What Holds should you Buy? Pt 2

Recommendation

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

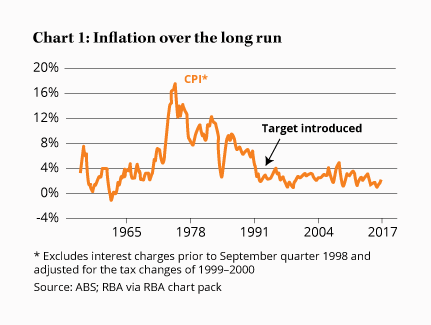

An astounding feature of the last decade has been the continuous presence of low-single-digit numbers. Even with the recent uptick in bond yields, Australian 10-year bonds still offer only 2.4%. A Commonwealth Bank five-year term deposit, meanwhile, delivers just 2.65% for amounts less than $50,000. But if you have a spare million, well, there's an extra 10 basis points on offer. Whoopee do.

Both figures make sense against the backdrop of Chart 1, which shows the rate of inflation over the past 50-odd years. As if you didn't know, great returns for savers are accompanied by out-of-control inflation. Now the world has the opposite problem. If anything, global inflation is too low.

Key Points

-

Hold are mildly underpriced

-

Might make sense to buy some Holds

-

But worth sticking to quality

The generalised response has been utterly predictable. With cash and bonds yielding not much, stocks have been the go-to asset for a half-decent return. Five years ago, the ASX 200 was trading at 4,048. Yesterday, it closed at 5,805, a 42% increase. The result has been many things, including a Buy List of only 11 stocks, with the notable absence of blue chips, and last week's story titled What Holds should you Buy? – Part 1.

The purpose of part one was to point you in the direction of a portfolio of stocks, many of which don't feature on the Buy List but still make for sensible buying. Here, we'll explain the thinking behind these selections in a little more detail before offering a synopsis of each stock in what we've called the ‘Holds to Buy mini-portfolio'.

Margin of safety

Between a Hold and a Buy recommendation exists a grey area more visible in times of low returns. Let's start with our Hold recommendations, all of which offer some value relative to cash (if that weren't the case they'd be Sells).

The difference between the two isn't as clear cut as might first appear. It really depends on how big a margin of safety you demand in your purchases. Hold recommendations are mildly underpriced. Sydney Airport, for example, is currently a Hold up to $10, a Sell above $10 and a Buy below $6.

Now, these numbers are misleadingly precise but, with a current share price of $7.47, there's a fair distance before we pull the Sell trigger on Sydney Airport. That point would be around fair value because, in the same way we like to buy undervalued stocks, we don't want to hold overvalued ones. The difference between the current price and the sell price therefore approximates to the margin of safety in the purchase. Research director James Carlisle puts it like this:

‘The point at which you buy to a large extent comes down to how greedy you want to be. When great opportunities are plentiful, you probably want to be very greedy, demanding a cheap price and a big margin of safety. But when opportunities are few and far between, as they are now, a fair price for a high-quality business is more easily justified.'

That proviso regarding high-quality businesses is important. If we are to accept a smaller margin of safety, which is what buying a Hold entails, we'll want to stick to higher quality stocks, which are less likely to produce nasty surprises. And if they provide a decent yield, to keep us in Tim Tams, then so much the better.

In the past we had a recommendation category for this type of somewhat undervalued quality stock – Long Term Buy. But people understandably wondered why all our Buys weren't long term (which of course they were and are), so to reduce confusion so we dispensed with the category and such stocks are now classified as Holds.

That, however, doesn't stop them from being good, reliable, income-based purchases for many members. That brings us to the 10 stocks in our mini-portfolio, designed to provide a collection of quality stocks, with a decent yield, in spite of most of them being Holds.

Amaysim (AYS) – Buy

| Price | $1.875 |

| FY17 expected dividend yield | 5.5% |

| FCF yield | 6.2% |

| Franking | Unfranked |

| Portfolio limit | 4% |

| Price Limit | Buy below $2.00, Hold up to $3.50 |

| Reasons for inclusion | High quality growth stock; good management. |

| Key risks | Competition in mobile market; big energy acquisition. |

Happily, this mobile virtual network operator is on our Buy List. Having built a subscriber base of over a million customers, the company recently purchased Click Energy on the basis that it could replicate its success in mobiles by cross-selling energy services. The ultimate ambition is to have three products – mobile, NBN and electricity – on a single platform with shared technology to market to a shared user base.

We aren't overly excited by the purchase but there's logic to their combination. And amaysim still appears inexpensive. In two years, the company could be generating about $500m in revenues and about $60m in earnings before interest, tax, depreciation and amortisation (EBITDA), delivering an adjusted enterprise value (EV) of about $480m and an EV/EBITDA of about eight times.

