Australia's top sectors in a slowing economy

Summary: The GDP data released today by the Australian Bureau of Statistics was a major disappointment, with growth well below economist forecasts. While the mining sector remains the stand out concern, this time weakness came from softer-than-expected consumer spending – which had been strong in the previous quarter. What's interesting, however, is that there are clear signs of an exceptionally strong upturn in a number of other industries. |

Key take-out: Notwithstanding today's data – which need to be taken with a large dose of salt – there are areas of strength in the economy. Investors should look for opportunities in high-growth sectors, including construction, accommodation, food services, financial services and real estate. These key sectors may also get further support from a rate cut that's looking more and more likely. |

Key beneficiaries: General investors. Category: Shares. |

On the same day that Bank of America Merrill Lynch chief economist Saul Eslake declared a recession in Australia, the Australian Bureau of Statistics released data showing that some areas of the economy are actually doing extremely well.

We're not in a recession I might add, not even close, so investors needn't worry. Similarly, national income isn't falling. The measure that economists use to justify that statement – the misleadingly titled 'real net national disposable income' – doesn't actually measure what the country earns as income.

What it does do is adjusts gross domestic product (GDP) to the prices of our exports and imports (the terms of trade). So if the terms of trade falls sharply, then naturally, any measure of GDP that is adjusted by the terms of trade will fall. Yet just because the terms of trade falls, that doesn't mean that national income is really falling – the terms of trade is only a relative price index. Nothing more.

A much better measure of national income is GDP measured on an income basis. This is derived as the sum of income earned from households, company profits, etc. That is, what the country has actually earned – not just what export and import prices have done. On this more accurate measure, national income is actually rising at a solid pace – around trend on the latest figures with quarterly growth of 0.5%, or around 3% annually.

It's true to say that some areas of the economy aren't doing as well as they once were. Indeed, today's GDP figures were a major disappointment. Economists had expected GDP to rise by 0.7% for the September quarter and by 3.1% over the year. Instead growth was only 0.3% for the quarter and 2.7% higher over the year.

It has to be said though that the weakness isn't due to the end of the mining boom as such, but rather much softer-than-expected consumer spending. Partial indicators had suggested consumer spending could be as high as 1%, but in the end, the actual result was only 0.5%.

Whether this is just a one off of or the start of a new trend is uncertain as consumer spending in the previous quarter had been strong and the Australian Bureau of Statistics (ABS) seems to be having some quite serious problems with many of its data points such as the Labour Force Survey.

On a sectoral basis, weakness in mining is the obvious stand out concern. Yet even here things aren't as bad as what is being made out. According to ABS data earlier in the week, while profits (-15% over the year) and nominal sales (-8% annually) have softened, actual production levels are very strong.

The slowdown in nominal sales and profits don't reflect weak demand. Rather, they reflect a sharp drop in prices.

The mining sector has its challenges, certainly, but that has more to do with adjusting to less extreme pricing rather than an actual deterioration in growth prospects. Prospects remain bright once the dust settles. You can see this in the incredibly strong sales volumes data (up almost 9% over the year) which hit new records in the September quarter.

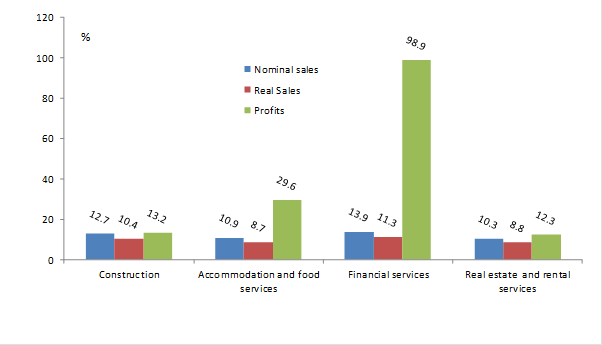

What's interesting, however, and often not reported is that outside of mining, there are clear signs of an exceptionally strong upturn in a number of other industries. Take a look at chart 1 below.

Chart 1: Australia's outperforming industries (annual growth)

Construction, accommodation and food services (restaurants, etc.), financial services and real estate and rental services are the winning sectors of the Australian economy at the moment, measured on three metrics: nominal sales (revenue basically), real sales (volumes – which strip out price impacts) and gross profits.

As you can see from the chart, growth is very strong. We've got double-digit sales and profit growth in each case – outcomes that are well above trend. These kinds of outcomes aren't necessarily restricted to those four sectors, I might add. For instance, information and telecommunications service companies are doing well.

Together these sectors account for about a quarter of the national economy compared to mining's 10%. Similarly, they employ a quarter of the labour market while the mining sector only employs 1-2%. The good news is that these are the interest rate sensitive sectors; they show that monetary policy is working – if more slowly than usual.

Notwithstanding today's weaker-than-expected Australian growth figures – which readers need to take with a very large dose of salt – there are areas of strength in the economy. Investors should look for opportunities in the key sectors mentioned above, which, if the RBA takes today's number seriously, may get further support from a rate cut.

The planets are aligning for a rate cut, with the market now pricing in an 80-90% chance of one next year. Economists, in contrast, had expected the RBA to hike rates next year. Following these figures, however, I suspect there will be a litany changes to rate forecasts. This perhaps won' be immediate, but will certainly occur as we get into 2015.