Value is building for Brickworks

Brickworks (BKW), the $2 billion company best known for its building products division, is a diversified business, run primarily by the Millner family who are substantial shareholders. The three main divisions are building products, land development, and the cross-holding investment in Washington H. Soul Pattinson (SOL).

Robert Millner is chairman of both SOL and BKW while Lindsay Partridge is the managing director of BKW.

Given the complexity of the SOL cross-shareholding agreement and the nature of the products BKW produces it appears to have been overlooked in recent years while its building material peer group (Boral, CSR, James Hardie, Fletcher Building) has significantly re-rated.

The brick industry has been structurally declining for many years but the recently announced JV between Brickworks' two key competitors (Boral and CSR) should improve industry structure, and in turn, the outlook for BKW earnings. With the housing construction cycle remaining supportive, we believe that 2015 will be a year in which to take a closer look at the investment case in this business.

Industry changes should lead to favourable pricing

In recent years the brick industry has been presented with a number of structural challenges including:

- The growth in multi-residential construction (which is typically less brick intensive) relative to single dwelling construction

- A shift from double brick construction to single brick construction methods

- Increased penetration from other cladding materials.

Despite increases in housing construction activity, these factors have resulted in a near halving of brick production in Australia.

In addition, there has been an aggressive new entrant to the market in the Buckeridge Group (primarily in WA) as well as significant input cost inflation, primarily relating to an increased cost of gas.

Clearly, independent of the housing construction cycle, the brick industry has been through a challenging period in recent decades.

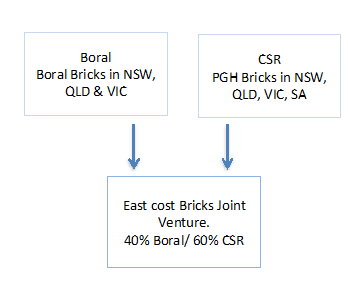

However, in December 2014, the ACCC approved a proposed joint venture to combine CSR and Boral's brick operations on the east coast of Australia. CSR and Boral are Brickworks' primary competitors on the east coast. The formation of the JV is expected to be complete in the first half of 2015 and is the first material improvement in industry structure that this product category has seen in many years.

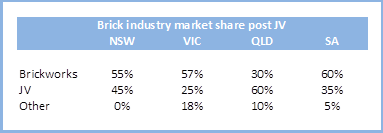

The transaction will result in significant industry consolidation as outlined below.

In recent years the industry has arguably behaved less than rationally in the eastern states as competitors chased volume over price due to Boral's lack of profitability in the eastern states and CSR's lack of market share in Victoria. Given the high fixed cost nature of manufacturing of bricks this has resulted in poor margin outcomes across the industry.

The consolidation of the industry will likely result in more rational competitor behaviour, and in turn, improved cost recovery/pricing outcomes. Our conversations with industry suggest that Lindsay Partridge has been the most aggressive in pushing brick pricing in recent years and this joint venture should see support from his major competitors. Ultimately we expect a 5-8% increase in brick prices in between now and FY16. We expect BKW to benefit as the lowest-cost producer nationally.

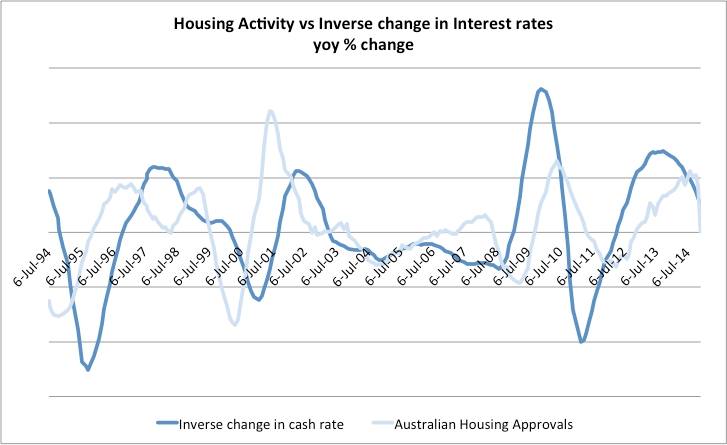

Housing construction dynamics remain favourable

If history is any guide, the primary driver of housing construction in Australia is affordability. And with marginal newly constructed houses being financed with a variable mortgage, the primary driver of affordability is interest rates. As outlined below, the correlation between the inverse in changes in interest rates to housing construction cycle is robust.

