Qube breaks into the big time

First selected by Eureka Report in September 2014, ports company Qube is suddenly involved in some very big plans – it's also just released interim results so it's time for an update.

Sydney-based Qube runs diversified ports and transport operations and when it saw Canadian multinational Brookfield make a bid for ports and logistics giant some months ago Asciano it could not stand idly by to see what might happen next. (To see our last report on Qube, click here).

Consequently, Qube followed Brookfield's first bid for Asciano with an ambitious superior offer – As the Asciano group mulled two competing offers …Qube and Brookfield made the very pragmatic move to settle their rivalries and went to Asciano with a joint bid – that bid is now almost certain to go through.

There are three immediate items of note for Eureka Report:

1. We are re-iterating our buy call on Qube Holdings.

2. We are adjusting our valuation on Qube post results from $2.95 to $2.65, due to a delay in recovery for some of the company's key end markets.

3. If the deal is accepted by Asciano and all appropriate regulators approve it, then the deal will certainly be earnings accretive for QUBE, and we will increase our $2.65 valuation.

In a stroke, the new deal catapults the Qube group into the big time, taking a string of port assets off Asicano in a planned break-up of the company: It also means that the leadership team of Corrigan, his chief executive Maurice James and a string of top notch executives are back in charge of port assets they ran years ago at Patrick - the group which once upon a time took on the waterfront unions during the Howard government years.

Earlier this month the Asciano chief executive John Mullen announced he was stepping down (to go to Telstra as chairman). Mullen told the market he did not see a role for himself in a company that was no longer public: This comment suggests Mullen certainly believes the deal will go through, his comments relating to Asciano no longer being a public company refers to Brookfield not being listed on the ASX, while we can infer that the Corrigan/ James team at Qube will not have a role for him,

Qube jumped 10 per cent in a single session earlier this week but to be honest the stockprice has barely changed compared to the day Eureka picked it as a long term buy – of course, in relative terms that's better than many stocks on the ASX.

New AIO JV offer, and interim result

Short interest in Qube Logistics (QUB), had been building up as we approached today's interim result. The likely rationale was combined fears of weak customer demand in a majority of Qube's end markets, and the potential balance sheet impacts of Qube's recommended bid for Asciano (AIO).

At this stage it looks like short interest is wrong on both fronts. Yesterday it was announced that Qube, its consortium partners and Brookfield are working together on a joint proposal for Asciano (AIO). Assuming the proposal becomes binding, it will reduce regulatory risk (ACCC) and the acquisition price for Qube while still vitally enabling them to gain control of the Patrick Container Terminals business.

The Moorebank intermodal terminal opportunity will increasingly become a large part of Qube's business. Gaining part ownership and operational control of the ports container stevedoring assets, creates the opportunity for synergies as well as de-risking the Moorebank opportunity by gaining greater control of the container supply chain.

In terms of the half-year result, it was clear that as expected demand has declined across the board due to generally weak end markets. This was especially the case with oil and gas and mining. But the strength and efficiency of Qube's service offering means their margins aren't exposed to the same downside leverage as a typical mining services company.

The team is still continuing to win market share, as well as implement new initiatives to cut costs. Importantly strong free cash flow is being achieved to internally fund all capex and interest requirements. A key component of the Qube business model is re-investing in its assets, and they have maintained this focus alongside their efforts to acquire Asciano's ports business. The downturn will also create the opportunity to acquire distressed competitors, and generally position the business to grow strongly when end markets eventually pick-up.

The Qube management team has done an excellent job in building up a diversified logistics business in fast time, but the key missing link has always been container stevedoring. Not only does Asciano's ports business (Patrick) fit very well in the Qube stable, but there is also the added bonus that many of the current management team previously ran the Patrick business. Current Qube Managing Director Maurice James was formerly an Executive Director and Head of the Ports Group at Patrick for approximately 10 years. Current Qube Chairman in Chris Corrigan was Managing Director of Patrick, and played a key role in training and mentoring many of the current Qube management team.

JV Proposal (Qube, Brookfield and partners)

Before yesterday, it looked likely that Qube and its consortium partners had won the bidding war against Brookfield for ownership of Asciano (AIO).

But yesterday details were revealed of the Qube consortium joining with Brookfield Infrastructure in a $9.28 per share all cash proposal to acquire Asciano (AIO) by way of a scheme of arrangement. The new proposal looks like a win for all concerned. Asciano shareholders are likely to be happier with an all cash bid, as well as the reduced regulatory risk of the offer.

Qube and Brookfield both have a similar view of the benefits from owning and investing in the Container Ports Terminals business, and the reduced capital cost for Qube is a positive given it is still a very big acquisition relative to Qube's $2.4 billion market cap.

