Vita leverages Telstra, AMA sparks growth

Vita Group delivers

Since we first recommended VTG at $0.70 in March 2014, chief executive Maxine Horne and her team have delivered on every promise. The end result is a share price of $2.97 that has increased by more than four times in two years. The share price increase has been a combination of large earnings growth and a P/E ratio that has doubled.

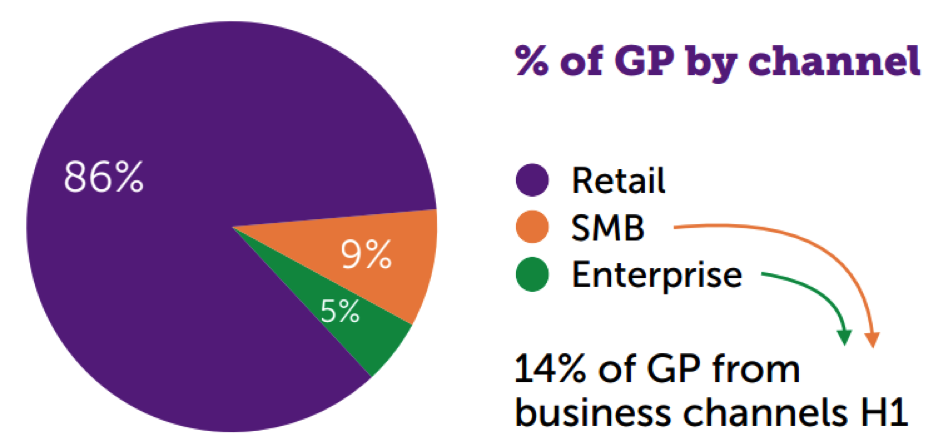

The success has been driven by the decision to close the non-core stores including Next Byte, Fone Zone and One Zero, instead of prioritising the opportunity to optimise the Telstra branded retail stores. In more recent times additional growth has been achieved from Vita's small-to-medium business (SMB) and enterprise channels. The company has continued to benefit from investment in people and technology.

Moving forward, Maxine Horne has reinforced her views that the company's best opportunities include:

- > Optimising the retail portfolio – physically and through performance initiatives

- > Driving scale and profitability in the SMB channel

- > Leveraging the foundations that are being developed in the enterprise channel

First half review

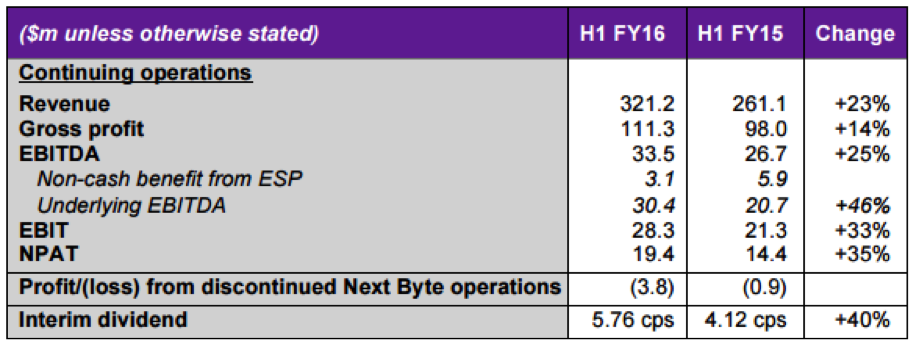

When looking at this interim result, there are two one-off factors impacting the accounts. Firstly it was announced in December that the Apple Next Byte business was to be closed down in February, and the second factor is the now discontinued ESP warranty and swap program. Reported earnings before interest, tax, depreciation and amortisation (EBITDA) was up 25 per cent to $33.5 million from continuing operations. Including Next Byte, EBITDA was $29.5m, well ahead of guidance in December of between $25.5m and $27.5m. Underlying EBITDA from continuing operations, which excludes the benefits of the now discontinued ESP warranty, was $30.4m – which is a 46 per cent increase on the prior comparable year.

Like-for-like EBITDA grew 12 per cent, with the balance of growth coming from the physical portfolio optimisation.

Margins were slightly reduced due to lower ESP revenue (due to expire in June 2016), the re-allocation of some support costs to cost of goods sold in business channels, and a higher proportion of hardware in the product mix. Despite this, productivity improved with expenses down as a proportion of revenues, reflecting the investments made in staff development and new and improved technologies.

Group revenues from continuing operations grew 23 per cent, reflecting strong performance from all strategic segments. The retail business – consisting mostly of the Telstra-branded stores – grew 22 per cent, benefiting from 21 per cent like-for-like sales growth and new additions to the portfolio from the prior year. The contribution from Fone Zone and One Zero was reduced, partly offsetting the Telstra store growth.

