Balancing act: The trouble with too many bank stocks

Summary: With the banks delivering such incredible outperformance in recent years, we suspect many investors have substantial allocation to this sector. But given the banks offer a less attractive valuation case than three to four years ago, we ask whether it is sensible for investors to retain such overweight positions. |

Key take-out: Investors with unbalanced portfolios need to consider whether they are comfortable forgoing the benefits of diversification to generate a yield from the Australian banks. |

Key beneficiaries: General investors. Category: Shares. |

With the banks up 15 per cent so far in 2015, there has been a great deal of debate in recent times about how they stand as investments today.

On the one hand interest rates are low and the banks offer an attractive relative yield. On the other hand the case can be made for caution, with valuations at record levels and operating conditions that are potentially as favourable (or at least close to it) as they will to get.

The purpose of this note isn't to weigh into that debate. It is about making some observations around portfolio construction and where some risks may lie for many self managed superannuation funds and investment portfolios.

A recap on the banks as an investment

Financial stocks have been a terrific investment over the last three to four years. To put the performance into context, it is worth considering what investors were buying back in 2011.

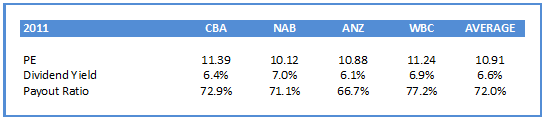

In 2011, investors were buying the banks on an average trailing price-earnings (PE) multiple of less than 11 times. This is broadly in line with where the banking sector has historically traded. Furthermore, banks were offering a fully franked yield of over 6.5 per cent, again broadly in line with long run average levels.

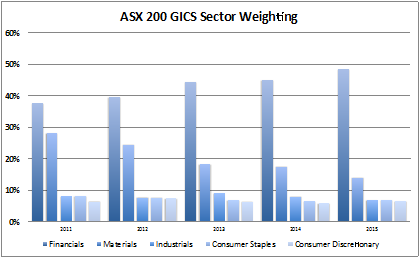

Back in 2011, if you were invested in an ASX 200 index fund, around 38 per cent of your Australian share portfolio would be in financial stocks. More specifically, roughly 25 per cent of your portfolio would be in the banks.

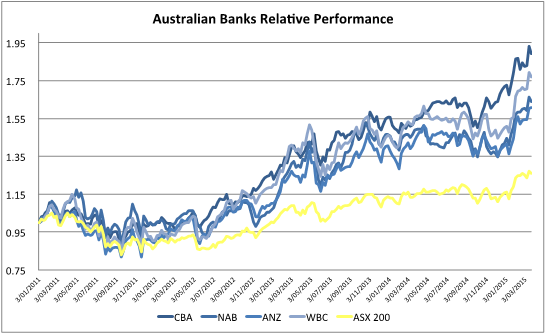

Since 2011, the financials sector (and more specifically the banks) has enjoyed terrific share price appreciation. Since the start of 2011, each of the big four banks have outperformed the ASX200 by a substantial margin: CBA by 63 per cent, WBC by 51 per cent, NAB by 38 per cent and ANZ by 35 per cent.

The net result of this outperformance is that investing in the banks is less appealing that it was four years ago on many metrics.

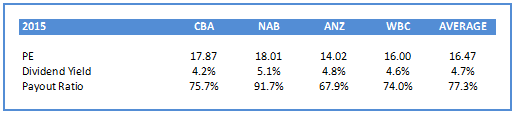

The market today requires an investor to pay 16.5 times trailing PE for a yield of 4.7 per cent – this is nearly two standard deviations above long run historical PEs. Such aberrations rarely last forever.

Considering the relative outperformance of the financials sector in recent years, the weighting of financials in an ASX200 exchange-traded fund (ETF) or index fund have increased from 38 per cent to 48 per cent. The banks, a subcomponent of financials, have increased from 25 per cent to 36 per cent.

