Matching jobs growth to company valuations

Summary: Labour market figures can help investors determine which companies are investing in their future. |

Key take-out: Firms that aren't investing or preparing for the future are unlikely to experience the type of earnings growth that will justify higher valuations. |

Key beneficiaries: General investors. Category: Economics. |

Australian employment has increased by 212,300 people over the past 12 months.

It's a result that is certainly not as stellar as the gains experienced during the commodity price boom; nor is it a result befitting an economy with a cash rate of 1.5 per cent.

Investors would be excused for being confused about the state of the Australian economy. Are conditions improving or deteriorating? The data suggests that traditional measures of economic growth may be misleading and employment growth is being driven by part-time and casual work rather than high-quality full-time roles.

The disconnect between inflation and growth

Rarely in our history have we experienced a combination of such low inflation and interest rates while simultaneously maintaining above-trend economic growth and solid employment. Normally low inflation is associated with below trend growth and rising unemployment. Above-trend growth normally points towards higher interest rates.

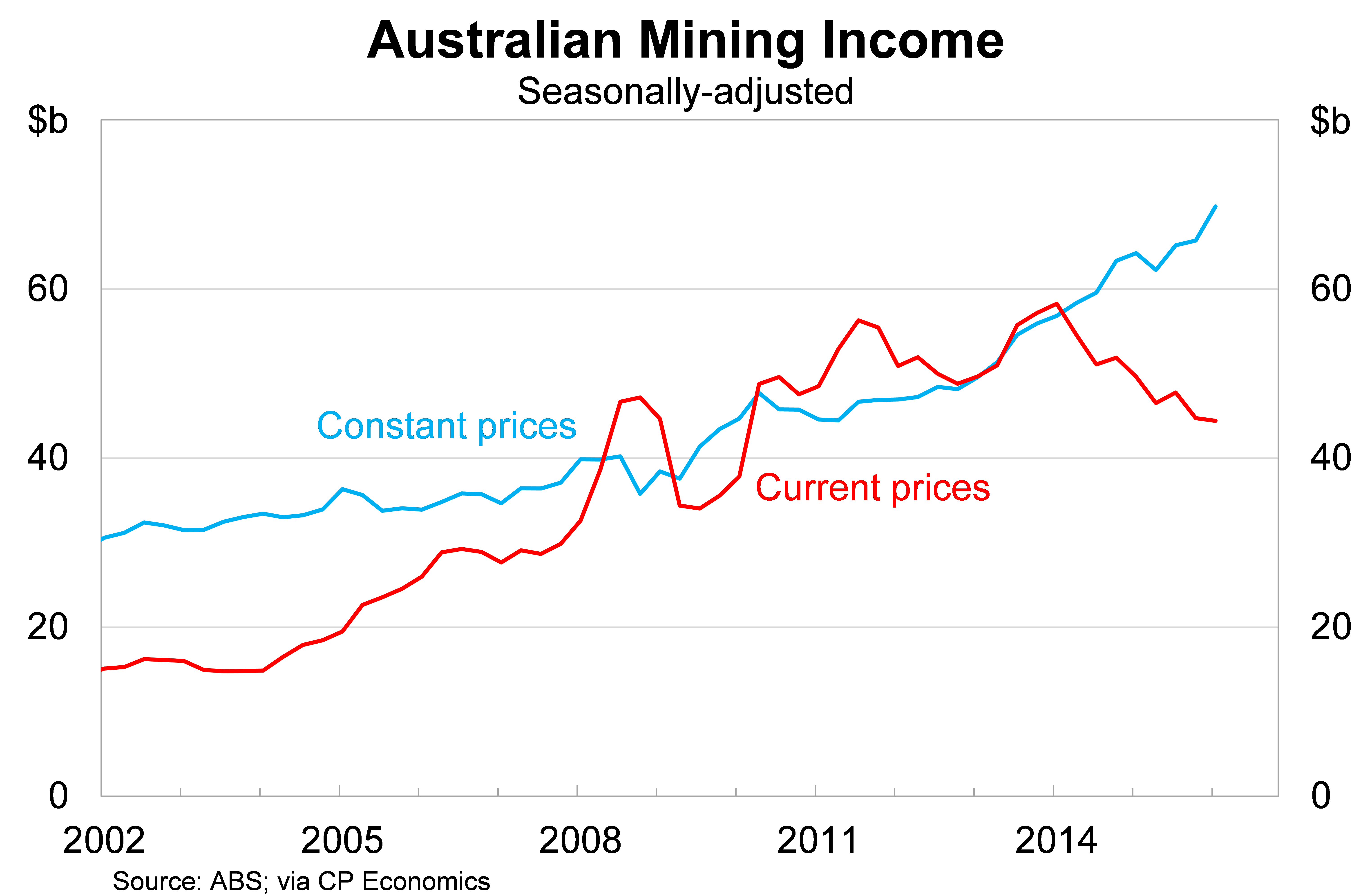

The disconnect between inflation and economic growth began three years ago when commodity prices, particularly iron ore and coal, began to fall. This initially hit mining income and profits but has since spilled over into other sectors of the economy.

The impact can be seen quite clearly in the graph below. It basically shows the income earned from mining activities against what those earnings would be if prices were unchanged. The latter is included in estimates of real gross domestic product.

The decline in company earnings has hit the labour market via the weakest wage growth since at least 1998 (when the data began). Perhaps the most surprising thing is that this decline in company earnings hasn't translated into a significant rise in unemployment.

Companies have been reluctant to lay off staff – perhaps reflecting concerns over retraining or finding new staff when conditions improve – and have been content to absorb those losses rather than pass them on to employees.

Softer wage growth has hit the demand for goods and services and that is why inflation remains at such a low level. Economic growth, by comparison, remains slightly above trend due to external demand for Australian commodities. We continue to export growing quantities of iron ore and coal but the income we earn from those sales remains disappointing.

Why is employment growth so strong?

There is also a disconnect between inflation and employment growth. We have established that economic growth is being driven by commodity exports – a capital-intensive sector that doesn't hire a lot of staff – so why isn't employment growth a lot lower?

