2016: Strong outlook with tremendous scope for growth

Summary: Jobs growth is the strongest it has been for seven years. The non-mining economy is doing quite well while business conditions are above average and business credit growth is rising. A number of indicators point to solid and ongoing strength in the non-mining sector, which is unlikely to be curbed by high debt or rising interest rates. Although China is slowing, growth in our major trading partners is only slightly below trend. |

Key take out: While some negatives may weigh, they don't look like they'll be sufficient to offset the tremendous scope for strong growth in the Australian economy. |

Key beneficiaries: General Investors. Category: Economy. |

What to make of the Australian economy as we close out the year and head towards 2016? The Reserve Bank is more optimistic, but a lot of people are talking about a housing slump next year. So confusion reigns.

To get a sense of where we might be going, it pays to first have a look at the state of play. Timely, because the statisticians just gave an update on the economy's performance today.

Now as regular readers will know, I've been a long-term bull on the Aussie economy. That view hasn't been completely vindicated, sure, but it's been largely vindicated and that will have to do.

So and as today's GDP figures show, the economy is growing at a slightly sub-trend rate of 2.5 per cent. Although to be fair, apparently the new trend rate is between 2.5 and 2.75 per cent, so if we're below, we're not too far below.

Having said that, a bullish view is supported in many other respects. A couple of years ago, I wrote in these pages that the Aussie economy could boom – all the planets were aligned. As it turns out, we only got some of that boom.

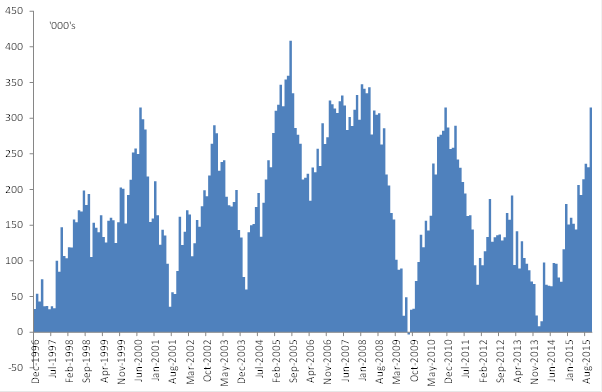

Chart 1: Jobs growth strongest in 7 years

So jobs growth for instance is the strongest it has been for seven years. 315,000 jobs were created over the last year. And while many people don't believe the job figures, that argument is a little tired for two reasons.

- First, there is persistence in this strong jobs growth.

- Second, because most of the anomalies in the data actually act to weaken the jobs gains and lift the unemployment rate. If you correct for those anomalies, jobs growth is actually stronger and the unemployment rate markedly lower.

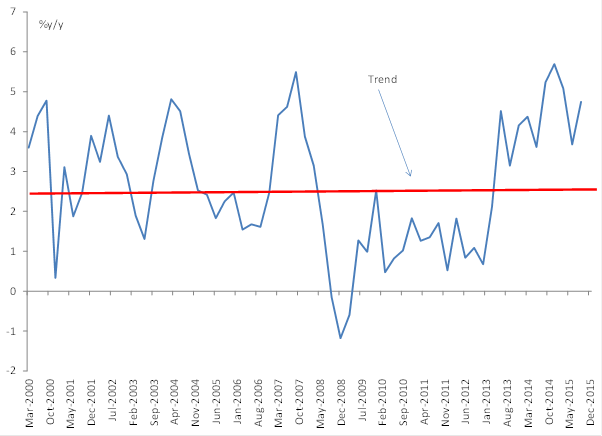

This jobs growth shouldn't be surprising anyway. Because the non-mining economy is actually doing quite well as shown in chart 2 below. For some years now, growth in the private sector, excluding mining investment has been running well above trend – there's your boom right there. It's just that the mining investment slump is masking it.

Chart 2: The non-mining private economy is growing well above trend

Really, the only problem for Australia, as I've been arguing for a while now, is/was confidence. That idea, unique at the time, has now gained considerable traction and policy makers too have suggested something similar. Importantly they've also noted the possibility that cutting rates further might actually harm it.

With that in mind, there are two key economic questions:.

- Why is public spending so weak at a time that the budget shows spending is strong?

- What explains the absence of a strong pick-up in non-mining investment?

