Asset allocation alert 1: Bonds and traditional index funds fade

Summary: It should be possible to build an index beating portfolio by adopting a multi-factor approach to share investing and investing less in low yielding government bonds. |

Key take-out: While a good starting point for investing, indices aren't perfectly constructed and recent events that have advantaged them may reverse in the future, as and when we return to an old normal, higher bond yield environment. |

Key beneficiaries: General investors. Category: Strategy. |

Asset allocation always demands attention. Today I'd like to recap why you need to pause and rethink about slavishly following market capitalisation based indices which are no longer always the safest bet.

First we'll talk about shares, then bonds and offer some broad suggestions to the active investor.

While investing in index funds is an efficient way to access the returns from the whole market, there are ways to systematically beat the index over the long term through smarter portfolio construction.

Regardless of any aspiration to beat the index, sometimes you also need to invest differently than the index simply to undo risky biases that arise in unusual times like the present. (Tony Rumble addresses similar issues in his piece today - Asset allocation alert 2: DAA, a new investment approach.)

Now is a particularly good time to revisit solely investing in index funds as doing so can cause you to for instance, allocate 40 per cent of your Australian share exposure to Australian banks and lock you into a sub 3 per cent yield for five years lending through your bond exposure. For most investors that outcome is simply not good enough. So let's see what might be done...

Australian share market: Most concentrated, least defensive

Earlier I showed that the Australian share market was one of the most concentrated and least defensive share markets in the world (Goodbye to the “All Ordinaries”, June 6, 2012).

Then in June 2012 our share market was 33 per cent financials (excluding property trusts) and 30 per cent resources (materials and energy stocks). As I mentioned then, you wouldn't set out to build a portfolio where two thirds of your returns were driven by just two things: 1) banks' ability to lend to Australians keen on residential property and 2) resource companies selling commodities – both in volumes and at prices set by others and susceptible to boom and bust.

Since June 2012 falls in commodity prices and resource company prices have busted and especially hurt index investors overweight in these companies. This sector now only accounts for 20 per cent of the index, implying index investors lost one third on their hefty one-third exposure.

Now Australian index investors are 40 per cent invested in banks and financial companies (46 per cent if you include property trusts). Four banks alone nearly account for a third of the broad market index. They are even more sensitive to the fortunes of this sector. Let's hope they don't lose 40 per cent of their 40 per cent exposure in three years' time!

A quick glance at the pie pieces shown in Figure 1 shows how undiversified our broader market remains compared to even a concentrated top 100 global company index ETF.

Figure 1: Australian and Global share markets' mix of industry sectors and top companies shown for index style ETFs IOZ and IOO which provide returns from the top 200 local and a concentrated group of top 100 global companies respectively. Source: ishares

Factoring in better share market returns

Various academic studies have shown that the returns from the market aren't homogeneous and that it is possible over the long term to invest in types of shares that may outperform. This is not necessarily a free lunch, but a reward for taking more risk or undoing the big company, big price bias to market capitalisation based indices.

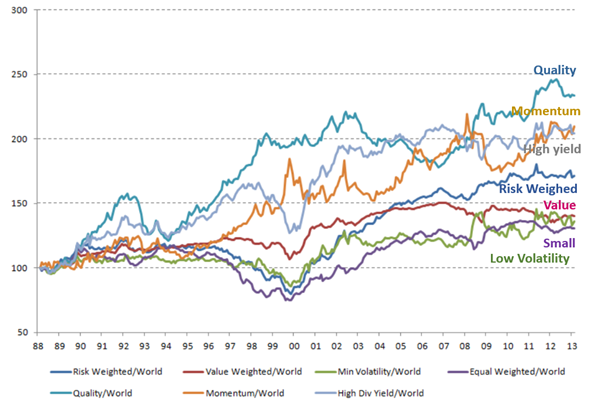

Index supplier MSCI neatly summarises the cumulative excess return investing in various factors delivered over recent time (Figure 2). Following the introduction of index rules based on these factors, local and international listed ETFs have been introduced that you can invest in to introduce these factors into your portfolio.

Figure 2: Cumulative excess return from investing in various factors, expressed as a ratio to broader market global share market returns (MSCI World) indexed to 100 from 1988 to 2013. Source: MSCI

Of note:

- Professor Eugene Fama recently won a Nobel Prize for his work showing that over the long term cheap companies outperform expensive companies. However looking closely at Figure 2 you should see that since 2007 value companies have not kept out with the returns of growth stocks like Apple and other IT darlings. In Australia, value has outperformed growth, but only if you count bank shares as value. Clearly ETF supplier Russell does, having 50 per cent financials in its value ETF “RVL”.

- Like out of favour value companies, small companies are also riskier investments and should return investors a premium return for investing in a diversified mix of them. This was especially true if you avoided holding them in your portfolio for the latter half of 1990s when small companies globally underperformed. In Australia investors in the Small Ordinaries index would have been disappointed earning minus 1 per cent annually over the last three years compared to earning about 14 per cent annually over the last three years investing in the bigger All Ordinaries index. Earlier I suggested that the Small Ordinaries was a very ordinary index and probably best avoided when investing in small companies (see A small-cap strategy that works, October 31, 2011). This sector has struggled with a large exposure to materials companies including those with one mine, one mineral and now no hope.

- Momentum is the idea that company share prices that are on a run, stay on a run. This also applies to commodity prices and currency which Commodity Trading or CTA funds bet on when trading futures contracts. While a rewarding strategy for some of the time, you can see in Figure 2 this is the bumpiest way to try to beat the market. Sometimes momentum reverses sharply.

