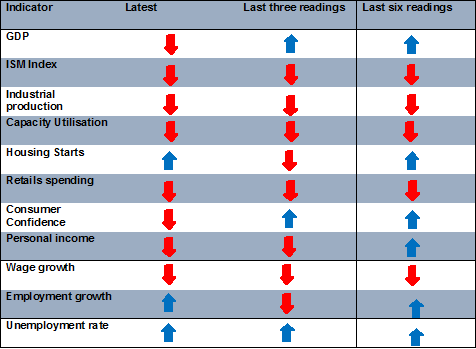

Table 1: The US is slowing

As you can see from the table, there are a lot of indicators that have weakened lately (red arrow) and not just necessarily on one read. In some instances we're talking about the last three or even six months of data – wages, industrial production and the ISM index in particular. That's a clear trend in place and, on the face of it, problematic.

Especially as that weak first-quarter result looks set to be followed by another weak quarter. Even the official numbers provided by the Atlanta Federal Reserve support that case. They reckon growth will be around 0.7 per cent annualised. With all that in mind, I don't doubt that the ‘slowdown' is set to become a source of angst for the market.

Indeed, while Yellen reiterated her confidence that the economy would strengthen, she must have known at the time of the speech that it was highly unlikely the Fed's 2015 growth forecasts would be met.

The Fed forecast growth of between 2.3 and 2.7 per cent for that year, down from an expectation of 2.7-3 per cent at the December meeting. Given the weak March quarter – and expectations that the June quarter will be similarly weak, we'd need to see extraordinary growth in the September and December quarters just for those forecasts to meet the lower bound growth expectation. That's not impossible but it is unlikely. What's more likely is that the Fed will revise down its growth forecasts at the next meeting.

So to my mind the economy has certainly slowed and this will impact the Fed's decision. I maintain my view that the Fed is unlikely hike rates in 2015, notwithstanding Janet Yellen's speech on Friday night reiterating a desire to do so.

Having said that, three things give me some confidence that, while the economy has slowed and the Fed won't hike, the magnitude of the slowdown isn't anything to worry about when it comes to the equity market – outside of possible short-term softness. The slowdown certainly isn't as large as suggested by GDP figures and we're not looking at a material change in momentum sufficient to impact corporate earnings.

Firstly, jobs growth remains strong and the unemployment rate is still falling. The pace of growth has slowed, but it's still going in the right direction.

Secondly, the ISM index, while it has declined in each month for the last six months – by a cumulative 11 per cent – is still at a level that shows the economy expanding. More to the point, both new orders and also production picked up in April.

The third reason is that the construction sector is likely to remain very supportive of growth.

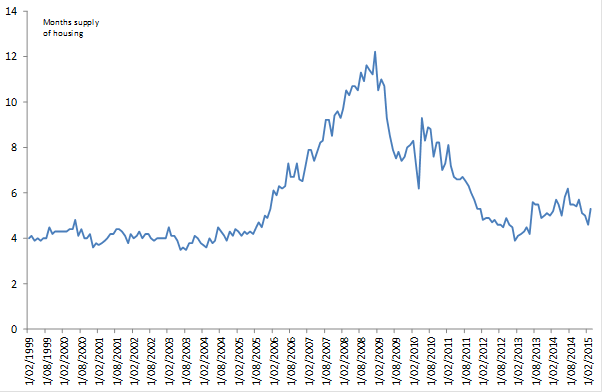

Chart 1: US housing stock

The chart above shows the current month's supply of housing available to hit the market. Admittedly, at 5.3 months of supply, the market doesn't look especially short – that's only just below average. Bear in mind though that this is a buffer that exists to support a still low sales environment. New home sales are recovering, and at a decent clip. But they are still very low historically. The market doesn't look very well supplied when you take an ongoing normalisation of housing sales into account.

These factors should rule out a significant slump in growth outcomes – but the economy probably has moved into a sub-trend period. That's not necessarily unusual by the way. Data is volatile and it bounces around; you get soft patches and periods of comparative strength. For instance, GDP growth averaged nearly 4 per cent in the final three quarters of 2014 – well above the average of 2.4 per cent.

Those kind of growth rates just aren't sustainable though, and I suspect all we are seeing now is something akin to a reversion to mean.

If that view is the correct one, then it could be that the recent turn of events amount to the perfect storm for investors. At a minimum, table 1 makes me more confident in my view that we won't see the Fed hike this year. At the very least they won't do anything until September, and then we'll see what the data flow is after that.

Similarly, the recent growth slump will convince Fed members that the US dollar is to high currently and a threat to the recovery. Concerns exist already and the Fed noted at the last meeting that the “value of the dollar had increased significantly since the middle of last year, and it was seen as likely to continue to be a factor restraining US net exports and economic growth for a time.”

While the unemployment rate is falling and that may support the case for rate hikes, Yellen's view is that the current employment rate doesn't capture the full slack in the labour market. This means she must think the non-accelerating inflation rate of unemployment (NAIRU) – the lowest unemployment rate you can get before inflation lifts – is lower than it would otherwise be. Consequently, Yellen wouldn't be worried if the unemployment rate falls further – especially if GDP is slowing.

With that in mind, I think the most likely outcome is that we're witnessing a new calm. Some of the wind is clearly coming out of the US sails, but it's not looking sufficient to threaten underlying earnings growth on a sustained basis. Firms are still hiring after all and the low stock of housing should ensure the construction cycle remains supportive of growth more broadly. That combination will continue to see US stocks supported on both an earnings and valuation basis.