The markets caught in the middle

Summary: Asian stocks are being roiled over growing trade war concerns. When China sneezes, others surrounding seem to catch colds.

Key take-out: Retail investors may look to these leading indicators when trying to gauge the pulse of Asian emerging markets.

While most of Asia was on holiday, treasury yields spiked again, begging the question – what will it take for emerging Asia to come back into flavour?

JPMorgan has joined the banking chorus that’s cautious about China, and this week upped its bets there could be a “full-blown trade war” between the US and China next year. It’s now the bank’s ‘base case’ scenario. They’re the world’s largest economies, so this would have clear ramifications throughout the regions.

State Street’s new head of Global Markets for Asia-Pacific, Michele Hardeman (pictured right), told Eureka Report this boils down to the US changing tack. In her view, it stems back to the Trump Administration moving away from multilateral negotiations and basically engaging in bilateral negotiations directly with individual members of the APAC (Asia Pacific) community, while taking the same approach when dealing with Mexico and Canada too.

“That is spilling over into the softening of trade values, and in that environment, people do get nervous about their risk assets,” says Hardeman.

“As much as emerging markets and APAC, things might be really progressing with these economies, in some situations, they are still in embryonic circumstances.

“The trade war is problematic, and there is an element at some level that some of Trump’s concerns are probably justified, but the method in which he is trying to effect change is fairly unusual and very drastic.”

Hardeman doesn’t offer a view about what will incentivise investors to go back into emerging markets. She does think investors should watch world trade volumes, and remember that, whatever the impact, “Australia won’t be left in isolation”.

InvestSMART Chief Market Strategist Evan Lucas thinks, on a granular level, there's already pockets of value to be found in Asia considering the severity of the sell-off.

'Average' not 'cheap'

Emerging markets equities, in particular, are caught up in the tension, as their counterpart credit markets seem to be heading in a more positive direction. At least that’s what Morgan Stanley strategists think. In terms of valuations, the bank thinks emerging markets stocks right now are ‘average’ not ‘cheap’:

“And relative to other equity or other fixed income markets, the difference is even more stark; there are plenty of global equity markets that offer similar or cheaper historical valuations than EM stocks: That's not the case for EM fixed income, including both hard currency and local currency debt.”

Earnings estimates may still be elevated, believe the strategists, and trade tensions present further downside risk. Yet, credit is “tied to a better sovereign picture” considering recent corrections we’ve seen in current account deficits and expectations of a weaker US dollar, among other things.

Plus, in periods of stress, stocks in emerging markets seem to fare much worse than sovereign debt.

Some things would turn the investment banks more bullish about the prospects for emerging markets equities. And the average investor can easily look out for some of these cues too.