The outlook for 2016 – how well the Australian economy performs – will really depend on these two components. Together, they compromise roughly one-third of the Aussie economy, but they are the big swing factors.

Now on the public spending side of things, I have no explanation – nor I have I seen an adequate one – for the divergence between the Budget and the national accounts. There is no reason why public spending should be so weak though. There haven't been any spending cuts since the GFC.

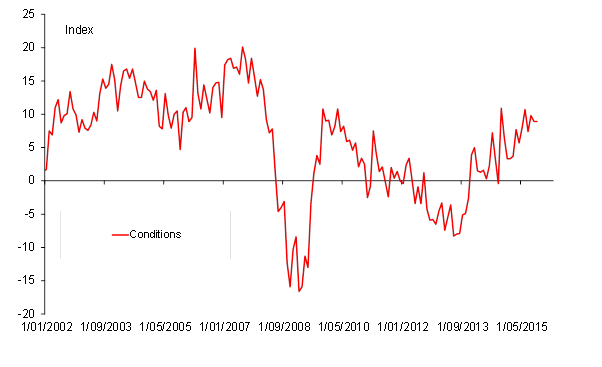

And what of non-mining investment? Well, here there are very positive signs emerging. For a start, reported business conditions are robust. So according to NAB's monthly business survey, business conditions are elevated, well above average, and have been so for eight consecutive months.

Chart 3: Business conditions rising

So while business confidence has been bouncing around a lot, if actual reported conditions are coming in at a solid clip, then it makes sense to expect that investment will follow.

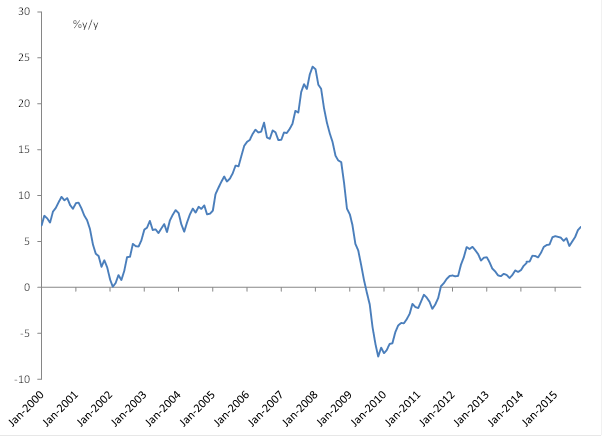

Now take a look at chart 4. It shows business credit growth accelerating which is another sign that the non-mining business sector is picking up.

At 6.6 per cent annual growth on the latest figures, business credit growth is the best post-GFC performance we've seen. Two things are noteworthy in that regard. One is that even at the fastest pace in seven years, credit growth isn't hitting any speed limits. The peak at the last cycle was over 20 per cent. Secondly, non-financial corporates, as a general rule, are not excessively geared. Balance sheets are healthy. So heavy debt isn't a constraint to this credit growth or non-financial corporate activity.

Chart 4: As is business credit growth

Take a look at charts 3 and 4 again. They follow a similar path – so you begin to see the picture. We've got a number of indicators – business conditions, business credit, strong jobs growth (business is hiring) that all point to solid and ongoing strength in the non-mining sector.

What's going to end that? It's not high debt and it's unlikely to be interest rates. Rates aren't going up for a while, and if so not by much. Consumers in Australia – the biggest chunk of the economy – are otherwise in a good position. The unemployment rate is falling, jobs growth is strong. Then, and while debt is at a record – debt servicing is at a decade low.

Moreover, the average Australian isn't in debt anyway. Only one-third of Australians have a mortgage and most of these have low debt. On the Reserve Bank's own figures, most of the debt in Australia is held by a minority of heavily indebted, but high income, households.

As for the expected housing slump? Construction may slow but a slump is unlikely. The population is still growing and as I have highlighted in the past, there is still a shortage in three-quarters of the housing stock – detached housing. There is only a glut of apartments in some areas, but this only represents a small part of the economy.

Elsewhere, China is slowing and the commodity slump is hurting, sure. Yet as the RBA noted recently, growth in our major trading partners is only slightly below trend. It's not bad.

So while some negatives may weigh, they don't look like they'll be sufficient to offset the tremendous scope for strong growth. All of this suggests that the outlook for the Australian economy is very good – excellent perhaps.

This is my final weekly column for Eureka Report.