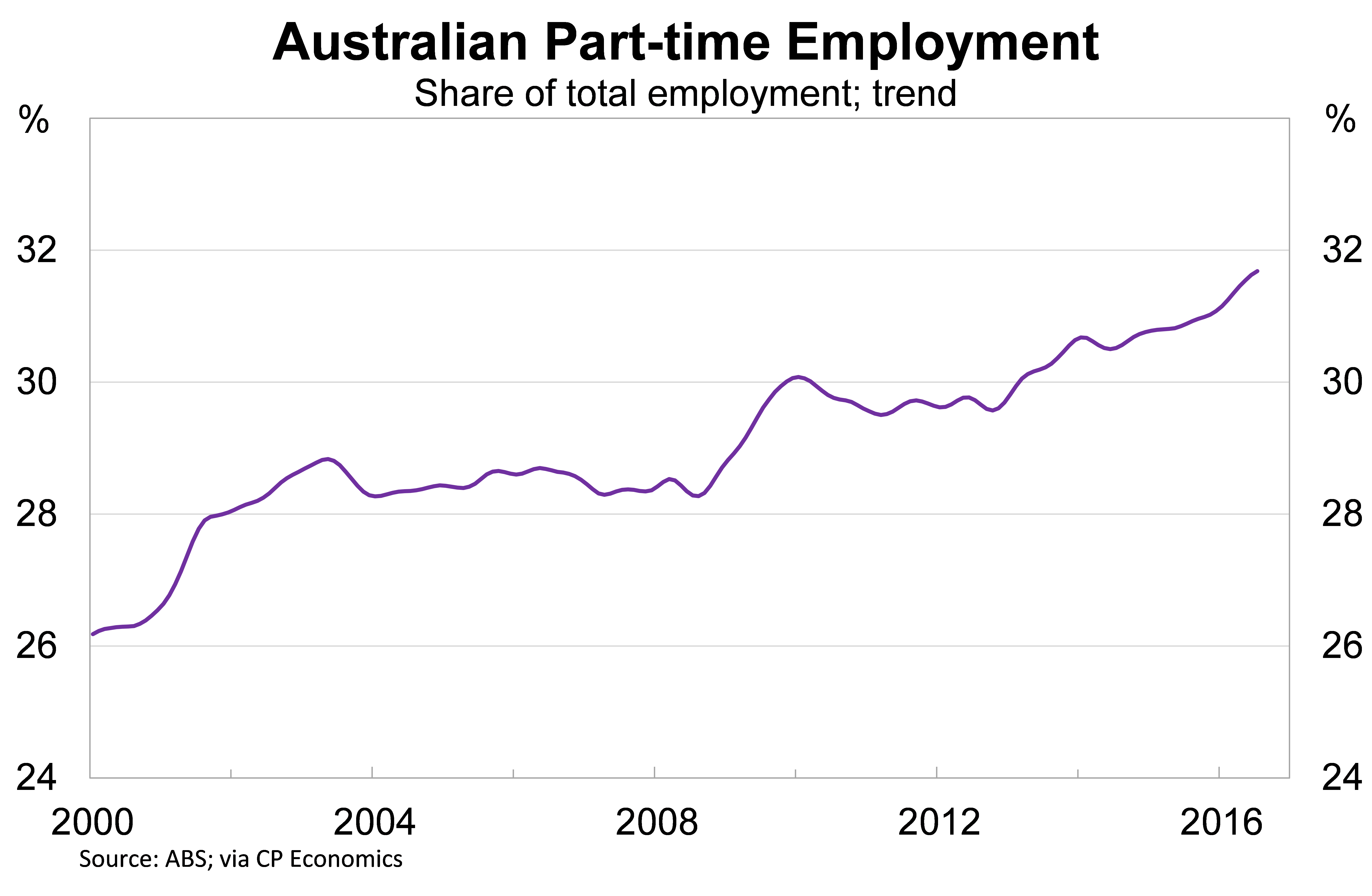

One reason, as I mentioned above, is that there is a reluctance to lay off existing staff. Another reason relates to the ongoing casualisation of the Australian workforce. Month after month we are witnessing a shift toward part-time employment at the expense of high-quality full-time roles.

Over the past year, part-time roles have accounted for three-quarters of total employment growth. Since the September 2013 election, part-time employment has accounted for 60 per cent of employment growth. Overall, part-time employment accounts for around one-third of the entire labour force.

This is a long-term structural change. The graph below shows part-time employment as a share of total employment.

The labour force survey is keenly scrutinised by market participants. It is arguably the most important monthly indicator for the Australian economy. Understanding the data and what it means in a structural and cyclical sense is important for investors.

The growing shift towards part-time employment requires a rethink on what constitutes strong employment growth. Employment growth of 20,000 people today is not the same as 20,000 people a decade ago since the former includes more part-time and casual positions.

