Qube: Now to carve up Asciano?

Update: On November 10, Qube Holdings and its financial backers submitted a proposal to acquire all of the Asciano shares it does not already own. Qube's proposal would see Asciano shareholders receive $9.25 per AIO share, comprising around 75 per cent in cash with the balance in Qube stock.

At present the Qube consortium's offer seems to have a slight edge on that of its rival, Brookfield Infrastructure Partners, whose earlier offer gained the support of Asciano's board. If Asciano deems Qube's offer to be the best available, a bidding war could loom. We will analyse Qube's proposal and review our recommendation on the stock accordingly.

One of Eureka Report's favourite Growth First model portfolio stock picks, Qube Holdings (QUB), has suddenly hit the headlines. The logistics group has moved to become a player in the future of takeover target Asciano (AIO). At Eureka Report we are impressed with Qube's audacious move and we see a lot of upside. On the downside there is a chance Qube may have to go to the market for new equity.

Qube covets the Patrick container terminals and stevedoring assets that Asciano (AIO) has owned since 2007. Qube has wedged itself between Asciano's suitor, Brookfield Infrastructure Partners (NYSE:BIP), and the Patrick businesses — but the effectiveness of that wedge remains to be seen.

Qube should have a strong say in Patrick's ownership over the next few months. But in light of Brookfield amending its takeover offer as a response to the threat from Qube, it is far from a foregone conclusion that Qube would ultimately own or operate Patrick.

Acquiring Patrick at the right price could drive substantial value for QUB shareholders, but regardless of the outcome of the Asciano transaction, Qube looks well set to grow profits well into the future.

Raiders of the lost asset

Qube stunned the market on October 29 with its audacious raid on a block of Asciano (AIO) shares worth nearly $1.7 billion. With backing from two deep-pocketed North American financiers — the Canada Pension Plan Investment Board (CCPIB) and Global Infrastructure Partners (GIP) — Qube gained control of 19.99 per cent of its target.

Qube has minimised the impact of this purchase on its balance sheet by having the North Americans foot nearly 70 per cent of the bill, and by funding the bulk of the remainder through an equity swap with its adviser, investment bank UBS.

The Qube consortium bought the bulk of its AIO shares at $8.80 each. That was a 16.4 per cent premium to AIO's last close, but a notable discount to the $9.15 of value per share that Brookfield's original cash-and-scrip offer implied.

The vigour with which institutional investors sold their AIO shares to Qube at $8.80 shows three aspects of Brookfield's play for Asciano:

- It reveals Australian infrastructure investors' dim view of the merits of US-listed BIP shares.

- It reflects the lower likelihood of regulatory approval of Brookfield's takeover proposal, since the Australian Competition & Consumer Commission (ACCC) raised “red light” concerns about the bid.

- Most importantly, it's a vote of confidence in the value of the Patrick assets in Qube's hands.

Many of Qube's senior managers owned or operated Patrick Corporation until its takeover by Toll Holdings in 2006. There is a sense of unfinished business in Qube's raid for what insiders view as a “lost asset”.

The logic

Nobody outside Asciano understands the Patrick business better than Qube.

It was Qube chairman, Chris Corrigan, who grew Patrick Corporation through the 1990s ahead of its takeover by Toll Holdings, Asciano's former parent. Corrigan has an abiding passion for industrial efficiency and Patrick is only just beginning to enjoy the benefits of port automation conceived while he was managing director. Qube's managing director, Maurice James, enjoys a similarly strong grasp of the Patrick business, rising over his 12-year stint at the firm to Executive Director of Ports.

Qube's links to Patrick's past extend far beyond the boardroom. All but one of James' executive management team worked alongside him at Patrick. Qube's biggest shareholder, Peter Scanlon, was Corrigan's chairman at Patrick until the Toll takeover. The Patrick alumni are a close-knit crew — it's reported Corrigan and Scanlon even have adjacent villas in Tuscany.

Past relationships and cultural understanding aside, there's a much more tangible reason why, in James' words, “the market for several years now has seen us as natural owners of these assets and we believe they're a perfect fit for Qube”.

The opportunity

Qube's strategy has long involved a focus on efficiency gains where it drives costs out of the logistics supply chain. In light of management's proven ability to deliver on that front, it should make plenty of sense to bring Patrick into the Qube tent. What's more, Qube relies heavily on the cost effectiveness of its port providers — so letting Patrick fall into the hands of a potential “absentee landlord” in Brookfield could pose a real risk.

If Qube can integrate its storage, handling and distribution facilities at 29 ports with the Patrick container terminals in Melbourne, Sydney, Brisbane and Fremantle, it could meaningfully reinforce the firm's market position. There could be a particularly strong benefit in New South Wales, where Qube operates container rail from Port Botany. NSW Ports plans to triple Port Botany's throughput over the next 30 years, and for Qube to own more of that supply chain gives them a greater chance to capture integration benefits.

Qube views its ownership or management of the Patrick container terminals as a move that could generate valuable cost and revenue synergies with its existing businesses. The firm believes it could grow Patrick's container volumes, implement and expand Patrick's terminal automation project, improve the road and rail links into the terminals and enhance Patrick's operating procedures.