ASX (ASX) – Hold

| Price | $52.48 |

| FY17 expected dividend yield | 3.9% |

| FCF yield (last 12 months) | 4.0% |

| Franking | 100% |

| Portfolio limit | 8% |

| Price Limit | Buy up to $50, Hold up to $70 |

| Reasons for inclusion | Earnings set to grow; monopoly market position; |

| Key risks | Competition in equity clearing and potentially trading; major sharemarket weakness |

After several years of static earnings, ASX has finally got some growth back. In 2016, earnings grew 7% with 2% expected this year and 4% tipped to follow in 2018. That's not bad in the current environment, particularly for a stock of ASX's quality.

The growth is coming from the company's derivatives business and the much-maligned share trading operation, which is benefiting from increased trading, particularly on the higher margin Centre Point exchange.

ASX is travelling well and the market seems to be coming round to that view, hence the recent downgrade. But this remains a reasonably priced, top class business.

Flight Centre (FLT) – Hold

| Price | $37.70 |

| FY17 expected dividend yield | 3.5% |

| FCF yield (last 12 months) | 4.8% |

| Franking | 100% |

| Portfolio limit | 6% |

| Price Limit | Buy up to $32.00, Hold up to $50.00 |

| Reasons for inclusion | Strong market positions in Australian leisure and corporate travel; significant potential for overseas expansion and/or acquisitions; weaker players under pressure. |

| Key risks | Threat from online travel agents; recent weakness in airfare pricing; housing or consumer downturn. |

Flight Centre is one of the world's largest travel retailers, with more than 1,000 retail outlets across the English-speaking world and a rapidly growing corporate travel business with a presence in more than 50 countries.

This isn't a business that's going backwards either, despite the threat from online travel agents. Between 2011 and 2016 the company opened more than 400 stores in Australia and increased total transaction value by 40%. Flight Centre is reinventing itself over time, just as the best businesses do.

There's a risk 2017 profit comes up short of management's pre-tax profit target of $300m–330m but, with airfare deflation moderating, that now looks unlikely.

IOOF Holdings (IFL) – Hold

| Price | $9.895 |

| FY17 expected dividend yield | 5.2% |

| FCF yield (last 12 months) | 5.8% |

| Franking | 100% |

| Portfolio limit | 6% |

| Price Limit | Buy below $8.00, Hold up to $12.00 |

| Reasons for inclusion | Experiencing inflows; move to non-bank platforms; earnings to rise in 2018. |

| Key risks | Falling wealth management margins; earnings linked to equity markets; possible capital raising to fund acquisitions. |

IOOF is one of the few businesses in wealth management enjoying significant net fund inflows at the moment. Almost $1bn flowed in for the three months to March, making $2.4bn for the year to that date. About 90% of that went to the Advice and Platform businesses. Chief executive Chris Kelaher explained at the interim result that advisers were shifting from the big banks and AMP to IOOF due to the latter's open architecture and less bureaucratic approach.

We expected increasing funds under administration to offset falling industry margins. Earnings look set to fall around 7% in 2017 after a large number of customers were moved onto a more efficient platform. But cost savings should flow through in due course and, combined with inflows, earnings should start to rise again in 2018.

Navitas (NVT) – Buy

| Price | $4.55 |

| FY17 expected dividend yield | 4.3% |

| FCF yield (last 12 months) | 1.7% |

| Franking | 100% |

| Portfolio limit | 5% |

| Price Limit | Buy below $4.70, Hold up to $7.50 |

| Reasons for inclusion | Demand for education from international students; helps universities that are under funding pressure; strong cash flow. |

| Key risks | Loss of university contracts; government crackdowns on immigration or visa changes. |

| ^ NVT FCF yield should normalise around 6% – high capex this financial year as the company invests in its campuses | |

Education is Australia's third-largest export industry behind coal and iron ore, earning more than $20bn in export revenue. Navitas partners with universities in Australia and overseas, preparing international students for their degrees. The universities obtain access to a steady flow of international students, while the students are eased into university life at their chosen destination.

Due to recent contract loses, Navitas will report another year of flat EBITDA in 2018 (the company's fifth in a row). But this remains a top-notch business with favourable tailwinds, notwithstanding occasional contract losses and a difficult international migration climate. We believe the market is underpricing the stock, which is why we recently purchased Navitas for the Intelligent Investor Growth Portfolio.

Perpetual (PPT) – Hold

| Price | $55.52 |

| FY17 expected dividend yield | 4.9% |

| FCF yield (last 12 months) | 5.2% |

| Franking | 100% |

| Portfolio limit | 6% |

| Price Limit | Buy below $50.00, Hold up to $70.00 |

| Reasons for inclusion | High quality funds manager; proven track record; reasonable pricing. |

| Key risks | Sharemarket downturn; deterioration in investment performance. |

There aren't many stocks that stand to benefit more from a rising sharemarket than fund manager Perpetual. A 1% move in the index should translate into a revenue increase of about $2.5m, or about half a per cent. Given the business's relatively fixed cost base, that's likely to mean an increase in net profit of several times that. No wonder 2017 earnings forecasts have increased by about 12% over the past year.

