Dividends: From insane to ludicrous

Summary: After recent price falls the cash and after tax yields on Australian shares are “insane” and a narrower mix of high yield shares even more “ludicrous”. |

Key take-out: High yields are compelling versus debt investments. Overall they mostly signal an oversold share market. Be aware of extra risks chasing a narrower mix of top yielding shares. |

Key beneficiaries: General investors. Category: Strategy. |

As at September 30 the forecast yield from the broad Australian share market is an “insane” 5 per cent cash and 7 per cent gross. The forecast yield from a smaller basket of high yield, but also blue chip companies is even a more “ludicrous” 7 and 9 per cent. Like Tesla cars and its “insane mode” and ludicrous mode” that accelerate cars to 100 km/hr in 3.2 and 2.8 seconds respectively, these are game changing numbers for a low interest rate world … or are they?

Here we revisit high yield equity investing in Australia including taking a special look into popular ETFs that some use to access these yields.

Insane and ludicrous yields

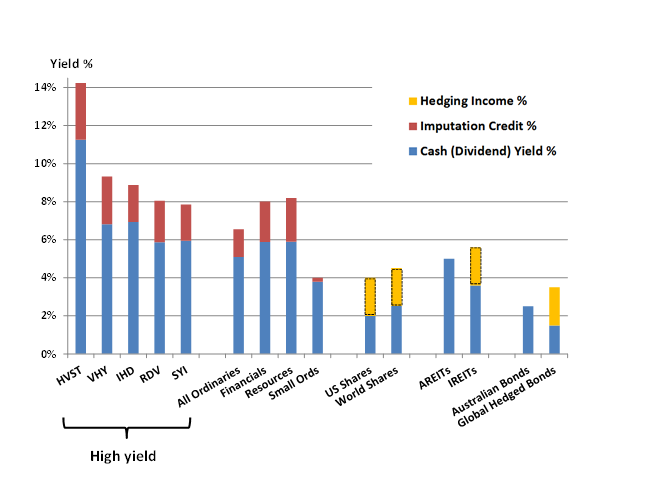

Figure 1 summarises the yield on offer from various high yield index-style funds and compares that to investing in the broader Australian market and other asset classes. These yields have been sourced from ETF fund factsheets published at September 30 and generally are calculated by dividing last year's income by the fund price at that time – though some like Vanguard are based on a forecast income. Also shown are accompanying 1) imputation credits and 2) income from any elected currency hedging (see Hedging's little extra, February 24, 2012).

Figure 1: Cash and after franking credit and optional hedging income yields from various equity and non-equity investments for Australian investors at 30 September 2015

Notice:

- The yield from the broader Australian share market is (or technically was at September 30 when the All Ordinaries was at a low 5,050) a very attractive 5 per cent plus 1.5 per cent tax credit, so 6.5 per cent for nil taxed investors – that's insane!

- This is an enormous premium to local deposits and bonds yielding only about 2.5 per cent, which you can blame on central banks (see It's time central bankers considered citizens, March 18).

- Australian investors earn more by buying through a fund, lower face value yielding foreign bonds, than same credit-rated local bonds. After being topped up by currency hedging income the net yield premium is about 1 per cent.

- The cash yield from offshore equities is about half that from local shares because of the imputation credit-driven bias of Australian companies to pay about two thirds of their profits out as dividends.

- Investors hungry for higher equity income can invest in four traditional high yield ETFs from Vanguard (ASX symbol: VHY), State Street (SYI), Russell (RDV) and BlackRock (IHD).

- These funds each follow the construction rules of four different index suppliers, which means for instance the proportion of high yielding financial stocks ranges from a capped low of 35 per cent (IHD) to a high of 50 per cent (SYI, RDV). Anything above one third worries me.

- Recently the likes of BHP, Rio and Woodside have turned up as top 10 holdings in high yield equity funds. It's assumed past and/or promised cash dividends will be paid, making this a high percentage yield on a collapsed share price. You can see in Figure 1 that Australian resource companies are now as high yielding as financials. I don't think that's sustainable (see The pitfalls of mining for income, September 21).