All of these initiatives could boost Patrick's profitability at a time when pressure on volumes and rates are challenging the industry. Qube's past achievements in executing a similar strategy suggest that combining the firms' operations could enhance QUB shareholder value over the medium term.

The preliminary nature of Qube's entry into the deal for Asciano makes it hard to forecast the scale of any eventual value uplift. It is yet to emerge whether Qube will seek to carve up and buy parts of Asciano, hold onto its strategic stake and seek board representation, or propose a joint venture where it runs the terminals with Brookfield as financial partner.

Qube is yet to disclose its preferred ownership and commercial arrangements. Despite Brookfield's insistence that it will remain an investor and oppose any breakup of Asciano if its takeover fails, discussions between the key players should establish a mutually agreeable outcome. Regardless of how those negotiations play out, the road to regulatory and shareholder approval could stretch well into 2016.

A moveable feast

As we publish this evening, Asciano has postponed its original plan for shareholders to vote on the Brookfield offer at its annual general meeting tomorrow (November 10). Asciano sought to defer the vote because Brookfield, which now controls more than 19.2 per cent of AIO, is seeking to outflank Qube with an off-market bid for 50.1 per cent of its target at the same price as its original offer.

This is an alternative and arguably more practical route to control of Asciano for Brookfield, running concurrent to its existing scheme of arrangement. It's worth noting that Brookfield running a scheme of arrangement and a takeover offer at the same time puts investors in seldom charted territory.

With Brookfield seemingly determined to oppose a break-up of Asciano, and Qube set to vote its 19.99 per cent stake against the offer, a stalemate looms — one where the ACCC might play a pivotal role as it delivers its ruling on the Brookfield offer on December 17. Qube would be in the box seat to carve up Asciano if the ACCC denies Brookfield's ambitions.

Brookfield could well get its foot on 50.1 per cent of Asciano, which is all it needs for its latest takeover proposal to succeed. However, it's hard to see the original scheme gaining the necessary approval of more than 75 per cent of AIO shareholders.

That being said, stranger things have happened. Earlier this year, TPG Telecom (TPM) moved to stymie Vocus Communications' (VOC) bid for Amcom Telecommunication by taking a 19.9 per cent blocking stake in the target. Amcom made Australian corporate history as it mobilised more than 90 per cent of its shareholders to fend off TPG and approve the deal.

Qube is likely working hard in the background on a superior offer to Asciano. The firm would want to make such a proposal quickly enough for Asciano shareholders to consider it before Brookfield's offer opens for acceptance in mid-December.

Qube would also want access to due diligence as part of a proposal to buy the Patrick assets, but the firm is wary of triggering Brookfield's substantial $88 million break fee. If Qube can't orchestrate an offer that avoids that material payment, Corrigan and co might extract leverage elsewhere in exchange for selling their 19.99 per cent stake into Brookfield's offer.

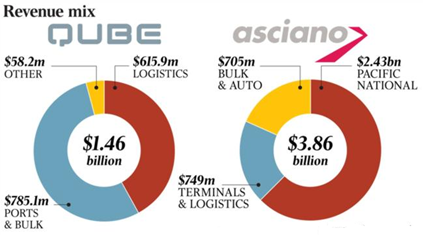

In analysing how the play for Asciano could change Qube, it's worth considering the chart below which shows the companies' relative revenue exposures in FY15.

Source: The Australian

Victory for the Qube consortium would likely see the North American financiers take Asciano's Pacific National rail freight business — which, as the chart above shows, is currently a larger business than Patrick. Qube has indicated it would engage actively with the ACCC to allay any competition concerns.

Such a deal would only boost shareholder value if Qube buys the container terminals and stevedoring business at the right price. In the scheme booklet for Brookfield's offer for Asciano, the independent expert valued Patrick at between $2.3 billion and $2.5bn, implying 10 to 11 times FY15 earnings before interest, tax, depreciation and amortisation. Assuming a similar transaction multiple, and accounting for the value of certain Asciano assets that Qube may seek beyond Patrick (i.e. the 50 per cent of cargo handling facility Australian Amalgamated Terminals that Qube doesn't already own), then Qube could be looking at an acquisition worth upwards of $3bn.

That could more than double Qube's size and would be a transformative event. Qube has indicated that its capital structure would remain unchanged and it would not significantly boost its gearing to acquire any company. On that basis, Qube shareholders should be mindful of the potential for a large capital raising to help carve up Asciano.

Valuation impact

I will factor the impact of these corporate actions into our Qube valuation when we gain clarity on the outcome of talks between the Qube consortium, Asciano and Brookfield. For now, Qube is playing its cards close to its chest while it faces a range of outcomes which could have a variety of impacts on its balance sheet and profitability.

In the event that Qube gains control of the Patrick assets, the impact on profitability would come in FY17 at the earliest. Between this opportunity and Qube's transformation of the Moorebank terminal, it's clear that this is not a stock for investors with a short-term mindset.

Qube's opportunity at Moorebank alone makes this stock worth buying, but the potential upside from its pursuit of Patrick reinforces my view of this stock as one of the best long-term growth stories in the logistics sector. We maintain our buy rating and $2.95 valuation, and note that investors in this stock should keep some spare capacity in the event that they are invited to participate in a transformative capital raising.