The SMB channel grew 51 per cent, with the addition of five Telstra Business Centres (TBC) and improved like-for-like performance ( 12 per cent). The enterprise channel grew 13 per cent, benefiting from account wins and growth in the managed services offering. Sprout accessories grew by 28 per cent in line with Vita's strong retail performance and expansion of third-party distribution.

The balance sheet remains in excellent shape with no debt and $10.6m cash. Capex of $13.5m was incurred during the period, mainly towards new Telstra Business Centres and strategic IT investments.

The interim dividend of 5.76 cents per share was up 40 per cent on the prior year. The payout ratio was maintained at a sustainable 65 per cent.

Telstra relationship

For a long time one of the reasons VTG traded at such a large PE discount to the market was due to the company's reliance on the ongoing health of the Telstra relationship. But as the company has continued to execute its strategic plan, it has become clear that Telstra benefit from the relationship to such an extent that it is hard to see them wanting to break the agreement.

There are 360 Telstra stores in Australia, with Vita owning 100, Telstra 80 and the other 180 being independently owned. The current agreement involves Vita being capped at 100 retail stores. Given Vita's track record of improving the performance of Telstra operated stores, if this number was to increase it would be a driver of shareholder value.

One of the key reasons Vita have been so successful is that the company has a greater ability than Telstra to foster a performance based culture. The investment in the development of people and leadership promotes highly motivated and incentivised staff.

Summary

Vita group remains well placed to continue growing from the continued optimisation of the retail stores, and greater emphasis on the growth of Telstra business centres and enterprise. But with success comes high expectations, and it will be difficult for the team to maintain recent growth rates. We maintain our HOLD recommendation with a $2.90 valuation.

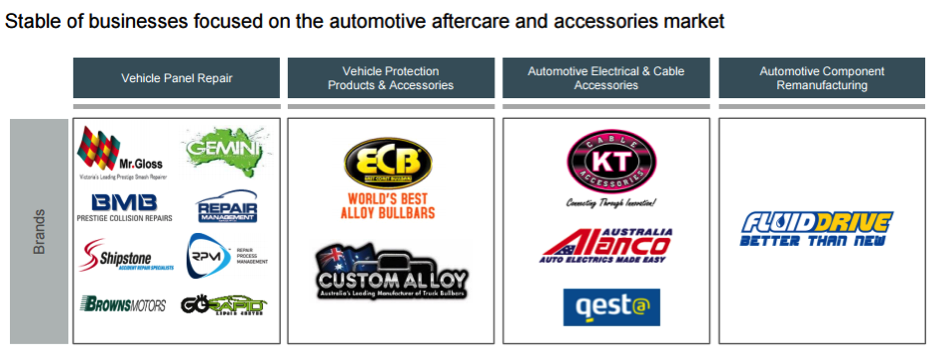

AMA: Panel driven growth

The highlight of the first half was the acquisition of Woods Group and Gemini Accident Repair Centres. Gemini was the largest independent accident repair group in Australia operating with sites across New South Wales, Queensland, Victoria, Australian Capital Territory and Western Australia. The purchase significantly broadened AMA's geographical exposure, with Gemini having eight centres in NSW, seven in Victoria, eight in WA, and 18 in Queensland. Previously AMA had 28 of its 29 panel shops in Victoria.

Gemini also brought $150 million of additional revenue to the group on top of AMA's prior $100m. As well as the obvious synergy and efficiency benefits, it also removes one of the main competitors who was trying to consolidate the smaller panel shops. Although the amount of panel body shops has reduced from 6000 to 3500 there are still significant opportunities for consolidation with the industry view that it will eventually reduce to well below 1000 shops.

As part of the Gemini acquisition, the AMA management team has been strengthened. Industry expert and former Gemini Executive Chairman, Andy Hopkins has become chief executive officer of the panel operations. Ashley Killick was appointed as chief financial officer and appointments of Brian Austin and Leith Nicholson as non-executive directors further strengthened the board.

Further smaller acquisitions

On January 4 AMA acquired Micra Accident Repair Centre, which is based in Launceston. Micra has a strong relationship with Suncorp, and was acquired for an initial $2m consideration. The “earn out” will be capped at a maximum of four times the normalised EBIT.

Further on the same date, AMA acquired BDS Panels; which is a panel operation based in Mornington. The business operates on a large two acre property, providing opportunity for expansion and was purchased for $900,000. This represents a very attractive earnings multiple of 2.5 times post synergy EBITDA.

