Time to hang up on Vocus?

Recommendation

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

When we upgraded M2 Communications in M2 finds life in Dodo (Buy – $6.02) it was a simple business and a simple idea. M2 leased broadband capacity from wholesalers and resold that capacity to retail customers under several brands including Dodo and Commander.

We weren't particularly enthused by the business model which leased infrastructure rather than owned it outright, but the business was growing and, most importantly, it was cheap.

As M2 continued collecting customers, a takeover of the business became increasingly likely and, eventually, it came. Competitors with native infrastructure could make more margin on every M2 customer by funneling them onto their own network and the upcoming NBN created an imperative to do just that.

Key Points

-

A three-way merger has changed the business

-

Opportunity to lower costs

-

Lots of growth baked into the share price

Vocus Communications paid 1.625 of its own shares for each share in M2 plus 9.5 cents in dividends, worth a combined $12.45 when the deal was completed in February and $14.61 today. Investors who followed our initial recommendation are sitting on a 143% paper gain. Is it time to cash in profits? To answer that question, we must understand the newly merged Vocus.

Focus on Vocus

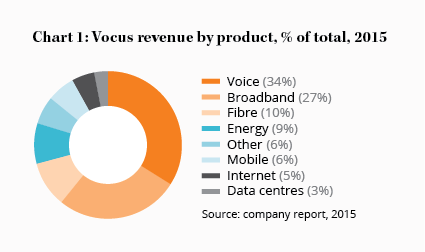

Vocus began modestly, leasing wholesale cable capacity, but has grown via acquisition to own its own spaghetti network of fibre.

The new Vocus – really a three-way merger with M2 and Amcom – is now Australia's fourth-largest telco, providing broadband, voice, fibre capacity and mobile services. Chart 1 shows how the enlarged business generates its revenue. Broadband and voice are the most important categories, contributing over 60% of revenue; in both categories, the rollout of the NBN looms as an imminent threat.

Last year, for the first time, non-NBN broadband connections declined as new NBN connections were activated. The switch to NBN is happening and it will have important implications for the industry in general and for Vocus specifically.

Almost 90% of M2 customers currently purchase voice and broadband bundles which generate higher revenue per user and high margins. As voice is replaced altogether by the NBN or mobile, the benefits of bundles are likely to unwind and margins will fall in Vocus's largest category.

The entire broadband market will be affected. Providers that have enjoyed a cost advantage from network ownership will see that advantage weaken as they are forced to lease capacity from the NBN. Infrastructure will still matter – access to backhaul and fibre connections can still lower costs – but scale will increasingly matter more to margins than assets.

For Vocus this isn't the worst outcome. As the business has the smallest network it generates the smallest efficiency gains from asset ownership. In the NBN world, it has the least to lose but we still expect margins to fall in the absence of cost savings.

The M2 and Amcom acquisitions will help there. Fibre infrastructure gained via Amcom could host some of the 500,000 retail customers gained from purchasing M2, saving Vocus about $40m per year. Fibre, which creates direct links to buildings and data centres, can still bestow an advantage even in a post NBN world.

This strategy – funneling acquired customers onto native assets – is how TPG has been so successful.

Yet Vocus's infrastructure isn't as extensive and, until the NBN is complete, it will still rely on pricey wholesale capacity from Telstra. Even post NBN, it will likely need to lease backhaul connections so margins will remain below its peers.

TPG has more customers, more capacity and lower costs. Its churn rates are half of Vocus' retail churn (which sits uncomfortably high at 30%) and it boasts higher average revenue per user: $50 per month compared to $44 for M2 prior to the takeover. Vocus is a better business now but it isn't immune from competition.

The best bit

Fibre contributes 10% of revenues and is arguably the best part of Vocus, generating the highest margins and the best returns.

Growth from this segment comes largely from connecting more buildings to the fibre network; Vocus has doubled connections over the year from 1,400 to over 3,600 thanks to acquisitions. Vocus connects buildings to data centres via its fibre to create high speed data networks that are closed to outsiders.

The economics of this business are attractive. Like pipelines, the major cost is sunk upfront but, once laid, marginal costs are low and new customers attract enormous incremental margins.

The business model relies on initial customers to cover the cost of product installation and earns profit by adding more customers at high margin. The more customers move to fibre, the more money Vocus makes. This is economies of scale at their finest.

Valuation

Too often, size is pursued purely for its own sake. Not here. There is merit to the enlarged Vocus.

Owning data centres encourages the sale of hyper-profitable fibre to link offices; half a million customers, decent fibre coverage and low costs should generate higher margins in combination than in isolation. Yet how much should we pay for that growth?

| 2015 pro forma |

2016F | 2017F | 2018F | |

|---|---|---|---|---|

| EPS (cents) | 26.2 | 32.5 | 40.6 | 50.7 |

| PER (x) | 34 | 27 | 22 | 18 |

You can see our estimates for earnings over the next three years in Table 1. Cost savings, combined with growth in the industry as well as from building more infrastructure, could raise earnings per share 25% per year for the next three years, taking it to about 50 cents per share in 2018. That's an aggressive assumption that would require flawless execution, continued industry growth and subdued competition.

Vocus is currently valued at $4.7bn, or $8.93 per share, a multiple of 18 times the best possible outcome we can imagine for 2018. The market, sometimes silly but often wise, has already seen what we have seen and is not only anticipating success from the three-way merger, it is pricing it as a certainty.

In an industry rife with competition and change, such a rosy assessment of the future is hugely risky.

There is nothing wrong with the Vocus business and management has done well to pull off a series of unlikely takeovers that make this a better business than it has ever been. Yet we do not collect decent businesses; we are interested in underpriced stocks. Vocus isn't one. We have done splendidly from our dabble in M2, more than doubling our money. It's time to take profits. SELL.

Recommendation