- The extra cash yield from investing in these four funds, which hold about 50 not 200 stocks, is about 1 per cent more and they also offer about 0.5 per cent more franking credits. According to finance theory, only the 0.5 per cent credit is extra total investment return and then only to nil taxed investors.

- Vanguard's VHY ETF has a 9 per cent forecast gross yield, meaning income alone should pay back your investment in 11 years. So whatever your shares are worth then is all bonus! You'll have to wait 40 years for your deposits and bonds to do the same. Both are ludicrous.

- Betashares HVST fund is a franked dividend harvesting machine. Every two months it actively remixes the portfolio looking for the next payday and by doing so grabs more income and franking credits than other more passive high yield ETFs. Because of the dividend run up effect, this machine also turns capital into income, which if not understood may lead you to believe this is all free money. You need to reinvest about half the income grabbed to expect the capital value of your holdings not to decline. The free ride from this fund is perhaps 0.7 per cent more franking credits (1 per cent net of its 0.3 per cent relatively higher ongoing fee). To avoid catastrophe targeting only 10-15 stocks at a time, the fund also uses futures to manage downside risk. This is a clever but more complicated fund.

- After inflated valuations the rent from local property trusts is a relatively unspectacular 5 per cent (and 3.5 per cent from offshore property if unhedged). Still local commercial property offers about double after costs the yield from residential property. Local AREITs offer some tax deferral benefits but that's not relevant for nil taxed investors.

“Yield off”

Early in 2014 I encouraged readers to be careful chasing pricey, higher yield investments and instead consider making your own dividends (see Homemade dividends, April 14, 2014). I wrote recently I thought April Fools' Day was the peak in the yield trade (see From tailwinds to headwinds but I'm still in this market, August 12).

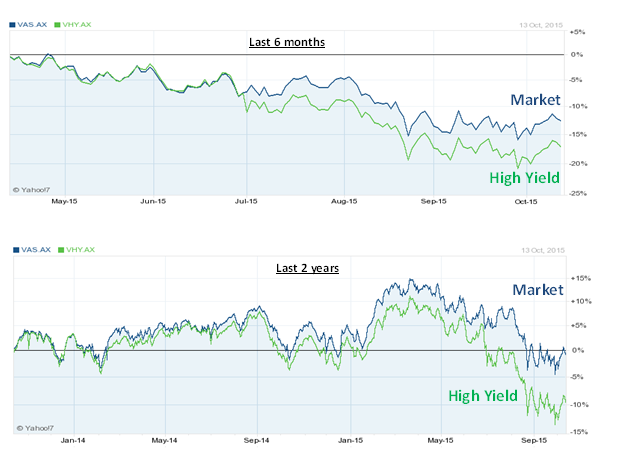

Figure 2 shows the relative price change investing in the broader Australian share market and a narrower high yield mix – based on the price of respective ETFs VAS (Vanguard Australian Shares) and VHY (Vanguard High Yield). Over the six months since April, high yield shares fell up to 20 per cent versus only 15 per cent for the broader market. An investor in the broader market over the last two years is square on a price basis versus losing 10 per cent chasing higher yield. In the latter case the extra 1 - 1.5 per cent income didn't compensate. You had to have been investing in high yield shares for more than 2.5 years to have earned a higher combined price and income return.

Figure 2: Change in price of Australian shares making up the broader market and a narrower higher yield mix over the last 6 months (above) and 2 years (below) based on VAS and VHY ETF prices.

“Yield on”?

After greater price falls in high yield stocks, the question now is whether they deserve specially reinvesting in? The answer depends on whether these yields are sustainable, which I'm inclined to believe they probably are not, but there is a buffer to fall before this becomes a dumb idea.

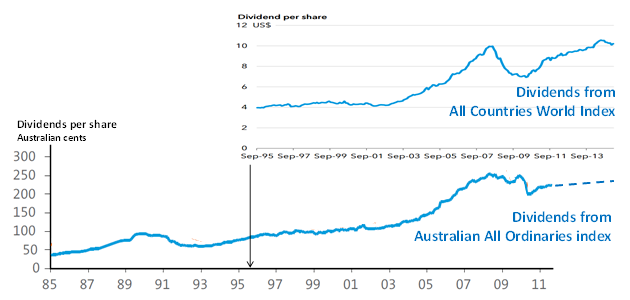

Figure 3 is an old favourite chart I borrowed from AMP chief economist Shane Oliver showing the relative stability of the dividend income of the Australian share market over time. When looked at on a dollar/cents basis it has been pretty stable, more so than share prices and deposit and bond income. I use this slide mainly as a “crutch” with some overly cautious investors to think about holding a little more equities. Please don't you overuse it for that purpose!

