China does not have a debt crisis

Summary: China's debt to GDP ratio has spiked but government debt in the country is actually fine. The real concern when it comes to Chinese debt is in the non-financial sector, mainly state-owned enterprises. There is a small pocket of highly indebted firms and this is what seems to have caused so much angst. |

Key take-out: If there was a large drop off in profitability, many of these companies would face significant financial distress. Luckily, China doesn't face that. Even in a disaster scenario, any downturn could be easily dealt with given the very strong fiscal position of China's government. |

Key beneficiaries: General investors. Category: Economy. |

As global markets, including China's listed markets, show some signs of stabilisation after a sharp mid-year correction the residual question on investors' minds – especially in Australia – is: How bad is China really?

I've argued on numerous occasions that an $18 trillion economy (PPP basis) slowing from double digits to high single digits is a very positive development for the world. It would be very disruptive to global growth to see China continue rising at 10-14 per cent rates. That fact, while gaining significant traction lately, still doesn't stop people getting anxious (see also Byron Wien's piece today, which suggests investors have over-reacted to China's softening: Unfazed by the turmoil, September 9).

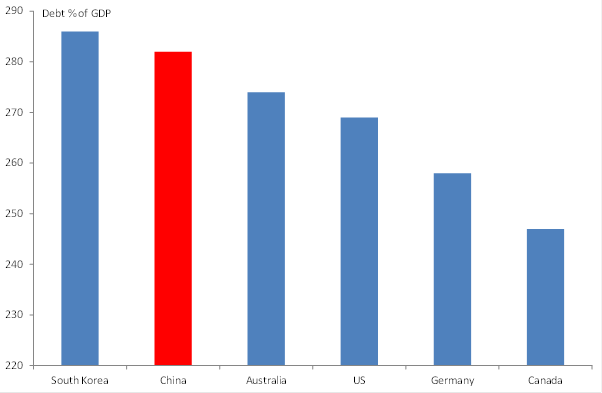

Debt seems to be the lingering issue and the worry is that China is at risk of some sort of financial crisis because of this debt burden. On McKinsey & Company figures, China has had one of the largest increases in debt in the world since 2007. An increase of about 80 per cent of GDP. So as it stands, China's debt to GDP ratio has spiked to 282 per cent of GDP. As many like to point out, that's bigger than Australia's and that of the US.

Chart 1: China debt to GDP

Source: Eureka Report, McKinsey & Company

Public debt including local government finance is fine

Within that huge figure, it appears that government debt, including local government, is actually fine. As the International Monetary Fund notes: “From a cross-country perspective, China's debt position is still comfortable”. So on figures provided by the International Monetary Fund (IMF), total government debt is around 55 per cent of GDP.

Now this figure includes local government debt – including off balance sheet items and ‘local government financing vehicles'. These are investment vehicles set up by local government authorities, typically to fund infrastructure investment. That 55 per cent figure includes the lot (though not state-owned enterprises, which I discuss below) and debt here is very low. For comparison, in the G20 advanced economies general government debt by itself – not necessarily including state and local entities – is about 111 per cent of GDP.

As you can see there is no comparison when it comes to public debt. China simply does not have a problem.

That's not to forget that when it comes to an analysis of China's public debt, it should be conducted net of foreign exchange reserves. This is because much of the central government debt on issue is actually tied up to the level of reserves. Why? To mop up – or sterilise – foreign exchange transitions. This is done by issuing debt to suck money out of the system that would otherwise be floating around to absorb foreign exchange inflows. So when we exclude the debt related to reserves, China's public debt position looks even less threatening at maybe 20 per cent or so of GDP.

Outside of the public sector, household debt too is very low at about 38 per cent of GDP on McKinsey figures, which compares favourably to most western nations and certainly isn't anywhere close to crisis levels.

The ‘corporate' sector debt explosion

The real concern when it comes to Chinese debt isn't in the household or government (including local government) sectors. Nor is anyone concerned about gearing in the financial sector. China's banks hold comparatively low gearing levels as well. Realistically, it's in the non-financial sector – state-owned enterprises in the main – where most of the concern is. It's true enough that in this space debt has ballooned. In fact on IMF and McKinsey estimates, corporate debt is roughly 125 per cent of GDP, or nearly two-thirds of the national total.

The problem with just looking at corporate debt as a percentage of GDP though, is that it doesn't really tell us very much. It gives an incomplete picture. The IMF instead uses a leverage ratio that compares corporate debt (total liabilities) to common equity as a kind of debt to equity ratio (used given data limitations). What they find is that the median leverage ratio for private firms has declined sharply, (from 125 per cent to 55 per cent) while for state-owned enterprises the ratio has been steady at around 110 per cent over recent years.

What the IMF found was that “while leverage on average is not high, there is a fat tail of highly leveraged firms accounting for a significant share of total corporate debt, mainly concentrated in the real estate and construction sector.”

So there is a small pocket of highly indebted firms and this is what seems to have caused so much angst.

Naturally enough, if there was some kind of interest rate spike or a large drop off in profitability, many of these companies would face significant financial distress. Luckily, China doesn't face that. Nominal GDP is rising at rates close to 10 per cent, real GDP at 7 per cent or more – per capita incomes are surging, not falling. That said, the property cycle already looks to be turning and even at its worst, didn't even come close to a disaster or ‘severe downturn' type scenario. Interest rates are otherwise only heading down. They are certainly not going to spike higher.

Yet even in that disaster scenario, and given the very strong fiscal position of China's government, any downturn could be easily dealt with. Especially given the very concentrated nature of the debt. At worst, they could print money like the US, Europe, Britain and Japan.

Don't forget, and as I've noted before when talking about the European debt crisis, public debt can't be looked at in isolation. It's only one side of the balance sheet and is meaningless without considering a nation's asset position. In China's case, these assets are considerable. In addition to the sizeable foreign exchange reserves discussed above, remember that the government has large equity holdings in China's corporate sector. That includes banks and most companies that are listed on the Chinese stock exchange. That's not to forget land, state-owned pensions funds, natural resources and the like – nor the fact that national savings stand just under 50 per cent of GDP in any case. All up we are looking at assets that are many multiples of GDP.

External debt is otherwise very low at around 8 per cent of GDP and according to the IMF nearly half of that is related to short-term trade credit. So what debt Chinese governments and corporates do hold, is to domestic lenders, who are, once again, all state-owned.

The fact is that China neither has a debt crisis, nor a significant debt problem nor anything that could be regarded as a broad-based debt issue. They're not even close. There are some sectors – construction and real estate – that have accumulated large debts but look nowhere near to having solvency or liquidity issues. In any case, these are largely state-owned enterprises anyway, borrowing money from state-owned banks who have low leverage and a huge asset base. The state is otherwise holding very little debt and has a very large and liquid asset base itself.