Taking advantage of a downturn

Since the LIC model portfolio's first purchase we have seen the market up to 5727 and as low as 4918. We've seen our fair share of gyrations in between and right now we are in the middle of another headline-catching downtrend.

It is apparent the LIC portfolio is cash heavy (for more on this, see The LIC model portfolio: Where to from here?, November 2). Now the market has begun to track down again the LIC model portfolio readies itself to splash some cash and let the managers do what they do.

From the start I said I would take my time getting the portfolio set. At the same time I did mention it was not my intention to try and be too cute with it either. This is meant to be as close to a hands-off approach as you can get with the exception of a little tinkering here and there on the very odd occasion. That odd occasion would include a change in portfolio manager, excessive price to NTA or the manager straying from the investment mandate.

I recently flagged three stocks I was looking to add further to. One of them has now dropped out of the running due to strong share price performance but two remain. Another has put its hand up for more cash after strong NTA growth which has been largely ignored by the market.

MFF moves to a hold

First, some housekeeping. Magellan Flagship Fund (MFF) has been a great buy so far for the LIC portfolio. It was the first stock in the door and has given us a little sniff of a dividend but mostly solid share price and NTA growth in a difficult market.

MFF is trading on or just over (depending on the time of day) its NTA when you take into consideration the dilutionary effect the options will have when exercised in 2017. The exercise price is $0.9964. With the share price at $2.06 at the time of writing it is safe to say they are well in the money.

The last reported NTA was $2.229 and in the announcement the kind folk at MFF do the calculation of the dilution effect for you which is $0.18. This makes the future NTA $2.049. I would like to own more MFF in the portfolio but we will have to be patient for now.

I'm changing my call on MFF from buy to hold because of share price strength.

PAF, the too-quiet achiever

PM Capital Asian Opportunities Fund (PAF), on the other hand, has been the quiet achiever of the group. Perhaps it needs to sing its own praises louder and so do I.

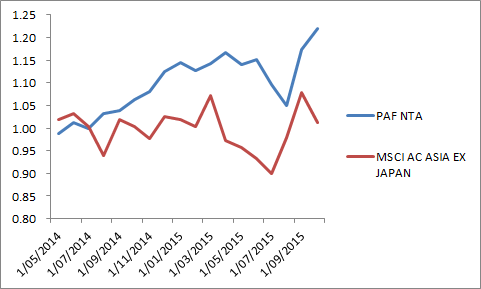

Here is a chart of the underlying performance of PAF versus the benchmark of the MSCI All Country Asia ex Japan index.

Portfolio manager Kevin Bertoli and team have gone about their business quietly at PM Capital and as you can see they have put light years between PAF and the index through their careful stock selection. Bertoli purposefully held back with the portfolio's cash and is now almost fully invested with the last monthly report showing 4.9 per cent cash.

At the time of writing the share price for PAF was still below the IPO price of $1. The last reported NTA was $1.1778. It is currently trading at a discount of 17.64 per cent. What also gives me confidence in the shorter term is PAF has options expiring on May 31, 2016. There are 55 million options on the table exercisable at $1. This means a potential extra $55 million in funds under management (FUM). That in turn means an additional $55 million worth of FUM the manager PM Capital will be able to collect management fees on going forward into perpetuity. Management's interests are aligned with shareholders here to grow that share price. These options also have the potential to create further liquidity for PAF shareholders as well.

If the NTA performance continues the way it has, management's spruiking job will be all the easier. Even taking into consideration the dilution effect on the NTA if all the options are exercised it is still an attractive proposition.

This week I intend to sit down with portfolio manager Kevin Bertoli to discuss the portfolio in full. Keep an eye out for an in-depth report to follow.

I will be adding an extra 5 per cent to the portfolio's PAF holding as of market open tomorrow, November 17.

Why more BKI?

BKI is a cornerstone (or brick boom-tish!) of the portfolio. I am happy to have it as the major component of the portfolio giving me exposure to the larger cap end of the Australian market. With BKI you have team members who take a legitimate long-term view and who are committed to doing what they say they do and have plenty of skin in the game. I am adding an extra 5 per cent to the portfolio's BKI holding.

The team clearly communicates with shareholders through frequent updates like the presentation from the AGM and gives you an insight into the long-term planning of the portfolio. The recent presentation highlighted key long-term thematics Millner and his team are positioning the portfolio to take advantage of. Additionally the presentation highlighted they anticipated the dividend to remain at currently levels or potentially grow for next year. In an uncertain market this will help to maintain stability. It will also be a vital source of income for the portfolio given the model portfolio's international exposure will not provide much if any.

I would also like to take the opportunity to offer the reminder that BKI is not just an ETF in disguise as a managed portfolio. Looking at the top 20 holdings, they are underweight a number of sectors.

Additionally I know BKI is not trading at a discount. I know it is trading at a premium. The premium is not great. And in times of turmoil for the likes of BKI, the other elder statesmen of the LIC space trade at a premium. It is what happens. But the market has fallen and this is a long game.

If you want to be looking at large cap Aussie equities LICs that are trading at a discount you will need to look for the under performers and look for comeback stories. I note the team at Wilson Asset Management has recently become a substantial shareholder on battling Westoz Investment Company (WIC). This is trading at a very large discount of 15.22 per cent. WAM has previously done this with Century Australia Investments (CYA) and Hunter Hall Global (HHV). The team there does look for catalysts when investing and when it comes to LICs sometimes they themselves are the catalyst.

Why more WAX?

WAM Research's (WAX) moves are relatively uncorrelated to the market for two reasons. First, the cash holding typically remains high. Second, the mid to small cap stocks that make up the portfolio are generally not included in an index. WAX invests in companies, not markets and not thematics. They stock enjoyed a nice run up to the ex-dividend date and has experienced some softness since.

WAX has a strong history of performance and a very capable management team who have been proven over many years. The managers are committed to paying good dividends as shown over the years in all the Wilson Asset Management LICs. I am content to have more in WAX than in my other mid cap manager Perpetual Equity Investment Company (PIC) simply because of the track record WAX has especially when it comes to paying nice juicy dividends. I don't doubt PIC will perform for the portfolio over time but when it comes to allocating more capital I am going to back my tried and tested LIC. Also now with PIC's share price closing in on $1 and then hopefully continuing to track towards NTA, the rise brings into play the options (strike price of $1). These will weigh a little on PIC unless the NTA continues to move forward materially.

I am adding an extra 5 per cent to the portfolio's WAX holding.