Pfizer gets its timing right

I've been a regular investor in Pfizer, the US-based pharmaceutical stock since the 1980s. Today I see it at a price and range of opportunities that rarely occur together. To understand why Pfizer is a 'buy' just now takes a little learning – you need to understand the story of 'biosimilars' in world medicine...they are a major breakthrough both for the pharmaceutical industry and for healthcare costs.

On March 6, 2015 the US Food and Drug Administration (FDA) approved the first biosimilar product in the United States under the new 351K biosimilar pathway mechanism, Sandoz's Zarxio (filgrastim). This decision has profound implications for the pharmaceutical industry.

So what's a biosimilar? It's a biological product that is approved based on clinical studies showing it is highly similar to an already-approved biological product, known as a reference product (in the Sandoz case it was Amgen's cancer drug Neupogen, a $US7 billion per annum product).

The biosimilar must also show it has no meaningful differences in terms of safety and effectiveness from the reference product. Only minor differences in clinically inactive components are allowable in biosimilar products. Biosimilar drugs have been available outside the US for a few years in limited quantities. In Europe they tend to cost 15-30 per cent less than branded products.

Biologics drugs, which are derived from a living organism: humans, animals, and various micro-organisms as opposed to “small molecule” chemical-based drugs, account for 30 per cent of total spending on drugs in the US and are growing rapidly.

Biosimilars will likely come in at significant (greater than 50 per cent) discount to the innovator list prices. Industry analysts anticipate key biologic revenues to erode globally from $US65bn to $US30bn over the 2017-2024 time frame so there will be winners and losers.

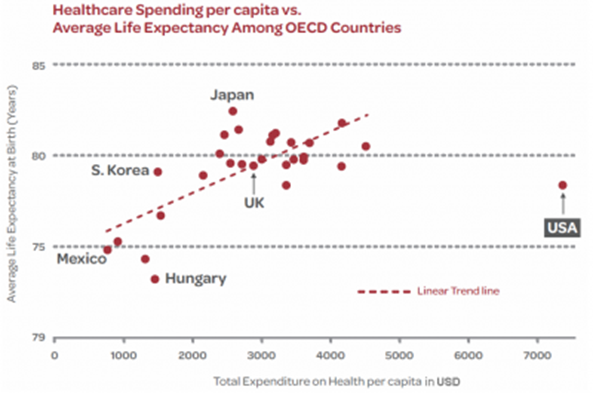

Healthcare spending in the US is so far beyond its developed world peers that it must be reined in (see below).

The lower price of biosimilars is one way to reduce total healthcare spend. Governments, regulatory agencies, and pharmacy benefit managers will be supportive of biosimilar adoption as will consumers.

A big winner will be Pfizer, one of the world's largest drug companies by revenues.

Pfizer focuses on drug discovery for human diseases. The company has key franchises in cardiovascular, infectious diseases, inflammatory conditions and vaccines. In 2014, Pfizer generated approximately $56bn in biopharmaceutical sales.

Pfizer is best known for two famous products- Viagra, ‘the little blue pill” (for erectile disfunction) and Lipitor (used to lower LDL cholesterol). I have been in and out of Pfizer's shares since the late 1980s.

The company is one of the clear beneficiaries of the biosimilar approval due to a recent acquisition. With impeccable timing, on February 5, 2015, Pfizer spent $US17bn to acquire US-based Hospira (HSP), a leader in generic and biosimilar medicines, instantly making the company one of the top three global players in biosimilars.

Hospira's product line has two high growth areas:

- biosimilars—drugs that have been engineered to have active properties that mimic those of a larger "brand name" drugs with previous license protection—is expected to be a market opportunity in the US alone of $US20bn by 2020. Hospira is on track to gain approval for the next two biosimilar compounds to be approved in 2015.

- Sterile injectables which will have an addressable market of in aggregate, of about $US70 Billion globally by 2020.

Expanding into the biosimilar market is strategically necessary for Pfizer, as many of their most profitable pharmaceutical products have lost or are scheduled to lose their intellectual property protection and are being replaced by generics.

Biosimilars are more of a medium to long-term story for Pfizer and the other biosimilar players about to enter the US biologics market. It will take time for biosimilar “sponsors” to clear both regulatory hurdles (the FDA) and negotiate (and perhaps litigate) with the innovators of the original indication.

However, ‘the genie is out of the bottle” and regulatory and intellectual property hurdles are no longer insurmountable since the FDA is now willing to accept EU and external bridging trials and there is now an acceptable regulatory pathway (351K) for biosimilars in the US.

It is the intellectual property hurdle that is the most time consuming and complicated. The Biologics and Price Competition and Innovation Act (BPCIA) of 2009 provides an abbreviated pathway for biologics to enter the market and negotiate with innovators but in many cases will give rise to further litigation. It is hoped that the FDA approval of Zarxio will clear up many of the ambiguities surrounding BPCIA.

That being said, I am also more positive toward Pfizer than I have been for some time because of a large and reinvigorated pipeline.

Pipeline summary

Pfizer is making big advances in its pipeline, having gained accelerated FDA approval for Ibrance (to treat metastatic breast cancer). Ibrance could be a $US5bn drug and has a significant lead over Novartis's LEE011 & Lilly's abemaciclib by at least two years.

Ibrance is priced at $US118,000 per year and will benefit from a very large patient population.

Pfizer also has a growing immune-oncology portfolio (an area that has huge potential in my opinion) with five IO drugs in the clinic by the third quarter of 2015 including a viral vector DNA vaccine for prostate cancer.

What's also promising is Pfizer's CCR2 inhibitor (‘309) which has shown a 48 per cent response rate in Stage III pancreatic cancer, a disease that is invariably a death sentence.

Over the next four years, Pfizer has 20 drugs that are in later stages of development. The company now has about 90 drugs in its pipeline, and more than 60 per cent are in Phase II or III trials. Key areas include cancer, neuroscience & pain, and inflammation & immunology, which account for more than two-thirds of these assets.

Other pipeline highlights include the filing of new indications for Xalkori (anti-cancer) and Xeljanz ( chronic plaque psoriasis), which could be key growth drivers over the near term.

Valuation and recommendation

Pfizer is modestly valued and trades at 15.3 times 2015 earnings per share (EPS) and pays a 3 per cent dividend.

Earnings are forecast to grow at a 14 per cent compound annual growth rate (CAGR) between 2014 and 2017 (see financial model below for assumptions).

This year the stock is up 10 per cent and over the last 12 months has given investors a slightly better than market return (14 per cent versus 13 per cent for the S&P500).

I would be a buyer of Pfizer at these levels. This is a high quality, innovative company that has the potential to grow at a much higher rate than seen over the past decade due to the biosimilar opportunity and its promising pipeline. That is not in the price in my opinion.

My target price is 16.5 times 2016 EPS of $US2.52 or $US41.50. Pfizer closed on Friday at $34.25.

Risks

As with any pharmaceutical or biotechnology company, failures of key products to either achieve sales estimates or gain FDA approval are the key risks:

- CDK4/6 inhibitor Ibrance may not meet sales targets

- Xeljance sales may be pressured by safety issues or competition.

- Delays in approval for blood thinner Eliquis and competition from Daiichi's drug edoxaban

- Poor trial data for potential blockbuster drug Prevanar 13 (prevention of pneumonia in the aged).