This is a significant increase in portfolio allocation to an investment that is on a number of metrics now less attractive.

In reality, many self managed portfolios would have had a greater allocation to the banks than 25 per cent back in 2011, considering the long history of positive returns, the tax effective income stream they provide individual investors and a perceived understanding of the investment case.

For those self managed portfolios that started with a greater weighting to banks and financials, sector allocations today are most likely even higher that those outlined above. If that is you, congratulations, it has been an incredibly fortuitous trade.

However, the question is this: Is it sensible to retain a significant overweight position (relative to what history suggests is sensible) in an investment that offers the lowest yield that it has in decades and is trading at two standard deviations away from normal levels?

For those investors who have the majority of their portfolio allocated to Australian shares, considering this risk is even more important. Is it sensible to have roughly 40 per cent of your retirement savings effectively invested in one singular investment?

Basic portfolio construction: What is it all about?

At a very simplistic level the old adage of ‘don't put all your eggs in one basket' or diversification is about finding investments that aren't correlated. I.e. if one of your investments doesn't play out as you expected the rest of your portfolio should partially offset this. This is what traditional portfolio theory is all about.

Mathematically, if you can find 15 uncorrelated investments, for the same return profile you will reduce your portfolio risk (volatility) by around 50 per cent.

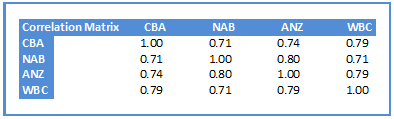

Not surprisingly, the Australian banks are highly correlated investments so holding a number or all of them don't provide meaningful diversification benefits.

As outlined above, the correlation of the Australian banks share prices over the past 15 years is high. Simplistically, a correlation of 0.74 between ANZ and CBA means that those stocks move together 74 per cent of the time. This has been the case as they go up – but equally as they go down.

A correlation this high means that if you have 40 per cent of your portfolio in the Australia banks, you effectively have 40 per cent of your portfolio in one investment.

This isn't to say that the banks are a bad investment but rather to say that if you are in this position you don't really have too many eggs in that figurative basket.

In a time of unprecedented financial market government intervention and extreme asset price levels by historical standards, this is a risk that investors should be thinking about when constructing portfolios.

Should you be forgoing the benefits of diversification to generate a yield for your portfolio?

For investors that need to generate an income stream from their investment portfolio, the natural follow on from considering reducing an allocation to the banks is to consider what else to invest in.

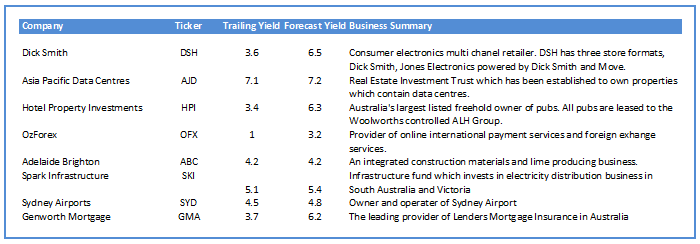

One stock which offers a yield of around 6.5 per cent that we have a positive view on is retailer Dick Smith. We recently wrote at length about this company, which we recommended as a "buy" on March 16. You can read about it here.

We outline below a number of stocks, which screen to us as worthy of further research when looking to add yield to a portfolio. A number of these stocks we do not formally cover so we can't provide a recommendation except to say they screen as interesting options.

A relatively new potential yield candidate is Caltex, which has been transitioning its business from oil refining to oil marketing and retailing. The company has benefited from the declining oil price and has a relatively conservative balance sheet.

However, on Friday night Chevron sold its 50 per cent stake in Caltex. This is interesting from a yield perspective as Caltex has $4.17 per share of franking credits on its balance sheet. With Chevron not in a position to benefit from franking credits, their exit from the register makes it much easier for the CTX board to return these franking credits to shareholders via increased dividends or a special dividend.