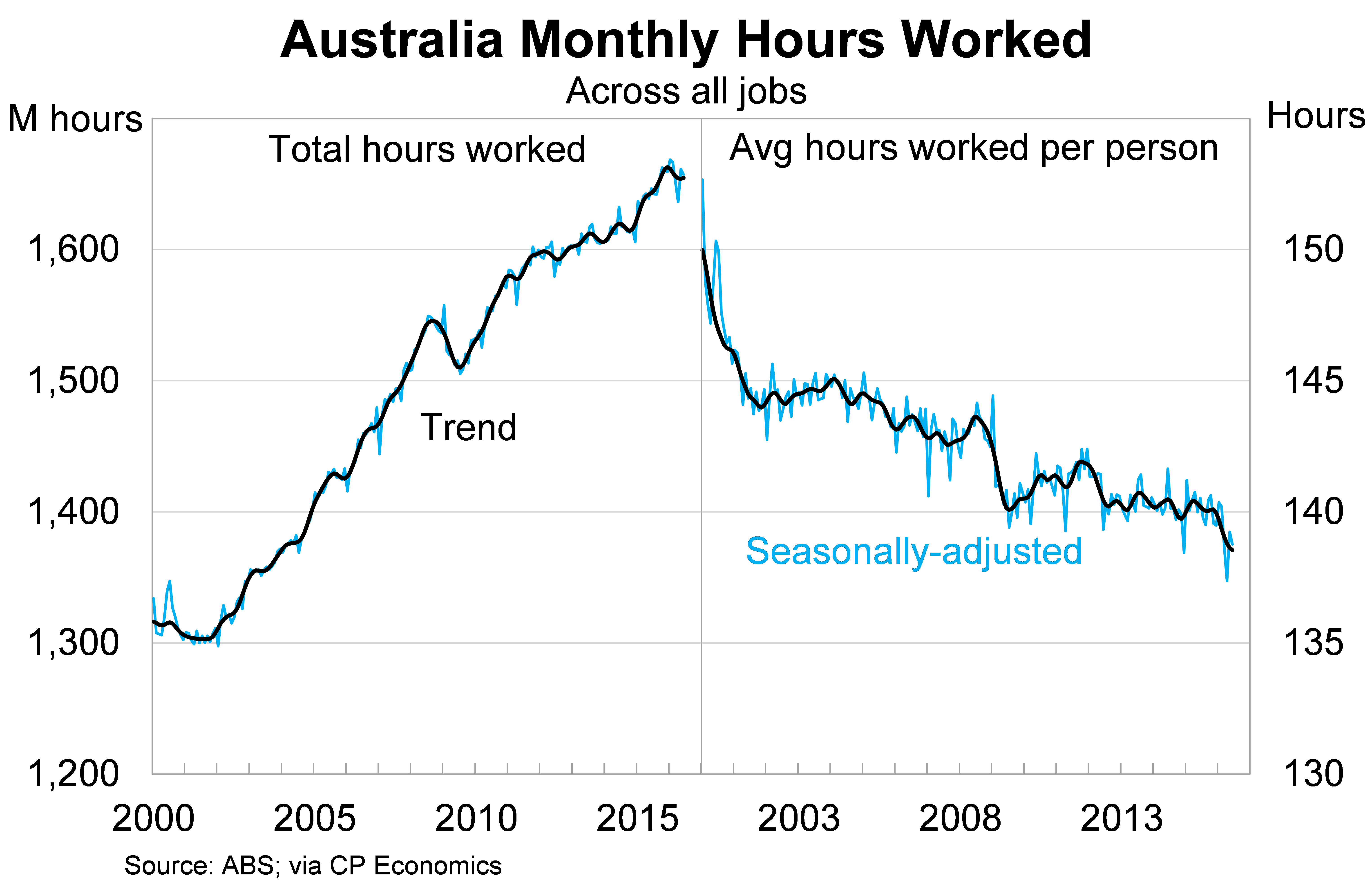

One solution for market participants is to focus more on the number of hours worked rather than employment growth. It's an elegant solution since, according to the Australian Bureau of Statistics, the number of hours worked is the most reliable indicator for the labour market.

Aggregate hours worked across the economy currently sits 0.4 per cent below its peak on a trend basis. Since that peak, in December last year, employment has increased by 74,500 people. We are creating a heap of jobs but companies across the country are utilising fewer employee hours than they were at the end of last year.

This reflects new employees taking on part-time or casual positions, as well as existing employees having their hours cut as companies try to contain cost pressures.

The casualisation of the Australian workforce can best be illustrated via the second panel in the graph below. It shows the average number of hours worked per person over the course of a month. Average hours worked per person has declined by 3.6 per cent over the past decade.

There are a number of reasons for this shift in Australian employment. The labour force has collectively become more flexible over the past two decades, as the influence of unions has declined. We have also seen an increase in the number of women in the workforce and traditionally women have valued greater flexibility in their working arrangements.

More recently it reflects the type of jobs created by the Australian economy. We are losing jobs in key sectors such as mining and manufacturing and creating jobs in sectors such as hospitality and retail. The former reflect full-time high-income roles, while the latter traditionally rely on casual and part-time staff.

