Tall poppy syndrome hits home

Summary: If Hillary Clinton wins the Democratic nomination, the global banks in New York will be under attack. In Australia, the high fees that big banks are charging for wealth management will be in focus. Coal miners are also under attack but they have only themselves to blame as they should have invested in carbon capture technology. And Greece in the past behaved in a very cavalier way and is now paying with a severe recession. |

Key take-out: I think the nervousness around a possible Greek exit from the euro is an opportunity, although it is very hard to pick the bottom. |

Key beneficiaries: General investors. Category: Economics and investment strategy. |

We are entering into a period of history where tall poppies are going to face challenges that they have never experienced before and in the process that is going to affect investment strategies.

Part of the reason for the attack on society's tall poppies is that western communities are being hollowed out with less in the middle class and more at the higher and lower ends of the income spectrum.

It looks as though the biggest tall poppy attack will come in the United States presidential election as Wall Street investment banks are being set up to be hit. But in Australia banks are also in the gun and are starting to respond by asset sales. But our biggest tall poppies in line to be hit are the coal mines. And finally there is the tall poppy taken down many years ago – the Greeks.

The US is leading the world in the contraction of its middle class and it is becoming harder and harder to achieve the great American dream. Nevertheless I was surprised to see that the central theme of Hillary Clinton's thrust for the Democratic nomination was a planned attack on Wall Street and in particular Wall Street securities traders such as hedge funds. That is the sort of attack that you would expect from those seeking to challenge the front runner but Hillary Clinton has felt the pulse of Americans who have been completely revolted by the enormous fines paid by the big banks for manipulating the currency markets and the fact that the people who committed those crimes are still collecting their annual enormous bonuses instead of long jail sentences.

Assuming Hillary Clinton wins the Democratic nomination and she continues this theme then the big global banks located in New York are going to have a tough time as will those traders who have special pipes into the market so they can get the inside running.

Of course the Clintons have been at the top of the power tree for a long time in the US. They are a wealthy family and should Hillary Clinton win the nomination in a bruising election campaign the Wall Street forces will spend large sums examining minutely every aspect of the Clintons' finances. The Clintons had better stand the scrutiny or Hillary Clinton will be the tall poppy that gets cut down.

Big banks don't dominate the American share market as they do in Australia but have no doubt that an attack on Wall Street will affect the long term American share market.

Could we have a similar situation in Australia? I think the answer is yes but it won't be concentrated on market manipulation but rather on the high fees the big banks and others are charging for wealth management. The fact that the accountancy association CPA Australia has now entered the advice market is highly significant.

CBA, NAB and to a lesser extent Westpac all made big thrusts into wealth management operations which were based on high fee charges. It has not been a happy experience and each of the banks is going to need to work very hard to establish models that make money and justify the large book values these financial planning and insurance businesses carry.

Westpac's thrust into BT Investment Management was executed at a time when BT was down so the price was cheap. But the bank has decided to sell part of the asset so as to improve its capital position. It would never have done that if BT had performed as expected.

But in Australia and in many other parts of the world the biggest tall poppy being attacked is the coal industry. Coal miners have only themselves to blame. The climate change argument has been promoted heavily in the schools and is now widely accepted in the community.

Indeed the writing was firmly placed on the wall in February 2013 when China announced it would seriously cut emissions and of course we conveyed that to Eureka Report readers a few days later (see China and super: Big changes afoot, February 8, 2013).

In many ways the coal industry has been like so many industries that have not used their high profits to adapt the way they do things to the modern environment.

So when coal was churning out cash companies like BHP, Rio Tinto and other coal miners should have been investing heavily in better burning processes or carbon capture. Instead the coal mining profits went onto new coal capacity or to other mining ventures. Some of it went to shareholders.

A key part of the carbon reduction plans of federal Environment Minister Greg Hunt is to use better technologies to burn brown coal in Victoria in a way that slashes emissions dramatically. This should have been done a long time ago.

Because the industry didn't take the lead in these areas the industry is very much on the community nose and will struggle to survive (see Will you be the last one out of coal?, May 27).

Probably the smartest “coal miner” in the country is Gina Rinehart who sold her majority stake in the Galilee basin coal reserves to the Indians for a highly inflated price. Of course she used the money to provide capital for the Roy Hill iron ore mine which would now have a market value well below what Gina Rinehart paid. But iron ore is a better investment than coal.

It is a great shame that one of Australia's successful industrial stocks Wesfarmers held onto its coal mines far too long. They could have been sold at a very good price. The rundown of the Australian coal industry will be a big blow to Australia's three eastern states because coal plays a big part in their economic strength.

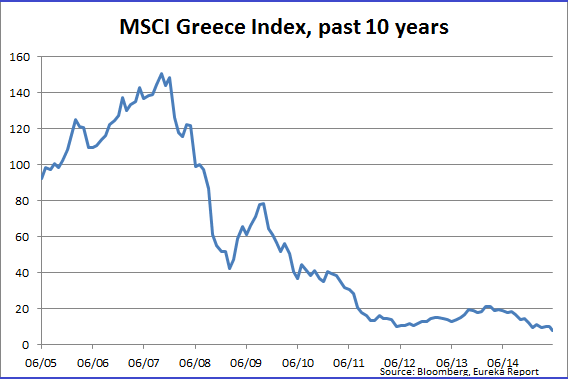

My final tall poppy is Greece but that stretches the bow. I am fascinated by what looks like being the last chapter in the Greek saga (for more on Greece, see Adam Carr's piece today: Is it time to worry about Greece ... again?).

The simple fact is that the Greeks behaved in the European community in a very cavalier way often being advised by global banks as to how to rig the figures. They are now paying with a severe recession but in the process they have actually lost their bargaining power and Europe is almost ambivalent as to whether Greece stays in the euro or leaves it. In the last 24 hours European share markets rose while Greece fell. Nevertheless the markets are very nervous about a Greek exit from the euro but certainly the people I speak to indicate that Greece's exit can be managed very well.

As I mentioned last week I think that the nervousness is a buy opportunity although like all buying on the way down it is very hard to pick the bottom. I still think there is a 60 per cent chance Greece will stay in the euro which will bounce markets. But if Greece does exit the euro the initial reaction is not likely to be favourable for the market. For Greece an exit will mean a deep depression but longer term both Greece and Europe will be better for the exit.

And one more point, back a decade ago we looked at the European system of shared control and thought the American market-based democratic model was far superior. But if America institutes major curbs on Wall Street then the old American rule the market knows best will have been severely damaged.