Over time, markets go up and with its tried and tested value investing approach, we expect Perpetual to take its fair share. Conservatively, we'd expect that to add around 5% of long-term growth to the fully franked dividend yield of 4.9% – albeit with some lumps and bumps along the way.

Sydney Airport (SYD) – Hold

| Price | $7.45 |

| FY17 expected dividend yield | 4.4% |

| FCF yield (last 12 months) | 4.1% |

| Franking | Unfranked |

| Portfolio limit | 8% |

| Price Limit | Buy below $6.00, Hold up to $10.00 |

| Reasons for inclusion | Monopolistic business model; passenger growth; |

| Key risks | Rising interest rates; recession; China crash |

For a boring infrastructure stock, Sydney Airport has been showing plenty of growth. The distribution per security has risen at an average of 10% a year over the past five years, to a forecast 33.5 cents per share in 2017.

Passenger growth has grown reliably at a few per cent a year over decades (despite occasional short-term blips), as real air fares have fallen. Revenue growth then comes in a little higher because each passenger spends a little more in the airport, and earnings, cash flow and distribution growth come in ahead of that due to the company's relatively fixed cost base (not least from a large pile of debt).

The greatest threat is a rising interest bill on the company's $7.7bn of net debt. Around half of that is hedged against interest rate changes over the next five years, but beyond that every 1% rise in rates is likely to shave around 10% from free cash flow. Even so, the combination of growth and a 4.4% (unfranked) distribution yield make this an attractive long-term investment.

Trade Me (TME) – Buy

| Price | $4.895 |

| FY17 expected dividend yield | 3.5% |

| FCF yield (last 12 months) | 5.3% |

| Franking | Unfranked |

| Portfolio limit | 6% |

| Price Limit | Buy below $5.00, Hold up to $7.50 |

| Reasons for inclusion | Dominant position in New Zealand online classifieds; latent pricing power in some segments; cost growth slowing. |

| Key risks | Economic downturn would reduce transaction activity; new competitors could hit margins hard. |

We've had a long history with this online classifieds business, first recommending it on 19 Feb 14 (Buy – $3.54). Trade Me offers access to a portfolio of high-quality businesses with powerful network effects, all under one roof. Think of it as New Zealand's answer to eBay, REA Group, Seek and Carsales rolled into one.

EBITDA might struggle to match our aspirational target of NZ$160m this financial year but the company still lags its Australian peers when it comes to premium product revenue. There's a lot of upside as new staff start making their mark and cost growth slows.

Virtus Health (VRT) – Hold

| Price | $5.565 |

| FY17 expected dividend yield | 5.0% |

| FCF yield (last 12 months) | 7.5% |

| Franking | 100% |

| Portfolio limit | 5% |

| Price Limit | Buy below $5.50, Hold up to $9.00 |

| Reasons for inclusion | Women having kids later in life; emotional purchase; strong market position. |

| Key risks | Low-cost competition; slowing economy; reduction in Medicare reimbursement rates, fertility specialists leaving once off contract. |

This provider of assisted reproductive services was on our Buy List for quite a while until a share price run provoked a recent downgrade – although it remains very close to our Buy price.

Women are tending to have kids later in life as they build their careers, while a rising incidence of obesity and sexually transmitted diseases are making it harder to conceive. Moreover, having a child is the ultimate emotional purchase, one that people tend not to skimp on.

Along with Monash IVF and Genea, Virtus dominates the market with economies of scale that help it fund advertising and scientific research and lock up fertility specialists on long-term contracts. These are powerful advantages and, with plenty of free cash, the company has good long-term growth prospects.

Wesfarmers (WES) – Hold

| Price | $40.67 |

| FY17 expected dividend yield | 5.2% |

| FCF yield (last 12 months) | 5.5% |

| Franking | 100% |

| Portfolio limit | 8% |

| Price Limit | Buy up to $38.00, Hold up to $55.00 |

| Reasons for inclusion | Irreplaceable collection of great retail brands; excellent management and culture, focused on shareholder returns. |

| Key risks | Retail downturn; Amazon entry to Australia; acquisitions don't work out. |

Wesfarmers is a highly diversified conglomerate with retail interests that include Coles supermarkets as well as the Target, Kmart, Officeworks and Bunnings chains. It also has interests in insurance, coal mining, gas, chemicals and fertilisers, and industrial supplies distribution.

But the retail sector – responsible for more than 80% of the company's earnings – is on the nose and the negatives are intensifying. With historically strong sales and earnings growth from Coles, Bunnings and Kmart easing, there's pressure on management to identify a new source of growth.

Acquisitions may add risk but the company's focus on returns rather than empire-building is reassuring. Recent worries about the retailing sector don't change our view that Wesfarmers is one of Australia's 10 best businesses.

Note: The Intelligent Investor Growth Portfolio and Equity Income portfolios own shares in Amaysim, ASX, Flight Centre, IOOF, Navitas, Perpetual, Sydney Airport, Trade Me and Virtus Health. You can find out about investing directly in Intelligent Investor and InvestSMART portfolios by clicking here.

Disclosure: The author owns shares in ASX.

Recommendation