Credit Corp hits income sweet spot

At Tuesday's market open we will take a 6 per cent stake in the Income First model portfolio.

Credit Crop Group Limited (CCP) is a business engaged in the collection of aged receivables, as well as the provision of consumer loans. The lending business is relatively new in terms of its materiality driving growth, but CCP has been in the business of buying aged receivables (Purchased Debt Ledgers, or PDLs) for some time, holding Australia's largest market share. The company has no official payout ratio disclosed to the market, but over recent years has paid around 50 per cent of underlying net profits to shareholders as dividends, and has paid 45 cents in the last 12 months. This equates to a trailing dividend yield of over 4.5 per cent, using a share price of around $9.60 (about 6.5 per cent, if franking value is included). Given that the company has a strong track record for growing dividends, and is well placed to continue to grow profits and dividends in step, the prospective dividend yield is quite strong. The stock is operating in an attractive space with a strong market position, and we are comfortable taking a 6 per cent position in the Income First model portfolio. There is upside in our view to the current share price as the company completes a record year of investment in PDLs and is also building its loan book. This bodes well for FY17 and beyond as this year's purchases will result in profits and collections in coming years.

Overall, CCP meets the profile of the stock we are looking for in that the company pays a strong dividend yield, but at a payout ratio that affords the ability to reinvest when opportunities present. Recent changes in competitive forces have allowed CCP to invest in growth and this should manifest in higher profits in FY17 and beyond.

Dividends and cash flow

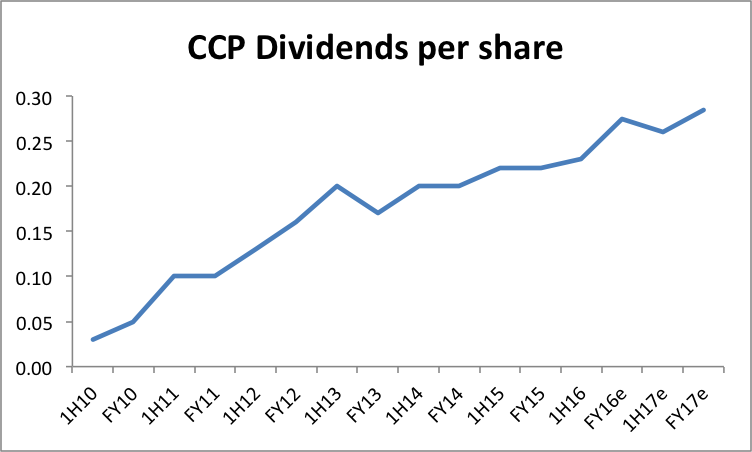

When discussing the matter with Credit Corp management, I became aware that the company does not have an official dividend payout target. The idea here is that the board sets the dividend with consideration to the investment needs and capital requirements of the operations. Effectively if the company sees strong opportunities to invest and meet targeted returns, then capital will be directed to reinvestment in operations. However, a clear pattern has emerged in the last few years that shows a dividend payout ratio just over 50 per cent of net profit. Additionally, the dividends have been growing at a similar pace to earnings, suggesting that there is a willingness and ability to pay higher dividends as the business grows and still reinvest into operations at a pace that affords future growth.

Here's a chart of the company's dividends since the start of FY10:

Purchased Debt Ledgers are the bread and butter

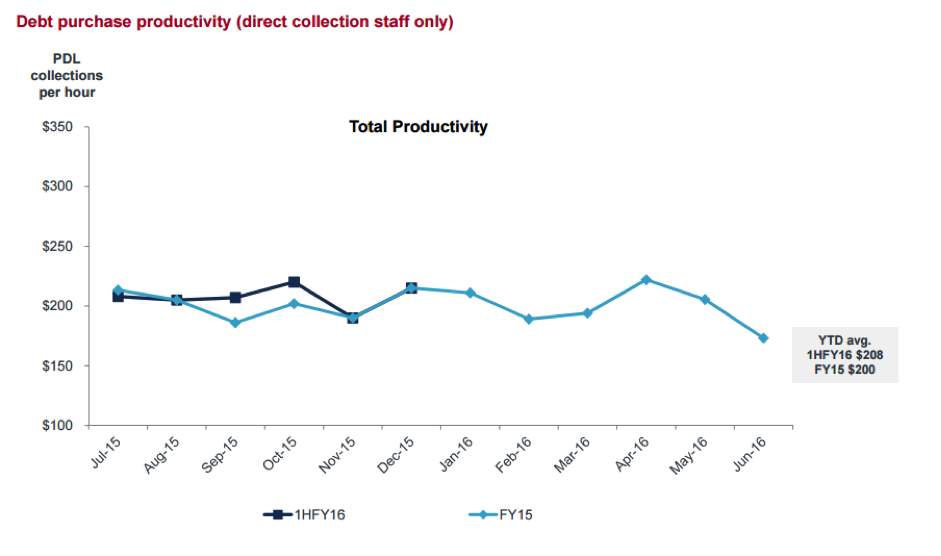

The bulk of CCP's business is the acquisition of Purchased Debt Ledgers, and the collection of these receivables. For the most part, this is 180-day arrears credit card debt, but also includes telco debt and other personal loans in arears. The company holds the largest market share in Australia, and has a competitive edge by virtue of its efficiency in collections. Underlying this, CCP provides an efficiency measure in it financial presentations that show the collections productivity, using dollars collected per hour from ledgers:

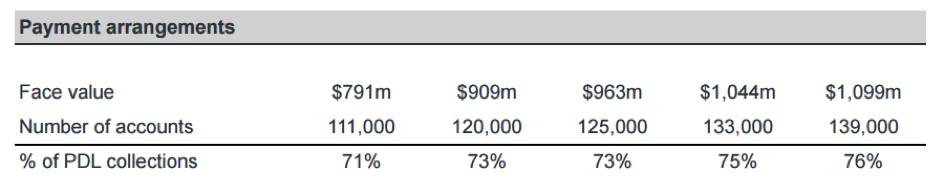

From an operating perspective, CCP is quite strong. The company has longstanding collection efficiency, along with an ability to place collections onto recurring payment plans. At the end of the first half, 76 per cent of collections were sourced through these payment plans, and this proportion has been increasing for some time:

In recent times, the PDL market has been quite competitive, and a key driver of profitability in future years has been the company's ability to purchase fresh PDLs for an acceptable price. The price is determined through a bid process, so competition is key. Pleasingly, CCP has been purchasing increasing levels of PDL with this year's purchases expected to be a record $185 million - $195m. The reason for such a large level of purchasing is that the market has seen some changing dynamics in FY16. Key competitor Collection House (CLH) has been purchasing at rates higher than operating cash flow for some years, leading to an inevitable need to pullback and reduce spending. In our view this has created an opportunity for CCP to take additional market share, and goes a long way to explain the increase in PDL acquisition guidance for FY16.

The PDL segment of CCP in Australia remains the core of the company's earnings. We take confidence in the fact that purchasing guidance has been upgraded, as this year's strong purchases will set up the company well for increased collections and profits in FY17.

Consumer lending

CCP has been building its products in the personal lending space through brands including Wallet Wizard, CarStart, MoneyStart and ClearCash. The focus here was initially to utilise the business' extensive database of distressed borrowers accumulated through the PDL collections business, and originate fresh loans for these customers that may not be able to directly access traditional personal finance due to weak credit ratings. You might recall that this is an area of the market that I believe affords good opportunity, and I have written on this in the past (to read more, click here).

CCP has guidance for net lending book growth of $32m in FY16, and has been growing the book significantly in recent years. It should be noted that two factors make the company's profile attractive as a result. Firstly, the accounting policy is to impair or provision loans upfront, meaning that a growing book has a negative impact on current year profit and loss (an accounting nuance). This year CCP is expecting the growth to moderate and notes that the cash flow from the book is at a point that it is close to self-funding for future growth (an important consideration when you observe that CCP has taken on some debt to grow this part of the business). Secondly, the slower growth rate in the second half of FY16 and into FY17 is likely to catalyse strong accounting profit growth. In this light, the company is in my opinion poised to see strong growth in lending book profits as a result of the lower growth rate in new loans. This could see CCP's net profit result for FY16 and FY17 deliver additional strength.

