It's time central bankers considered citizens

Summary: Central banks aren't mandated to worry about low depositor and other debt investor returns. But maybe they should. And maybe the RBA Board needs a representative from the personal investment community to champion investors' interests. |

Key take-out: Despite the squeeze on debt investors, Australia is one of only three developed countries with benchmark interest rates running above inflation. Globally, Australia is still the lucky country. |

Key beneficiaries: General investors. Category: Fixed interest. |

The Reserve Bank of Australia (RBA) chose yet again to keep interest rates unchanged this month which would have been a relief for millions of “depressed” depositors. For several years now debt investors worldwide have been called upon to subsidise the recovery of the global economy, shore up the balance sheets of financial institutions and help indebted governments borrow cheaply and some now freely. Lately these same investors have become caught up in a global currency war of sorts where various countries print money and/or bid down their interest rates to try to import jobs or avoid exporting them to those who are. As I suggested earlier, this is causing a “melt up” in most asset classes (see Will the markets melt up?, February 4).

In case you are wondering, you are almost certainly a “debt investor”. After all, it occurs any time you lend money to a bank, government, company or other institution, either through deposit, owning a bond directly, or indirectly in a bond or multi-asset fund. The issue of earning a fair return is especially important for conservative investors and those near or in retirement that can't expose a lot of their portfolio to the volatility of share prices or manage the indivisibility of direct property.

Given the immense powers of central banks around the world to set interest rates and interfere in the market pricing of bonds, I think it should be asked:

1. Should central banks take into account the needs of debt investors to earn a reasonable rate of return in their decision making?

2. Do or should central bank boards have representation from those sensitive about or experienced in the needs of investors?

As at time of writing the RBA has not chosen to answer these questions so I'll have a try here.

Do central banks care?

According to definition central banks and monetary authorities “manage the nation's money supply (monetary policy), through active duties such as managing interest rates, setting the reserve requirement, and acting as a lender of last resort to the banking sector during times of bank insolvency or financial crisis. Central banks in most developed nations are institutionally designed to be independent from political interference. Still, limited control by the executive and legislative bodies usually exists.” (Source here)

In Australia the Reserve Bank is an independent statutory authority, established by an Act of Parliament, the Reserve Bank Act 1959. According to the Act the function of the Reserve Bank Board (the board responsible for non-payment matters) is to “best contribute to:

(a) the stability of the currency of Australia;

(b) the maintenance of full employment in Australia; and

(c) the economic prosperity and welfare of the people of Australia”.

You can see that providing a reasonable rate of return to debt investors is not explicitly in its mandate. You could argue that contributing to the economic prosperity and welfare of investors is included, however, that would be offset at least equally by contributing to the prosperity and welfare of borrowers.

We aren't unique. Elsewhere in the world, mandates are largely the same.

Here's what you will read if you peruse various central bank websites.

* USA: The Federal Reserve System has been given a dual mandate – pursuing the economic goals of price stability and maximum employment.

* Canada: The Bank of Canada is the nation's central bank. Its principal role is to promote the economic and financial welfare of Canada.

* UK: The Bank of England's monetary policy objective is to deliver price stability and, subject to that, to support the Government's economic objectives including those for growth and employment.

* ECB: The European Union has multiple objectives (Article 3 of the Treaty on European Union), which include the sustainable development of Europe based on balanced economic growth and price stability, and a highly competitive social market economy, aiming at full employment and social progress.

* Bank of Japan: The Act sets the Bank's objectives "to issue banknotes and to carry out currency and monetary control" and "to ensure smooth settlement of funds among banks and other financial institutions, thereby contributing to the maintenance of stability of the financial system."

I can't see that caring that depositors and bond investors earn a reasonable, say at least an inflation-matching, return on their cash and bonds is on any list. Can you?

If you read RBA minutes you won't see this being discussed either.

In summary, the banks' jobs are to: stop runs on banks (best not mentioned), avoid corrosive inflation and consumption-stalling deflation, stabilise the currency and drive full employment – put another way, enable borrowing as cheaply as possible before inflation breaks out.

When the Reserve Bank Act was written in 1959, I suspect there weren't many self-funded retirees around, so it's not surprising their interest in adequate debt investor yields wasn't considered.

Maybe it's time to update the Act, adding in the objective to balance the needs of debt investors to earn a fair return with the borrowers accessing capital as cheaply as possible. Central bankers seem very good at managing trade-offs and I suspect they can manage one more.

Kohler for RBA?

There are nine members on the Reserve Bank Board chaired by Governor Glenn Stevens, who I have met and have tremendous respect for. Governor Stevens is joined by one other RBA member, Deputy Chair Philip Lowe, whose words interest rate diviners equally wait patiently on. They are joined by Treasury Secretary John Fraser (representative of Government) and five eminent Australians – economist John Edwards and current or former business executives and professional company directors John Akehurst, Roger Corbett, Heather Ridout, Kathryn Fagg and Catherine Tanna.