On February 1, the group acquired Keswick Crash Repairs, located in Adelaide and specialising in the panel repair of Mercedes Benz. The purchase price for this business was $300,000.

Divisional performance

Although the consolidation of panel shops remains the key focus for AMA, there are still smaller growth opportunities through the other three divisions:

1. In Vehicle Protection Products & Accessories, moderate growth was achieved despite the impact from the reorganisation of the operations of East Coast Bullbars and Custom Alloy. Moving forward this change is expected to no longer be a drag and instead promote growth.

2. Automotive Electrical and Cable Accessories has performed well in a difficult market with new product initiatives delivering alternate revenue streams.

3. After the disposal of non-core Perth Brake Parts the Automotive Component Remanufacturing comprises the Fluid Drive operation. Although a very small division of the business, it is expected to continue growing.

Result details

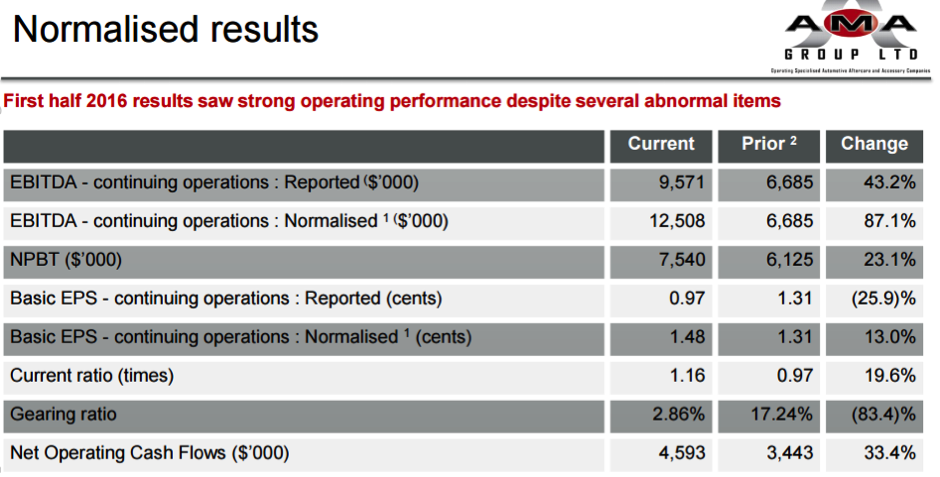

Net profit before tax for the six month period increased to $7.6m which is a 21.9 per cent increase. As expected the result was impacted by several large non-cash abnormal items, for example an employee equity plan expense and business acquisition costs.

These items also distort the effective tax rate, however this is also a one-off effect. The reported net profit after tax of $4.26m was slightly below the same time last year of $4.4m.

Revenue increased 155 per cent to $107.8m, reported EBITDA increased 43.2 per cent to $9.57m and normalised earnings per share increased 12.9 per cent to 1.48 cents. An interim dividend of 0.5 cents will be paid, representing an approximate payout ratio of 33 percent.

Gemini only contributed three months for the first half, and in combination with the other acquisitions AMA is set for a bigger second half. Although not fully realised chief executive Ray Malone stated that the synergy benefits have exceeded his expectations.

Outlook

Some of the difficult conditions AMA is up against include:

- Downward pressure on pricing, experienced as insurers try to protect their margins. Although in isolation this is a negative, it is one of the key drivers providing AMA with attractive acquisition opportunities.

- The low Australian dollar means further cost pressure on raw material purchases, but AMA will continue to crystallise synergy benefits from acquisitions.

Despite the step change in earnings from acquisitions, AMA has still provided fairly specific guidance for full year EBITDA of $28-29m (normalised).

Panel consolidation opportunity

As previously discussed, AMA is ideally placed to benefit from the fragmented nature of the panel industry in Australia. After eight acquisitions in the last 12 months, Ray Malone certainly has no shortage of his favourite work: That is, integrating finance, IT, HR and procurement to the benefit of the broader group. Malone has very detailed knowledge on what savings can be achieved from an acquisition, and his broad industry knowledge means he knows his competitors well. This reduces the risk of negative surprises after an acquisition.

AMA maintains very strong relationships with the major insurers (Suncorp, IAG) and prestige car manufacturers. This is critical, given the insurers are reducing the amount of panel operators that they accredit.

Summary

The guidance range of $28-29m EBITDA is slightly below our prior forecasts. However at 82 cents, the FY16 normalised PE ratio of 20, remains an attractive buying opportunity, given the 50 per cent growth that will flow through with a full year from acquisitions in FY17. The FY17 multiple is currently 14, and the stock remains at a discount to our slightly reduced $1.05 valuation.