Cautious investors beware the Parable of the Talents

Summary: Business and share investment is about growth and innovation and at some point companies that just sit on their pile and cut costs fall out of favour. |

Key take-out: When a board is prepared to adopt a growth strategy and it has the talents to market its plans to shareholders, it can be rewarded with a very high share premium. |

Key beneficiaries: General investors. Category: Shares. |

Global markets, and indeed some local chief executives and boards, remind me of the fearful servant in the Parable of the Talents.

Those that have read the Bible remember that the fearful servant was given money and buried it in the ground because he was frightened what his master might do to him if he lost it. And so in the global bond market the US 10-year bond rate this week reached 1.54 per cent as fearful money managers reckoned that US bonds were where the least amount of money would be lost when interest rates start to rise.

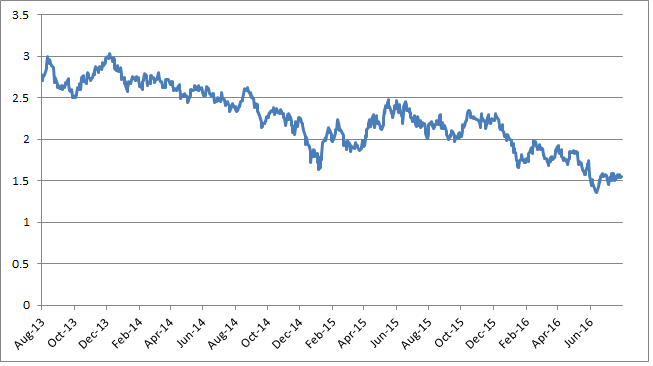

Chart 1: Approaching zero ... US 10-year bond yield (%)

Source: Bloomberg, Eureka Report

Similarly, institutions in Europe are burying their money in bonds and other securities that have a negative yield, again fearful of what is ahead. In a strange way many chief executives adopt similar strategies to the money managers. So today I want to look more closely at both these institutional and corporate strategies via a look at SEEK, and then give you a ray of hope as to what is happening in the US via the experiences of BlueScope.

There is a sidebar to the cash investment strategies. Burying money in the ground is in fact a risky strategy – apart from inflation, people can steal it. And in the modern world investors who, out of ignorance, often take that risk are those that invest in cash that has a description to it – usually “enhanced". The traders 'enhance' the return by taking risks. If you are worried about a financial calamity be careful how much money you have in 'enhanced cash' – or at least ask the institution what they are doing to enhance the cash.

Corporate priorities: Cost-cutting vs growth

Back to corporations. Today there is very little emphasis on growth and in most companies it is all about trying to lift profits via cost cutting. By contrast when a board is prepared to adopt a growth strategy and it has the talents to market its plans to shareholders, it can be rewarded with a very high share premium (a similar story to the other characters of the parable!).

We all know why so many money managers are scared about what might happen when America lifts rates – it will suck money out of the rest of the world and increase the American dollar. Accordingly they are prepared to take a token rate of interest in 10-year bonds hoping to make their money on the currency, or at least not lose it. The global fears extend beyond the US interest rates to the Chinese and European economies, Italian banks and a variety of other potentially scary situations.

I want to add one which I believe is at the back of the mind of many global institutions, but nobody talks about it.

Ten to 15 years ago America was the pre-eminent military power in the world. No one dared challenge the Americans, not only because of their actual superiority but their presumed superiority and the Americans' preparedness to use that superiority if necessary. But in the last 10-15 years America has not invested sufficiently in its military technology and where it has done so it has made fundamental mistakes. The most obvious mistake is the disastrous Joint Strike Fighter but there are a series of other equipment developments that have not matched either expectations or the capabilities developed by China and Russia.

So, suddenly, the world is much less frightened of the US and we see Vladimir Putin becoming more aggressive in Ukraine and Eastern Europe. Some of the Baltic States are petrified that he will invade in 2017, which would destroy NATO because it is unlikely that it would or could retaliate. Similarly, China feels safe to take control of most of the South China Sea and even North Korea is waving its fist at the perceived weakness of the Americans.