The outlook for employment

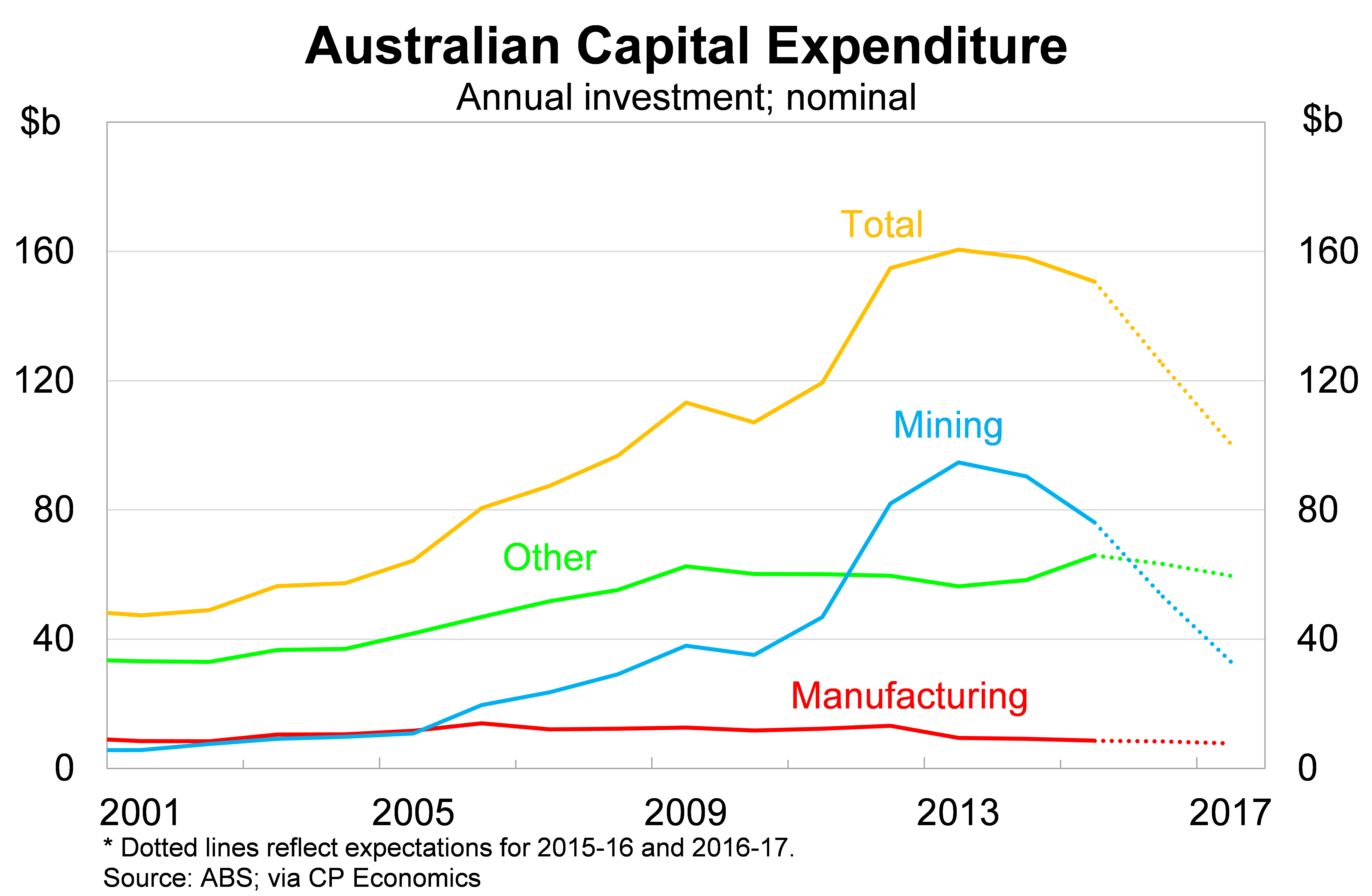

A major challenge for the labour market over the next few years is the weak outlook for business investment. Both the mining and non-mining sectors are expected to cut their capital expenditure over this period.

The graph below shows capital expenditure by the mining and non-mining sectors. The dotted lines represent estimates for the 2015-16 and 2016-17 financial years.

Investment is a key for productivity and employment growth. It's not a necessary condition, particularly when there is unused capacity, but strong investment will normally drive the creation of high-quality, high-income jobs.

It's been well documented that Australian companies are reluctant to invest (Business investment: the missing link, June 1). It's a problem globally. Rather than invest in new capacity and technologies, businesses have decided to pay down existing debt, pay out dividends or buy back their shares.

More importantly, for investors, investment represents the one sustainable path towards higher corporate valuations. Firms that aren't investing or preparing for the future are unlikely to experience the type of earnings growth that will justify higher valuations.

Right now equity markets across the globe are highly distorted by central bank policy. That won't change in the near term.

But identifying which companies are a sound long-term investment will require investors to look beyond monetary policy to determine which companies are investing in their future. Those who are will be well placed to provide sound returns once the influence of central bank buying diminishes. Those that don't will see their hefty valuations return to more normal levels.