While these individuals are indeed eminently qualified I wonder if the make-up of the Board should include someone with more experience working with personal investors? In fairness, amongst other company director duties, Kathryn Fagg is a director of Djerriwarrh Investments and Heather Ridout chair of Australian Super's Trustee Board so they should understand investor impact – it's just their mandate doesn't put much priority on caring for individual investors.

Roger Corbett's 10 year term is next up in December 2015 and I wonder whether the Federal Treasurer, who appoints RBA Board members, might want to think of adding someone who can represent or at least better relay the needs of personal investors.

Who? Well how about Alan Kohler?

In my opinion he would be good at championing personal investors' “interest”.

In defence of central banks' inflation paranoia

While I believe central banks' mandate should be expanded and perhaps the make-up of rate setting boards could be improved, let me say I'm glad they worry about inflation. As I pointed out earlier (see How to prepare for inflation, March 29, 2010) inflation is the number one enemy of self-funded retirees and we should never wish its return.

In the past when central banks have been late raising interest rates (in the 1970s for instance) this has harmed investor savings. When share markets collapsed, I too cheered when interest rates fell and bonds rallied upwards. It's probably also true that local and world government dysfunction required central banks to intervene more excessively to avoid calamity. They are doing a good job but some may have gone too far.

Not worrying enough about excessively low interest rates can drive asset prices to unsustainable levels and creates generational disadvantage, for instance between those old enough to enjoy asset price inflation and those young enough trying to buy their way into an expensive property market. Zero interest and ultra-low bond yields, especially overseas, will make many defined benefit pension plans insolvent. Prolonged asset inflation could lead to cost inflation when one day scarce workers (the unaged population coming) demand higher wages to afford expensive assets. In the meantime it simply robs depositors of a fair income to live off and drives some into risky investments they shouldn't make.

Australia is still the lucky country

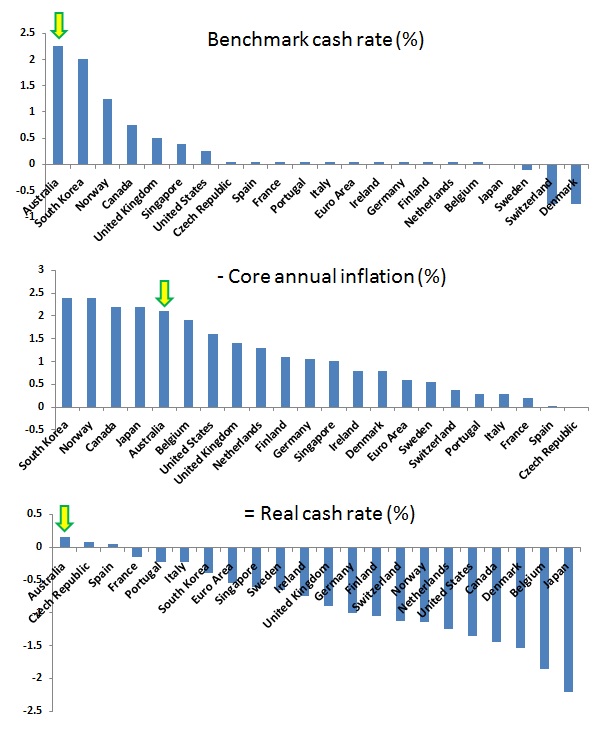

It is also important to put into perspective Australia's version of “repression” versus that overseas. Australians can take some comfort knowing they benefit from 1) the highest nominal benchmark interest rate amongst developed countries and 2) a banking system so desperate for cash to on-lend, they have an ability to earn nearly 1 per cent additional return above the benchmark rate.

The below figure shows Australia with a current cash rate of 2.25 per cent ranks generously above 22 other developed countries – including 15 whose benchmark rates are between 0 and 0.5 per cent and three which charge investors for holding cash.

Further if you believe that Australian consumer prices are only rising at 2.1 per cent annually then we are only 1 of 3 developed countries with “real” benchmark interest rates – that is benchmark rates running above inflation. Probably we are the only country, if you think that inflation in the Czech Republic and Spain is not zero.

If Australia is the lucky country, figure 1 shows Japan is the least lucky.

Figure 1: Developed country nominal and real cash rates and core inflation as at 1 March 2015

Last month (see Will the markets melt up?) I showed also an Australian 10 year Commonwealth Government bond had never traded lower than then 2.24% yield. While absolutely this is a poor return, it is relatively generous compared to developed country bond yields which also extend into the negative.

Maybe the RBA does worry about debt investor returns or maybe just it worries that dropping rates further will provide a bigger high to property addicted investors?

In summary: Until I see soup kitchens on Collins Street and Martin Place, I will wonder if central banks have overstepped. They would argue their actions are to prevent that happening. And anyway, it's not on the top of their list to worry about the low returns of debt investors.

Dr Doug Turek is principal advisor of family wealth advisory firm Professional Wealth (www.professionalwealth.com.au).