I've superimposed the same information for the global stock market since September 1995. These charts cover the GFC and for Australia, the 1993 recession. Those periods are a pretty good test of how companies might cut dividends in a crisis and how long they might take to recover. History suggests investors should expect cash dividends to fall about 40 per cent and take five years to return to their original level. They also show they could otherwise stay flat for up to 10 years.

Figure 3: Cash dividend yields in cents/dollars from the local (since 1985) and world (since 1995) stock market indices. Source: Thomson Financial, AMP Capital Investors (All Ordinaries) and Capital Group (MSCI AWI)

A 40 per cent fall off in broad market dividends and perhaps a 50 per cent fall off in more stretched high dividend companies income is not entirely unexpected for various reasons: i) dividend payout ratios locally are at record highs above 70 per cent, ii) prospects for an Australian recession that could match that of 1993, iii) observations that many companies are raising capital while at the same time promising to pay increasing dividends (Westpac, Origin) and iv) others are promising to pay dividends double that of broker forecast profits (BHP). In the absence of a recession maybe planning equity income yields to fall about 20 per cent would be prudent.

The irony is that even if a 5 or 6 per cent cash yield (for a broader or high yield mix respectively) falls to 3 per cent this is still more than deposits and the bond market promise to pay you over the next five years.

So if you can stomach share prices falling 30-50 per cent and recovering also in five years, can you conclude you're better off equity investing?

No. High yield or broad market share investing is not a substitute for owning defensive debt investments. The latter exist to help you sleep at night, pay your pension when you don't want to sell shares and buy into the share market when everyone else panics (I call that “panic buying”).

I think high yields are mostly a sign of reduced share prices and contribute to a buy signal for those underweight shares. The last two years have demonstrated that you don't need to target higher yield shares for higher total return. Doing so really only favours nil taxed investors with an extra 0.5 per cent more franking credits. Chasing higher yield investments also comes at the expense of diversification – in some cases loading way too much up on financial stocks and strangely now resource companies again.

In summary, when contemplating chasing higher dividend shares be careful as insane capital management practices are being driven by ludicrously low interest rates and money printing.

Dr Doug Turek is Managing Director of independently-owned family wealth advisory and money management firm Professional Wealth.

Please note all financial products discussed here are for educational purposes and do not constitute an investment recommendation. Please do your own research and/or speak to a licensed financial advisor before choosing to invest.

Eureka Report income analyst James Samson adds:

As I mentioned recently (see Bank dividend risks: What to do, October 19), the sustainability of bank dividends pose some real concern, and should be under scrutiny by every investor.

Additionally, as Doug Turek points out here, a market weighted to about 47 per cent in the financial sector lacks diversification. In fact it is downright dangerously concentrated.

A few weeks ago (see The pitfalls of mining for income, September 21), I also highlighted that resources stocks are extremely difficult to justify as investments for the purposes of income generation, and investors should be very cautious of dividend traps (think BHP and WPL).

Despite these easy, common sense, conclusions on banks and resources stocks, the phenomenon we are witnessing in Australia at the moment is that the banks and major resources stocks are being priced on yield. The earnings outlook is nothing short of benign in most corners of the market, so growth is not helping share prices. For the opportunistic, this phenomenon (of the biggest stocks on the market pricing on yield) has led to some other, smaller, higher growth stocks being priced in a similar fashion – potentially ignoring the relatively brighter outlook.

This is where income investors should focus their attention in order to take advantage of the historical highs we are seeing in the differential between bond and equity yield. This is where investors can take away a 6 per cent plus gross yield and sleep at night.

And this is the sector or sub sector of the market – detailed in my Income First model portfolio here – that is likely to outperform as the larger cap yield plays such as the banks come under the pressures of lower profit growth, regulatory squeeze and stretched payout ratios.