US operations

CCP has had a small loss making presence in the United States (of approximately -$2 million in the past year). The market in the US is huge, and complex, with regulatory flux in existence. This regulatory flux has caused banks to withdraw from the market and freeze the sale of PDLs for some time. However, with some regulatory clarity starting to emerge, there is an expectation that CCP's US operations will reach break even in FY17. Growth here has been a slow grind, and the operations have been moved from California to Utah as CCP seeks efficiency in a new market. Despite this, management's strategy of establishing a presence and waiting for market clarity to provide an opportunity appears a good one. It has certainly taken a long time, and longer than I expected, but if the market in the US starts to see increased certainty and volume, CCP may be well placed for additional growth. At this stage we don't value the US operations when considering upside, but note that there is an increasing focus here. The uplift in purchasing guidance for FY16 is representative of increased purchasing in the US. This increased US investment will lower returns, but will likely drive the US towards break even in FY17.

Regulatory risks

As can be seen from the company's experience in the US, regulatory issues are a significant issue in both collections and lending markets. Recently, the company withdrew from short-term loans or small amount credit contract (SACC) after regulators and funding and payments stakeholders questioned and even withdrew support for the market – under connotations to what is known as payday lending. In our view, this recent regulatory change has had significant impacts for companies such as Money3 (MNY) and Cash Converters (CCV), whereas CCP's exposure in this space was smaller. Despite our view that this incidence does not materially impact the investment case, it is a stern reminder that there are regulatory risks apparent, something investors should consider.

Under promise and over deliver – an excellent management track record

Since the start of FY12, CCP has upgraded or beaten full year net profit guidance on nine occasions. This is indicative of the management style that has been instilled since the GFC. CCP management now have built a recurring record to under promise and over deliver when it comes to net profit – something shareholders should be quite pleased with. The below table shows the profit guidance and upgrades over the past five years.

Initial Guidance | AGM | Half year | Update | Actual | |

FY12 | $21-$23 | $23-$25m | $25-$27m | none | $26.6m |

FY13 | $27-$29m | $27-$29m | $27-$29m | none | $29.9m |

FY14 | $31-$33m | $31-$33m | $33-$35m | $34-$35m | $34.8m |

FY15 | $36-$38m | $36-$38m | $36-$38m | $37-$38m | $38.4m |

FY16 | $40-$42m | $42-$44m | $44-$45m | n/a | n/a |

Given the trends in CCP's lending division and the record PDL acquisitions expected in FY16, it is fair to expect that this trend for higher profits will continue at least through FY17, barring any unforeseen events.

Outlook and competitive risks

I have discussed the guidance numbers for CCP, and am comfortable that the company is well placed in the short to mid-term. However, it is important to consider that the PDL market in Australia is a competitive one, and remains CCP's core earner. At the end of September last year, US listed Encore Capital Group (Nasdaq: ECPG) purchased 50.25 per cent ownership of one of CCP's key competitors, Baycorp. Potentially, this could led to investment in Baycorp and drive additional competition in the market for PDLs. Effectively, the higher the price at which PDLs are acquired, the lower the returns that CCP can generate on invested capital. Unfortunately the market is quite opaque when it comes to pricing and to competitive forces. CCP and CLH provide some anecdotal evidence of the market, but in general it is difficult to foresee. Given this uncertainty and the opaqueness of the supply and demand outlook, competitive forces, particularly through Baycorp's potential push for further scale is a key risk to the mid to long term outlook.

Notwithstanding this key risk, it is important to focus on what we can see in the market. CCP's closest listed competitor, Collection House Limited (CLH) has recently provided commentary suggesting that PDL prices have risen by around 5 per cent to eight per cent during FY15, and pulled away from high levels of purchasing. While this is a negative message for the market and returns from PDL collections, I believe that CCP's competitive advantage lies in its collections efficiency in Australia. This allows CCP to generate its target returns on purchases made at a higher price than competitors.

Given the strong purchasing guidance for PDLs, the potential for a $2m NPAT drag in the US to become a breakeven result in FY17 and the profit growth likely to come from the consumer lending book, I am comfortable initiating coverage on CCP with a buy call and an initial valuation of $11.56. Currently the share price represents a forward PE of around 10 times FY16 guidance. Given the expectation that growth will continue in FY17, the one year forward PE is under 10 and the stock appears cheap. With a strong dividend yield and a growing stream of DPS, the company represents an attractive opportunity.

To view Credit Corp Group's forecast and financial summary, click here.