Were your returns super or normal?

Summary: The average investor posted before-tax returns of 7.86 per cent in FY15. No asset classes were negative, but unhedged currency assets won play of the day. Returns over the three years to June 2015 were stronger, with even conservative investors nudging 10 per cent. |

Key take-out: SMSF trustees can take on the investment risks in areas where they have some expertise and outsource the rest. The average return is a benchmark for you to compare your SMSF's performance. |

Key beneficiaries: SMSF trustees and superannuation accountholders. Category: Superannuation. |

Sometimes a dreadful quarter can completely wipe a smile from your face. Other times, it just downgrades laughter into a grin.

And that's what the dreadful final quarter for investment markets did to returns for FY15. And it was a dreadful quarter. The Australian market went backwards (minus 6.5 per cent), property markets tanked and bonds were also in negative territory by nearly 2 per cent for the quarter.

Had Europe not worked itself into a state over Greece during the quarter, investors, including SMSF trustees, would have been salivating at a third consecutive year of growth in the teens. Too good to be true. (And possibly one of those times to start getting concerned or to consider a reweighting of assets.)

It's okay. Growth was healthy. In fact, at the end of the year, performance was about as “normal” as you're ever likely to see. Hopefully, that leaves a little in the pot for the coming year … assuming the eurozone can sort out its problem child.

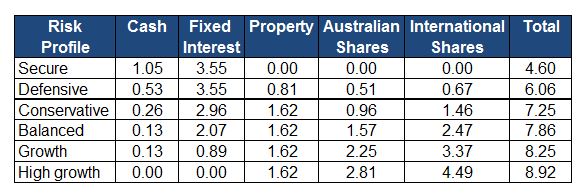

So what's normal? Of course, the answer depends on how much risk you are, as an investor, willing to take. But for the “average” investor, the answer for FY15 was 7.86 per cent.

A few quick notes to go with that figure and almost all figures in today's column. The figures are before tax on earnings. And they are based on the use of Vanguard wholesale funds, as laid out in asset allocation percentages below.

Third, this is assuming investments are diversified. A lack of diversification can lead to out-performance and under-performance. The less diversification, the bigger the potential spread from the average, obviously.

More conservative investors – those with more in cash and fixed interest and less invested in the more volatile assets of shares – should have returned between around 4.5 per cent and the low 7 per cent mark.

Invested in all cash for the year? Well, even 4.5 per cent would have been a struggle, unless you had locked in some term deposits. Our model figures assume an amount is allocated to fixed interest/bond investments.

Higher risk-taking investors were the ones whose performance was most trimmed by the poor final quarter. Still, they should have been expecting results in the 8-9 per cent range.

If you're really in need of a smile, then there are some great figures I can show you. (As I write this, I'm “stranded in Bali”, having been delayed getting here by the volcano ash cloud and in the lap of the gods as to whether our flight will return home as scheduled later this week. So, happy to be here, but concerned I could be stuck here for weeks.)

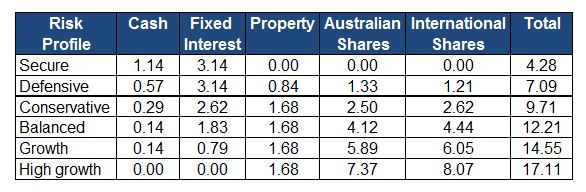

Take a look at the three-year returns below in Table 2. Everyone above even a mid-range risk profile is double digits, with high-risk takers performance topping a compound 17 per cent.

But first to the year just finished. How did asset classes perform in FY2015?

The returns of the individual Vanguard sector funds (after fees) were:

- Cash Reserve Fund: 2.63 per cent

- Australian Fixed Interest: 5.69 per cent

- International Fixed Interest (hedged): 6.32 per cent

- Australian Property Securities: 20.36 per cent

- International Property Securities (hedged): 8.48 per cent (unhedged at 23.81 per cent)

- Australian Shares: 5.62 per cent

- International Shares (hedged): 11.22 per cent (unhedged at 25.51 per cent)

It was a year when no asset classes were negative (we haven't separated out Greek bonds, but they would be included in the international fixed interest). Australia's property market clipped everything, by a long way, even with a poor final quarter.

We have always used the currency hedged version of the Vanguard international property and share funds for this annual exercise. And we will continue to. But I have included the unhedged performances above, to give you an idea of how much the fall in the Australian dollar from the US90c mark to the US70c region has added to performance of those asset classes over the year.