In 2017 the new president of the US will soon discover that the Americans have slipped back substantially, and it is going to take a lot of investment and strategic planning to recover the lost ground. In the case of the JSF, its dwindling number of supporters claim it has abilities that can't be revealed. In the military game you tell the other side what you can do because then they are less likely to attack. Keeping it secret makes them think you are bluffing, so the risk of war is increased. It's a bit like corporations.

And when it comes to corporations if you look at our big banks, four large retailers and miners (like BHP Billiton), most concentrate on cost reduction. Few are making adventurous strides. They leave that space to more aggressive and flexible small arrivals and other disruptors. So far shareholders have been well rewarded by this strategy because it has spun off large amounts of cash and dividends. Wesfarmers' Coles would legitimately claim that is it forging into financial service areas, but there is little sign that it sees online retailing as a huge long-term growth area which now requires substantial investment.

Growth and SEEK

Last week I talked about CSL and its growth strategies. This week I mention SEEK, which is shaping up as one of the world's major players in online classifieds. It has not performed in education as well as it would have hoped but it is still in the market and, in time, its strategies may pay off. Expanding globally in classifieds is a very expensive exercise but the company has a high price-earnings ratio so the market is awarding SEEK with a high growth rating.

Of course many chief executives who look at SEEK say that if it stumbles in the growth strategy the share price will slump dramatically. And they give that as a reason not to come up with growth strategies.

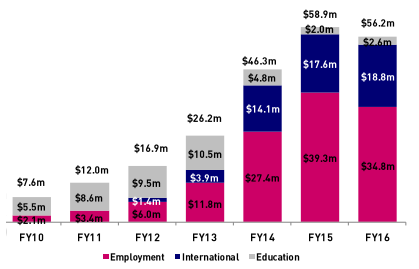

Chart 2: Thinking big ... SEEK capex, by segment

Source: SEK annual results presentation

In fairness, many boards and CEOs don't have the talents to adopt aggressive growth strategies either on the domestic or global stages. But longer term, business and share investment is about growth and innovation and at some point companies that just sit on their pile and cut costs fall out of favour. They are often taken over.

The US and BlueScope

One of the most unpopular stocks on the market for a long time has been BlueScope, which was spun out of BHP. Go back a couple of decades and BlueScope had brilliant managers who developed an Asian and US business. Then came the global financial crisis and their overseas investments looked silly. Moreover, as they were expanding overseas they had negotiated poorly with their local labour force and as a result BlueScope's Port Kembla operation became uneconomic.

Today I was looking at the Macquarie reviews of BlueScope, which produced some good results in 2014-15 including reducing its debt. In 2016-17 Macquarie is forecasting that the local steel business will lift its EBIT (earnings before interest and tax) from $261 million to $535m and its building products business in Asian, North America and India from $149m to $171m. Its US hot-roll steel products operation is expected to rise from $147m to $185m.

Of course BlueScope is benefiting from some tough talking from Australian managers to the unions which made the local Port Kembla plant suddenly economic. (Many other companies are too scared to negotiate with unions and workers).

In addition it is benefiting from higher steel prices caused partly by cutbacks in China's production. But the surprising win is in the US, which is becoming a more difficult place for steel imports – which is boosting the BlueScope business.

Chart 3: BlueScope's changing business - underlying earnings before interest and tax ($m)

Source: BSL annual results presentation

Obviously lots of things could go wrong but Macquarie believes that BlueScope can lift its underlining earnings per share from 51.4 cents to 91.4c in 2016-17 – a huge jump. Now, Macquarie expects earnings to slip in the 2018 year but that relies on pessimistic assumptions that are a long way out.

The short-term outlook for BlueScope in the US is a good sign for the underlining US economy and is a pointer that, in time, we will indeed see higher US interest rates.

Many are hoping that on Friday in her Jackson Hole address US Federal Reserve chair Janet Yellen will give real clues for what might happen. I don't think she will say anything worthwhile but I will be listening in case I am wrong.