Source: ABS, RBA

Accordingly, with interest rates likely to remain subdued for some time and with a number of economists now forecasting further easing in 2015, conditions appear likely to remain supportive of housing construction for some time. This is particularly the case when you consider that lag between housing approvals and housing commencement/completions (i.e. when BKW gets paid) has increased in recent years.

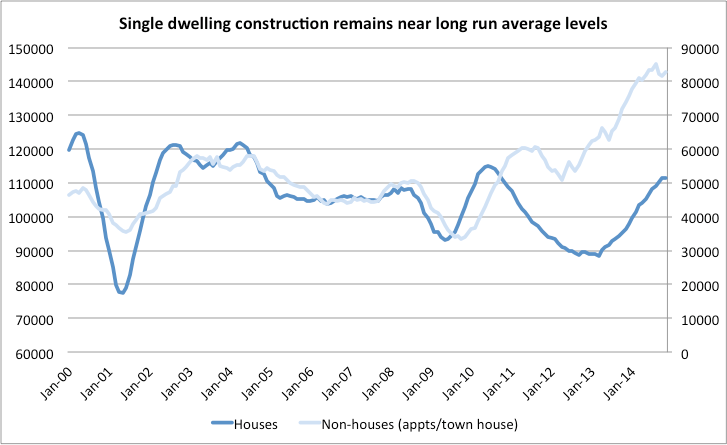

While building approvals, in aggregate, are typically considered when looking at the building materials sector, the composition is equally important. As outlined below the non-house component has been the primary driver of growth in approvals and is currently at near record levels. Unfortunately, BKW sells proportionately less products into this segment. However, from current levels, the houses component (single-family dwelling) is positioned to provide relatively favourable growth outcomes over the medium term when compared to the non-houses component. This should in turn favour Brickworks' product suite relative to competitors selling product into higher density housing.

Source: ABS

Ultimately, with improvements to industry structure and an accommodative cycle (at least in the medium term), we see Brickworks as well positioned to deliver growth in its building materials business. This compares favourably to many listed industrial businesses in Australia, which are devoid of growth outside of one-off cost cutting measures or currency benefits.

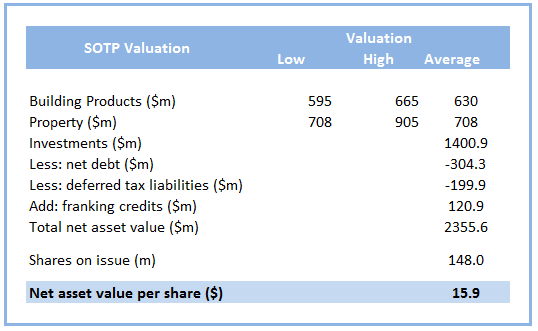

Valuation: Undemanding – compared both to domestic building material peers and to asset backing

Considering the diverse nature of BKW's business segments we have adopted a sum of the parts (SOTP) valuation methodology. We value the building products division in line with its building material peer group, the property division at NTA and the investment portfolio at market value. These are arguably a conservative set of assumptions.

As outlined below, this results in a SOTP valuation of $15.90. Considered another way, the current share price is ascribing an EBIT multiple of <2x FY16 earnings to BKW's building products division, other things held constant.

Given the complex nature of BKW's corporate structure we prefer to use a SOTP valuation methodology as opposed to P/E or cash flow analysis. However, to account for the SOL/BKW cross-shareholding we apply a 10% discount to our SOTP valuation and arrive at a price target of $14.30.

To see Brickworks' forecasts and financial summary, click here.