- Low volatility companies are boring companies which investors tend to avoid, leaving their share prices more stable. While they don't tend to outperform, this characteristic can be “leveraged” by some (too?) clever investors who borrow money to load up on them, expecting afterwards to earn a better return for the same risk of investing in the more volatile broader market unlevered. Low volatile stocks include(d) utilities and infrastructure which the market has embraced as a bond substitute which probably helped this strategy work, but now might put it at risk.

- High dividend and defensive quality companies have done particularly well in the current low interest rate environment. Having more of them in your portfolio would have helped returns over the last five years but perhaps not for as long as the prior 10 years. They are probably over valued now and at risk of delivering a less than premium return also.

- As you can see the benefit of these factors is temporal. Unless you are very good at picking turning points, it would be smarter to incorporate a mixture of these into your portfolio for the long term.

Share market investors who want to beat the market “multi-factor” investing can do so by choosing stocks in their portfolio that have these characteristics and trade accordingly. They can also employ active style fund managers who follow these strategies – value managers being one example.

Another way is to invest in ETFs built on customised indices designed to give investor exposures to one or more of these factors – also called “smart beta” investing (see Everything you need to know about “smart beta”, April 1). Of course, traditional index suppliers must find this frustrating as it implies they deliver “dumb beta”.

These can be combined with a traditional core index exposure (for instance invested in Australian share ETFs IOZ, VAS, STW) or in place of (for instance BetaShares FTSE RAFI Australia 200 ETF (QOZ).

Given my concerns above about the makeup of our local market, any attempt to add performance which also undoes sector and stock concentration risks has merit in my opinion.

Now let's talk about the defensive debt side of your portfolio.

Is index lending into manipulated markets wise?

Bonds and deposits are supposed to be defensive investments. However after interest rates have been set below the rate of inflation and money has been printed to buy government bonds, you have to question this assumption and question whether index funds based on bonds are truly defensive.

The main bond indices accessible to Australian investors via exchange-traded products are heavily or solely based on government bonds. Locally, this is because of our poorly developed corporate bond market. Overseas, this is because of government budget mismanagement and indebtedness – which sadly we seem keen on imitating.

A peculiarity of investing following a bond index as a guide, is that the more indebted a country or company is, the more you lend to them.

In the last few weeks we have seen cracks in the global bond market. An often compared 10 year loan to the Federal Government pays 2.9 per cent today, sharply up from the low of 2.3 per cent weeks ago. Figure 3 shows the price of this bond over the last six months. Over the last month it has fallen about 7.5 per cent which equals three years of return an investor was expecting to earn had they invested one month ago. Does this sound defensive to you?

Figure 3: ASX tradeable price of GSB25, a 3.25 per cent annual coupon paying bond issued by the Commonwealth Government maturing in 10 years in 2025 for $100.

An alternative to investing in static bond indices based heavily on long duration government bonds, is to invest with a bond manager who dynamically invests in a range of different bond maturities and credit risks. While this has merit, in the current environment this has required taking on significant, now poorly rewarded, credit risk. Some commentators have pointed out the next financial crisis could arise when investors rush to exit from high yield (non-investment grade or “junk”) bonds when concerns about future returns and default emerge. This means you need to choose a fund carefully.

Another hurdle for institutional fund managers is the poorer yield they get on cash compared to you. Because of their sizable funds and tendency to want their money back, they aren't welcome by banks. Instead they invest in the lowly yielding money market. As always, there they can only get about 0.1 to 0.2 per cent above the now 2 per cent cash rate. Given also that money printing central banks aren't investing in bank deposits either, and Australian banks are being “encouraged” by APRA to raise more sticky local funding, deposits aren't so bad. Despite “absolutely” poor returns, their relative returns are excellent. We'll have to see if my efforts to champion better interest rates for you meet with any success (see It's time central bankers considered citizens, March 18).

For many years I have championed bond investing to Eureka Report readers. Just for now, I can't and especially bond funds built on static indices overweighted to long maturity, government debt.

About multi-asset funds

Over recent years it has been difficult for multi-asset, active investors and multi-factor passive investors to beat portfolios constructed from index funds. This is for two reasons: 1) the major Australian share index overweights big and expensive dividend paying banks and defensive companies which rallied, and 2) the bond allocation of index funds is tilted to long duration sovereign issues which have also.

So while I have a lot of time for studies like those from SPIVA which show how few beat the index, it is possible we might see index funds winning less often, if and as the market turns away from those assets rich in index portfolios.

Earlier I pointed out that while interest rates and bond yields are so low, investors in “Conservative” portfolios might need to become more “Balanced” in their approach – by which I mean embrace say a 50/50 mix of equity and bonds (not funds mislabelled as such, for example this one).

Investors in a Conservative portfolio built using index funds should be even more careful. For instance in a well-meaning fund like that from Vanguard, know they are allocating 60 per cent of their money to bonds, including most of that into government bonds; with the extra 10 per cent allocated to cash, they might return less than high yielding deposits.

Conclusion

Indexing is still a smart way to invest, however, know that in unique share markets like Australia, an index construction can be heavily biased (currently to banks, earlier also to resources). In unique times like now, their bias to longer duration government bonds might not also prove ideal.

An irony of my other message that you should be able to beat the index by more smartly constructing a multi-factor portfolio (and buy less government bonds), is that over recent years you didn't. After recent reversals in the rising prices of Government bonds and big, expensive high yield stocks, the answer is probably now you will.

Dr Douglas Turek is Principal Advisor of family wealth advisory and money management firm Professional Wealth.