How did your SMSF perform in FY16?

Summary: Cash and fixed interest didn't do much to help SMSF returns in FY16 while property delivered – both at home and overseas. |

Key take-out: To beat the average market return for FY16, your portfolio had to perform better than 5.05%. |

Key beneficiaries: General investors. Category: Superannuation accountholders and SMSF trustees. |

ADVISOR Q&AInvestSMART begins our new 'Advisor Q&A' sessions on August 11 and we'd love you to let us know what investment and super questions you'd like answered by our panel of experts. We know that the Turnbull Government's proposed super changes are a hot topic, so are keen to discuss the unknowns with some real life examples in a webcast event on Thursday, August 11 at 12:30pm. You can register your questions and interest in attending the webcast: simply click here. |

A positive return in your self-managed super fund was probably just a dream for most of the last financial year.

Australian shares got crunched in July, then pounded in January and February this year. All these losses related to overseas events. SMSF accountholders were just taken along for the ride.

But last-quarter recoveries are funny things. They can turn negatives into positive returns in quick time. (In FY15, it was the opposite. A June quarter meltdown took away much of the year's gains.)

While shares often provide the glory, Eureka Report readers have increasingly discovered in recent years that diversification across other asset classes – cash, fixed interest, property and international shares – can provide valuable assistance when it comes to returns in volatile times.

And as you'll see below, not having fixed interest/bonds in your portfolio in 2016 made the job of getting a reasonable return that much harder.

So, how did you go in your job as “investment director” of your SMSF in FY16? What return did you manage to eke out for your retirement funds?

The number you needed to beat, assuming you wanted to beat an 'average' investment return for the year, was 5.05 per cent.

This is the figure that you could have achieved had you left your major investment decisions to an index fund manager and accepted basic asset allocation. (See our asset allocation across different risk profiles in Table 3, below.)

This is the seventh year I have written this column. The sole purpose is to give you a yardstick against which to measure your performance as an investment manager of your SMSF. (To see previous years' commentary and returns, see my previous columns here: 2015, 2014, 2013, 2012, 2011 and 2010.)

But first to the year just finished. How did asset classes perform in FY2016?

The returns of the individual Vanguard sector funds (after fees) were:

- Cash Reserve Fund: 2.13%

- Australian Fixed Interest: 6.78%

- International Fixed Interest (hedged): 10.46%

- Australian Property Securities: 24.38%

- International Property Securities (hedged): 18.17% (unhedged at 20.54%)

- Australian Shares: 0.65%

- International Shares (hedged): -1.27% (unhedged at 0.58%)

In the below performance figures, I have consistently used the “currency hedged” versions of the international share and property portfolios.

Last year, I included the unhedged versions of the international shares and property funds, because of the huge 20 per cent impact the falling dollar had as a one-off. The impact this year is far smaller, around 2 per cent.

It's interesting to note that property was, again, the standout performer for the year, both domestically and internationally, with performance returns straddling 20 per cent.

And … did you have bonds in your portfolio?

Cash has long been dead. No chance of it being revitalised as an asset class any time soon. But the relatively low-risk fixed interest asset class provided stellar returns again in the FY16 year.

International fixed interest returns topped 10 per cent and domestic bonds were approaching 7 per cent.

For the first time in many years, the Australian sharemarket outperformed international counterparts. But not by much. Australia barely eked out a positive performance ( 0.65 per cent), while international was marginally negative (-1.27 per cent).

Interestingly, we've got a bell curve this year, from a performance perspective on the risk profile axis. Those with too much cash performed poorly, because of the low returns on deposits, while those with too much exposure to shares (domestic and international) also were on the low side.

The best returns were from those who held relatively low amounts of cash and shares and had those two asset classes which I know Eureka Report readers tend to ignore – fixed interest and property REITs.

This led to the best returns this year, being from those with 'conservative' to 'moderate' risk profile tendencies. (My risk profile names have changed from previous years. However, there are still six profiles and the asset allocations have not changed.)

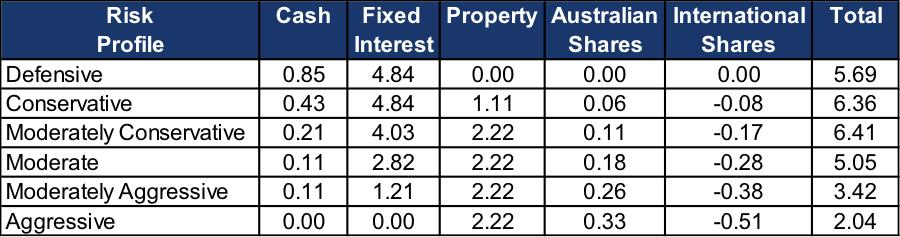

See Table 1 for returns for each of the risk profiles. (For the asset allocation of each risk profile, see Table 3.)