The offer is not binding yet, with some conditions to be finalised. However the Patrick Container Terminals business will become a 50/50 joint venture with Qube and Brookfield (and its consortium) at a cost of $2,915 million (Qube's share: $1,457.5m).

The independent expert valued Patrick at between $2.3bn and $2.5bn, implying 10-11 times FY15 EBITDA. Asciano's FY15 revenue of $3.86bn was broken up into the following - $705m for Bulk and Auto, $749m for Terminals and Logistics, and $2.43b for Pacific National.

The synergy benefits for the JV are expected to be consistent with what Qube previously identified ($30-50m). Additionally Qube will benefit from Brookfields international container terminal footprint and other international opportunities.

Brookfield Infrastructure (and consortium) will acquire the Bulk and Automotive Ports Services businesses, including the 50 per cent interest in Australian Amalgamated Terminals (AAT). Qube will have an option to acquire this 50 per cent AAT stake from Brookfield, subject to ACCC clearance for a cost of $150m.

Global Infrastructure Management (GIP), Canada Pension Plan Investment Board (CPPIB), CIC Capital Corporation (CIC Capital) and certain members of the Brookfield consortium would acquire the Pacific National rail business (Pacific National).

Brookfield has already cashed its $88m break-fee from Asciano, after the AIO board opted out of the Brookfield offer for Qube's superior offer. If this JV bid is successful, then it's unlikely that AIO will be paying QUB a break-fee for its previously recommended offer on the February 16 2016.

The new proposal reduces some of the prior complexity, and is very well thought out to address the issues previously raised by the ACCC.

Importantly after funding costs, Qube expects the transaction will remain highly accretive on a pro-forma basis.

Qube's capital requirements of $1457.5m (pre transaction costs) will be met through a combination of non-recourse debt funding within the new Patrick Container Terminals joint venture, additional Qube debt funding and a Qube equity raising.

The equity raising of $600-800m will comprise a fully underwritten accelerated entitlement offer, and CPPIB taking up an amount of up to 9.9 percent of Qube's expanded issued capital. Importantly this structure enables existing shareholders to participate as well as introducing another large strategic investor to the register.

As part of the transaction, Qube will exit its existing AIO shareholding at the offer price, with the $569 gross proceeds reducing existing debt and recognising a profit of around $35m.

The gearing reported in today's result of 42 per cent is slightly above its target range of 30-40 per cent. But following the completion of this transaction, gearing will fall back within its target range and able to fund the continued growth in its business, including the transformational Moorebank project.

Qube's long-term interest in Patrick

Arguably Patrick's former management team who are now the core of the Qube management are better placed to grow the ports business than the current AIO team. But the opportunity is not only investing in the ports and improving performance, but also the efficiencies that will be gained from combining it with the existing Qube operations.

The core to Qube's strategy is efficiency gains through fragmented port related supply chains. Given the past success of this strategy, it makes a lot of sense to add another major part of the container terminal chain.

It also makes sense not to let the key asset fall into competitors' hands. Qube relies on the cost effectiveness of its port providers, and the best way to remove this risk is operate it themselves.

Although Qube will integrate its facilities with the Patrick container terminals in Melbourne, Brisbane and Fremantle, it is the Sydney based Port Botany terminal where there is the most to gain. Firstly Qube currently operates a majority of the container rail volumes from Port Botany. Further, NSW Ports plans to triple throughput volumes over the next 30 years.

There are already capacity constraints, so the large increase in forecast volumes means the container chain in New South Years urgently needs additional infrastructure. Qube is already positioning to play a large part in this through the large Moorebank intermodal terminals that will ramp up volumes over the next decade.

So alongside the short-term synergy benefits, there are additional long term strategic benefits from owning the important Patrick terminals.

