Key risks for the global economy

Summary: Global growth is at trend and expected to rise, and the global expansion is robust, with only pockets of weakness. A fall in commodity prices is delivering stimulus, while central bank balance sheets are still to expand. But foreign policy errors have heightened tensions, the currency wars are raging, and there is a negative fall-out from excess volatility. |

Key take-out: The base case is that the global economy will remain very favourable, but a number of risks remain. |

Key beneficiaries: General investors. Category: Economy. |

Markets are in a state of flux at the moment. There is uncertainty as to what the slump in commodities heralds for the world. Rising geopolitical tension, the seemingly random acts of policy makers (such as the Swiss National Bank dropping its cap on the Swiss franc/euro rate, leading to a sharp spike in the Swiss franc), and global terrorism naturally add to the anxiety. So investors start the year, as we have every other year since the GFC, confronted by fear.

It's difficult not to get caught up in it all, I can appreciate that. Especially when our own market is taking a beating – and has done nothing over the last year! I'll talk more about the outlook for the market next week. Before I do, it's important to get a sense of where the global economy is headed and what the key risks are.

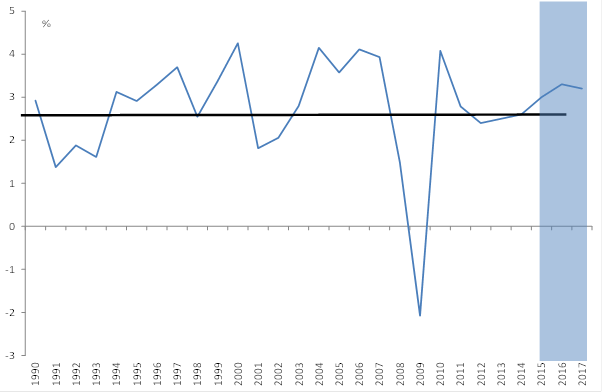

Macro-wise, things are looking good. A lot of noise was made about the World Bank downgrading their expectations for global growth last week. So much so that no mention appears to have been made that global growth – already at trend in 2014 – is expected to rise to an above trend pace in 2015 and for the next two years after that. That's not so shabby at all. It's unfortunate that trend-ish growth is now regarded as weak. That isn't the case. Trend growth is, well, what we should expect - it's “normal”, if I can use that word. Take a look at chart 1.

Chart 1: World growth forecast to rise above trend

So looking at the globe in its entirety, things are still very benign from a macro perspective. The US economy is doing better than anyone expected, as is the UK economy. Elsewhere in the world, emerging markets are growing at a solid clip. Growth in China is strong and expected to remain so, as is growth in India, Indonesia, Thailand and most of the major developing European and central Asian economies.

Indeed, the best way to describe the global expansion is robust, with only pockets of weakness, namely Japan and Europe/Russia. Naturally enough it'll be those pockets of weakness that will get all the attention. But really the only disappointments are Europe and Japan and as I noted at last year's investor conference, there is nothing unusual about weak growth in Japan and Europe.

The key risks the way I see them are evenly balanced at this point. That is, growth could be much stronger or weaker than this fairly benign base case scenario. I realise that sounds like a typically useless economist thing to say, but bear with me.

Upside risks

Left to its own devices, the global economy would be in a strong position, with little to derail it. So the base case scenario is still extremely positive for the real economy. There are few of the structural imbalances that began to hurt growth in 2007 and that led to the GFC. Interest rates are low, debt servicing is low, corporate balance sheets are pristine, there are no visible excesses in the consumer space. And as to the usual drivers of downturns or recession – a glut of housing or business investment – there is no sign.

In addition, 2015 faces an unprecedented degree of stimulus from two sources. Firstly, the collapse in crude oil and other commodity prices is delivering a huge stimulus to the advanced and developing economies. This hasn't even really begun to transmit through the world. Then, central banks in Europe and Japan are taking over, or are preparing to take over, from the US Federal Reserve as the primary source of global liquidity. That is, central bank balance sheets are still to expand in 2015, even if the Fed tightens, and there are very large question marks about that.

Downside risks

It's not all peaches and cream though. Policy makers are what concern me – those bureaucrats and politicians who are, without doubt, the single biggest threat to our prosperity. Foreign policy errors, largely American, have created heightened tensions with Russia, the crisis with ISIS, and so on. Geopolitical risks are high (see Geopolitics: What investors need to know in 2015, December 22, 2014).

In the economic policy space, the currency wars are raging and we have no idea when this process of monetary debasement – central bank money printing – will end. There is no doubt monetary policy is very stimulatory and that will continue to buttress growth. But this path isn't without very serious risks. As things stand now, there is a clear and present danger of a currency crisis, the key candidates being the US dollar or the Yen. Should other countries become more reluctant to accept those currencies or lose faith in them as a store of value, the consequences could be very serious. There is reason enough already for them not to.

Yet exiting this super stimulatory environment carries its own risks as well. If the Fed tightens (and that's a big if), should they miscalculate, then there is a sizeable risk of a disruptive bond collapse and a surge in yields.

Finally, there is the negative fall-out from excess volatility. Bizarrely, policy makers warned everyone that they were being too complacent last year. As if on cue, commodity prices collapsed and volatility surged, especially in the exchange rate and commodity markets etc. For 2015, what's to say that that crude won't surge, or iron ore for that matter? The US dollar for its part could just as easily collapse as rise again and all it would take is the US holding off on a rate hike. The move by the Swiss National Bank serves as a reminder as to just how dangerous policy makers can be to investors. It was a seemingly random act that burned many traders. The lack of fundamental drivers determining any of these prices means that they are not forecastable events.

These are just risks though – not the base case. The base case is that the economic backdrop will remain very favourable. How much support that will actually provide to investors is another matter though and something I'll discuss next week.