Table 1: One-year returns for FY16

Note: The performance figures under the asset classes is the amount, in percentage points, that the asset class contributed to the 'total' column. See Table 3 for asset allocation.

The one-year returns might seem a little subdued – but they are at least positive, following the last quarter run-up from shares and property.

SMSF trustees should, arguably, not hold themselves to account on performance matters for periods of one year. Fund managers are paid to panic and need to justify themselves via short-term performance targets and hurdles.

But not SMSF trustees. They only have their own long-term interests to consider.

So, perhaps three-year performance figures are more appropriate.

First, let's look at the performance of individual asset classes over that period.

The returns of the individual sector funds for Vanguard (after fees) for three years were:

- Cash Reserve Fund: 2.38%

- Australian Fixed Interest: 6.03%

- International Fixed Interest (hedged): 7.76%

- Australian Property Securities: 18.33%

- International Property Securities (hedged): 14.06%

- Australian Shares: 7.05%

- International Shares (hedged): 10.95%

We've got property (domestic and international) delivering serious double digits and international shares approaching 11 per cent.

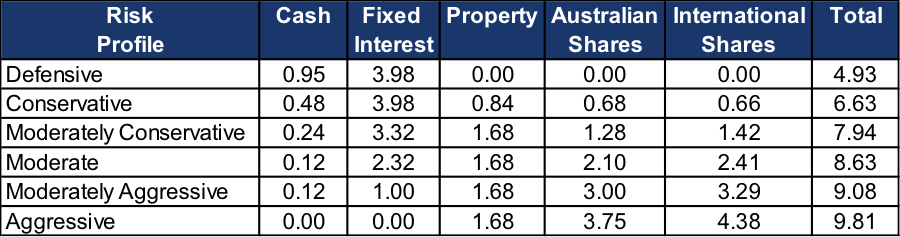

With FY16 being flat, but FY15 and FY14 delivering reasonably strong performance, what does the rolling three-year average look like? See Table 2.

Table 2: Three-year returns (FY14, FY15 and FY16)

Regarding your own risk profile…

If you haven't spent some time understanding risk profiles before, everyone will have a different perception of risk and a different idea of what assets should make up those percentages.

Compare your own SMSF's performance to whichever you believe most resembles your personal tolerance to risk (or do a risk profile. There's one available if you search my website at www.brucebrammallfinancial.com.au at the 'About us' page).

Table 3: Asset allocation across risk profiles

Asset Class | Defensive | Conservative | Moderately Conservative | Moderate | Moderately Aggressive | Aggressive |

Cash | 40% | 20% | 10% | 5% | 5% | 0% |

Fixed Interest | 60% | 60% | 50% | 35% | 15% | 0% |

Property | 0% | 5% | 10% | 10% | 10% | 10% |

Australian Shares | 0% | 9% | 17% | 28% | 40% | 50% |

International Shares | 0% | 6% | 13% | 22% | 30% | 40% |

Total | 100% | 100% | 100% | 100% | 100% | 100% |

The point of this annual column is to show SMSF trustees what sort of returns they could have achieved if they left everything to index fund managers, who charge tiny fees to try to get a return within a small margin for error from the major indices.

I realise that's not why most trustees take on the role, or start their own SMSF, but this column is also designed to be a reminder of how you can take on the investment risks about which you believe you might have some expertise (such as, perhaps, Australian shares, cash and maybe even fixed interest), while outsourcing the investment management for other asset classes, such as international shares and property, or even domestic REITs to low-cost index fund managers.

Mainly, it is designed to give you a benchmark for you to use to compare your SMSF's performance.

The information contained in this column should be treated as general advice only. It has not taken anyone's specific circumstances into account. If you are considering a strategy such as those mentioned here, you are strongly advised to consult your adviser/s, as some of the strategies used in these columns are extremely complex and require high-level technical compliance.

Bruce Brammall is managing director of Bruce Brammall Financial. E: bruce@brucebrammallfinancial.com.au . Bruce's new book, Mortgages Made Easy, is available now.