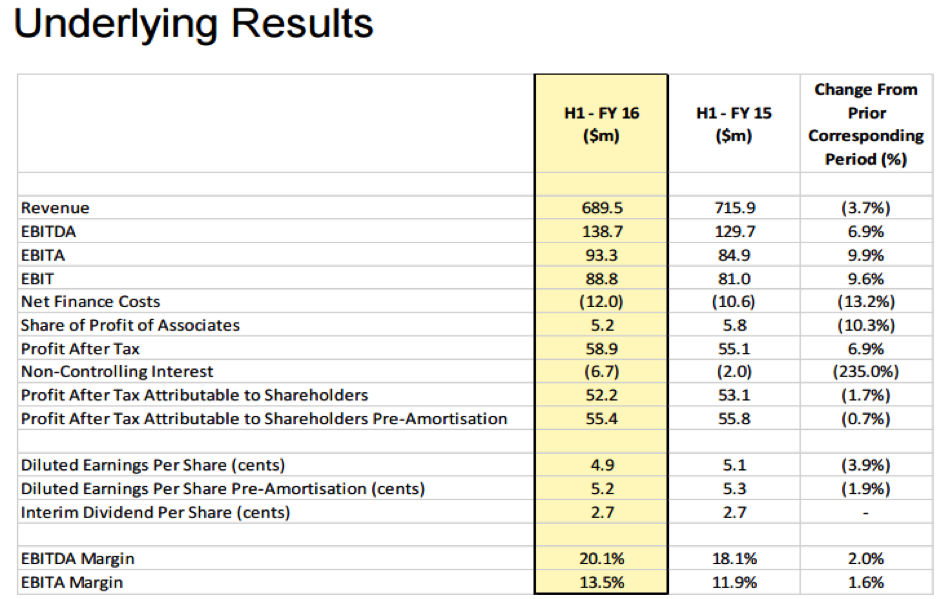

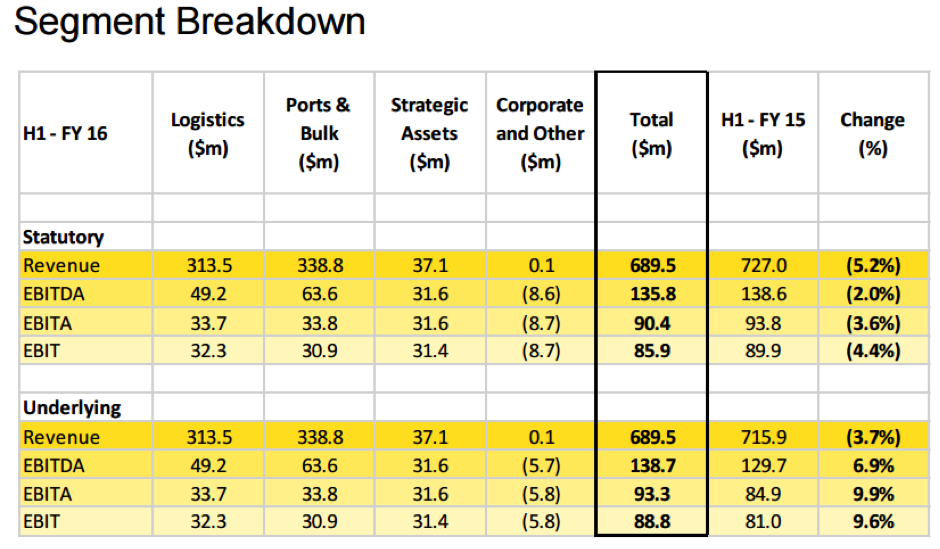

Half-year result detail

It was no surprise to see a volume impact from the half year result with weaker mining and oil and gas markets. The important component was that management has been able to reduce costs and deliver operational efficiency gains to partly mitigate the lower volumes and revenue.

The company had previously highlighted four problem contracts including Atlas Iron (AGO) and Arrium (ARI), but importantly there were no further major customer losses in the half. A constant focus on improved innovative solutions ensures they are well placed to continue winning market share.

Moorebank plans are progressing well, with the early lease surrender of the tenant (Department of Defence). Although it means the loss of a good tenant, it's a major positive for the ongoing planning with Moorebank. That is, it gives management the opportunity to start leasing warehousing space to new strategically important customers. Although there will be a loss of rental income for the second half of FY16, this will be partly reinstated from the start of FY17.

In logistics underlying earnings growth was achieved, with margin growth from operational improvements, and instillation of new facilities. Growth in the customer base has helped offset declining volumes from existing customers. Quattro Grain will commence operation from March 2016, with a material earnings impact from the beginning of FY17.

The Ports & Bulk division was impacted by reduced revenue from previously announced contract completion / amendments in the second half of FY15. The division had pockets of strength including vehicle imports and log exports, but weakness in bulk volumes. Qube has the opportunity to enhance relationships with existing customers by working closely with them to re-engineer logistics activities to reduce costs and deliver required returns.

Summary

In terms of the outlook, management expect broadly similar operational conditions in the second half. This means no improvement in the weak resources and oil and gas markets.

We have reduced our prior $2.95 valuation to $2.65, primarily due to delaying the timing of recovery in some of Qube's key markets. But if the AIO proposal is successful it will increase our valuation with short and long term benefits – both strategically and accretive earnings on a pro-forma basis.

We continue to view Qube as a compelling long-term investment, with a decade of strong growth to start flowing from Moorebank in FY17/FY18. Maintain the BUY recommendation with $2.65 valuation/target price.