It is the first time in six years that having unhedged currency assets has won play of the day. In the previous five years (see Did you beat the super benchmark?, July 21, 2014) having the Aussie dollar hedged in these assets provided superior returns.

When it comes to domestic versus international measures, last year was all international – it won all asset classes. This year, however, foreign assets won in fixed interest and shares, but lost out in property (REITs).

See Table 1 for asset allocations for the various risk profiles, from “secure” through to “high growth”.

Table 1: One year returns (all are percentage points of entire return)

Note: The performance figures under the asset classes is the amount, in percentage points, that the asset class contributed to the “total” column.

To see the equivalent comparative returns for this same series in previous years, see my columns from 2014 (Did you beat the super benchmark?), 2013 (How super is your return?), 2012 (Are you good enough to run your SMSF?), 2011 (How super were your returns?) and 2010 (How does your SMSF measure up?).

And that's about as “normal” as returns are going to get. Most financial planning licensees will work on around the mid-5s for an average, long-term, return for “secure”, being all cash and fixed interest and about 9 per cent total returns (shares and dividends, plus capital movement). Returns don't come much more classic than they have (according to the asset sector returns I've used here) for FY15.

As a reminder, SMSFs who are not using international assets in their portfolio have continued to miss out – but who knows what will happen in the coming year. And Australian SMSFs tend to be heavily weighted to just two asset classes in Australian shares and Australian cash. That will, again, have come with a performance cost.

But the story for the three-year performance is considerably different, as pointed out earlier.

The three years ending on June 30, 2015 took in two spectacular years of strong performance across shares and property.

The returns of the individual sector funds for Vanguard (after fees) for three years were:

- Cash Reserve Fund: 2.85 per cent

- Australian Fixed Interest: 4.87 per cent

- International Fixed Interest (hedged): 5.93 per cent

- Australian Property Securities: 18.42 per cent

- International Property Securities (hedged): 13.65 per cent

- Australian Shares: 14.73 per cent

- International Shares (hedged): 20.17 per cent

Taking these into account, the returns from July 1, 2012 to June 30, 2015 have been superb and have improved from the previous year, which still had FY12 dragging down results. Take a look at the following.

Table 2: Three year returns (all are percentage points of entire return)

Cash rates obviously are at historic lows and have been for some time, which also partly explains why more use should be made of bonds and fixed interest in investment portfolios, even for heavily conservative investors.

But to have even conservative investors nudging 10 per cent is a result that should please most.

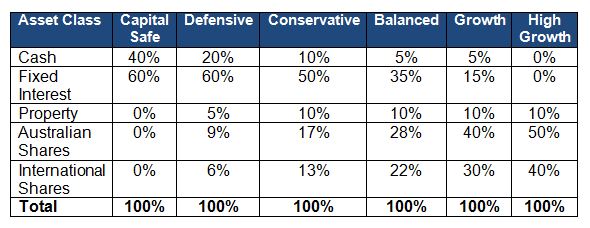

Now for your risk profile, if you haven't worked it out before. Everyone will have a different risk profile and a different idea of what a risk profile should look like when it comes to what assets make up what percentages.

Compare your own SMSF's performance to whichever you believe most resembles your personal tolerance to risk (or do a risk profile. There's one available if you search my website at www.brucebrammallfinancial.com.au at the “About us” page).

Table 3: Asset allocation across risk profiles

The point of this annual column is to show SMSF trustees what sort of returns they could have achieved if they left everything to index fund managers, who charge tiny fees to try to get a return within a small range of the major indices.

I realise that's not why most trustees take on the role, or start their own SMSF, but this column is also designed to be a reminder of how you can take on the investment risks about which you believe you might have some expertise (such as, perhaps, Australian shares, cash and maybe even fixed interest), while outsourcing the investment management for other asset classes, such as international shares and property, or even domestic REITs.

Mainly, it is designed to give you a benchmark for you to use to compare your SMSF's performance.

The information contained in this column should be treated as general advice only. It has not taken anyone's specific circumstances into account. If you are considering a strategy such as those mentioned here, you are strongly advised to consult your adviser/s, as some of the strategies used in these columns are extremely complex and require high-level technical compliance.

Bruce Brammall is managing director of Bruce Brammall Financial. E: bruce@brucebrammallfinancial.com.au. Bruce's new book, Mortgages Made Easy, is available now.