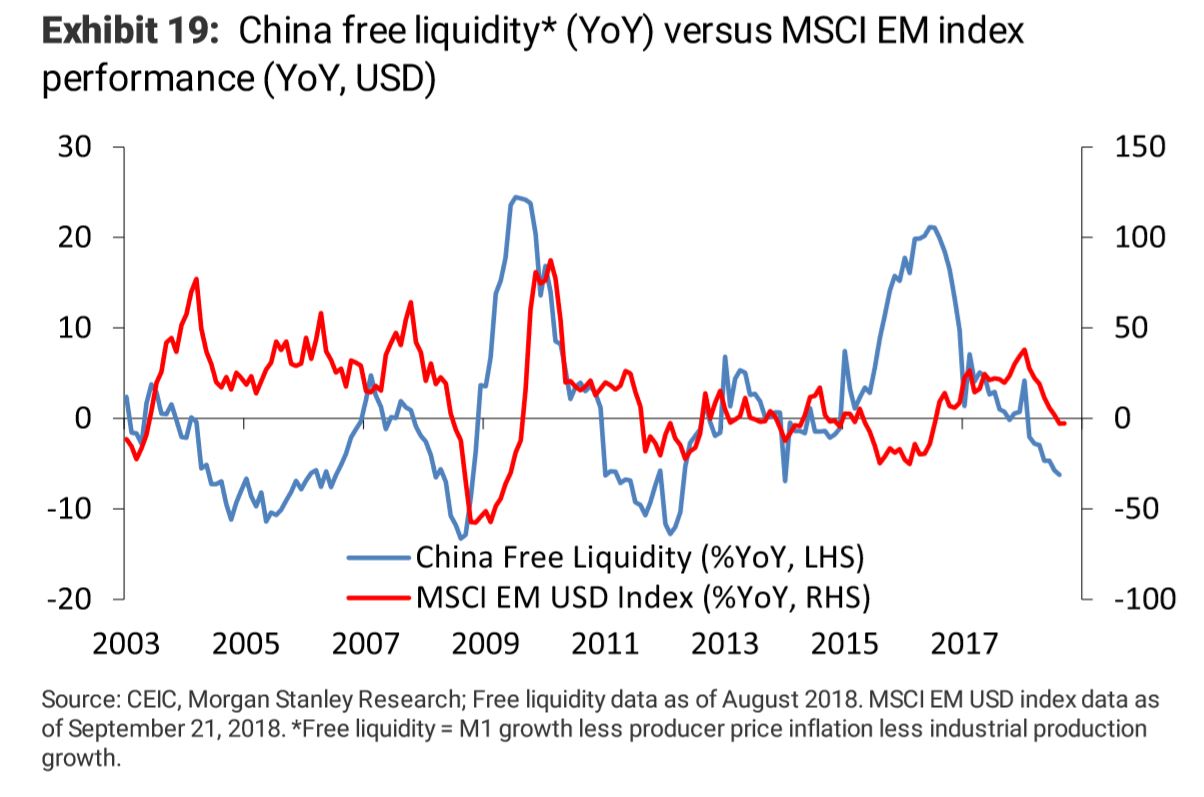

Focus on China free liquidity, and select sectors

Looking at China free liquidity is a good place to start. Morgan Stanley strategists describe this metric as a “good lead indicator of transmission to the real economy”.

For Asian emerging markets to re-establish positive year-on-year performance, the bank says China free liquidity would typically need to improve for several months. Here’s a chart showing where it’s at now:

Semiconductors and autos are also of great importance to Asian emerging markets. The investment bank suggests a break-out in these sectors could significantly alter the course of the broader market:

“It is noteworthy that even as risk markets were somewhat stronger last year, the SOX (semiconductor) index did not participate in the upside. While Chinese auto stocks did participate to some extent, Korean auto stocks were only very modestly higher.”

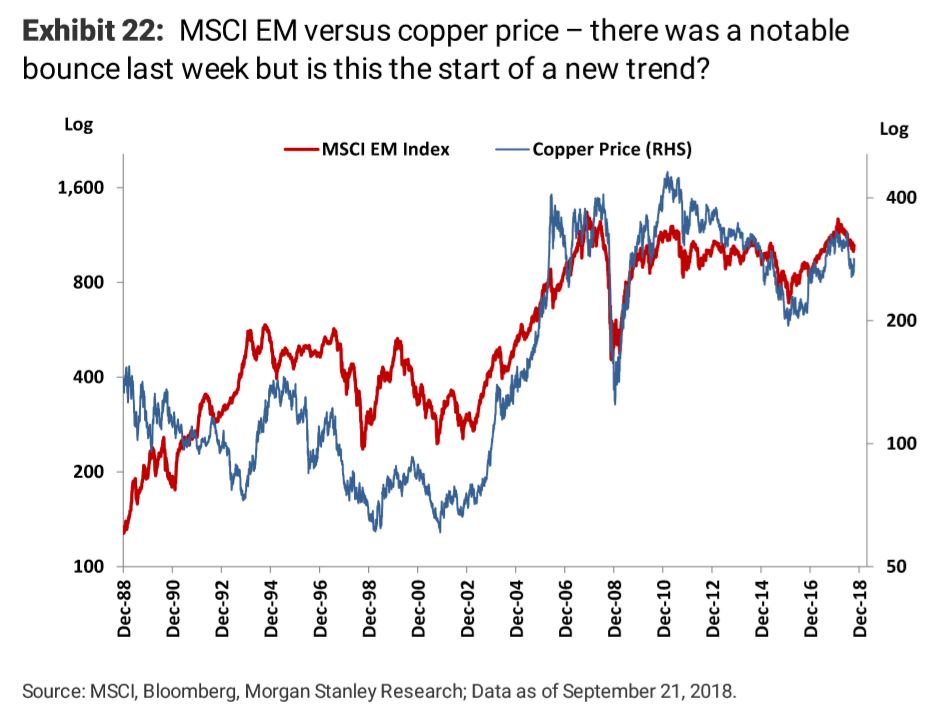

Check in with Dr Copper

Dr Copper is another leading indicator for emerging Asia. Copper is a core indicator for Chinese growth, which generally precedes the rest of the region.

The copper price in Chicago fell as much as 16 per cent at the height of US-China tensions, however it bounced once the final proposal was released by the Trump Administration.

In recent trading sessions, copper has been encouraging some emerging markets bulls, but it’s still early days.

But let’s remember, we’re coming off a period where we experienced one of the largest sustained inflows into emerging markets in their history. The period from January 2017 to April 2018 saw more than $US147 billion of inflows to emerging markets exchange-traded funds and actively managed products worldwide.

Sharper, more sophisticated tools

Most of these markets did well over this period, yet to varying degrees. And that’s why the more sophisticated investor may use sharper tools when trying to find the pulse of not just "Mr Market", but individual markets within a region.

Hardeman says State Street has provided media sentiment indicators for a couple of years, however they were focused exclusively on individual companies. Given State Street’s capabilities coupled with the demand, State Street introduced media sentiment indicators for countries and currencies last month.

The tool now pulls data from more than 100,000 traditional and social media sources to create indicators that measure abnormal intensity, conditional sentiment and level of disagreement. It’s covering 33 currencies and 44 countries.

Of course, this is more ‘real-time’ than a ‘leading indicator’ could ever be – but for now, at least retail investors still have other ways to get a handle on the flavour of the market.