NetComm surges ahead

Global macro concerns have done nothing to stop the NetComm (NTC) share price surge. At $1.37 it is up 50 per cent since the full-year result late last month, and the stock has tripled since the half-year result in February.

The company has also been an excellent performer for the Growth First model portfolio, up 85 per cent since the portfolio started on July 1. This portfolio is up approximately 8 per cent vs the S&P/ASX200 benchmark which is down 10 per cent in the same period. The 18 per cent outperformance is a very strong result, but it is early days with just under three months of history.

The NTC strength leading into the full-year result was mainly due to the faster rollout of the domestic rural NBN. With former communications minister Malcolm Turnbull becoming Australia's Prime Minister, there is potentially more good news to come in future weeks for the domestic opportunity.

The other major share price driver has been the prospect of the company's first major overseas contract. The most likely one is AT&T (large global telco) in the US, where the contract would provide strong earnings upside. There would also most likely be an earnings multiple re-rating due to the improved prospects of global scalability in rural NBN, and other machine-to-machine (M2M) related work.

Our prior valuation of $0.95 only included current contracts, and was potentially also too conservative around the domestic NBN opportunity.

AT&T: What would it mean?

With a share price under $1, the potential AT&T contract was a free option, but at the current price there is now downside if it doesn't come through. Therefore current holders need to consider the risk/reward opportunity and try to determine the likelihood of winning the contract.

In July, AT&T completed the $48.5 billion purchase of DirecTV, with final regulatory approval. Part of the conditions of this acquisition was AT&T committing to a rural broadband. NTC management has guided towards the company being in the final stages of the tender process with other competitors also still in the running.

The contract is due to be announced by December and the rollout would begin 12 months after.

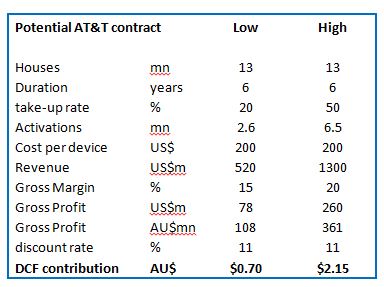

The assumption above of 13 million homes is taken from a report AT&T lodged with US government bodies as part of its acquisition of DirecTV. On top of the 13 million homes, there are also another 20 million homes in the US that could become available in future with other telco providers, but these have more risk around funding.

The table above lists our low and high case assumptions for the AT&T contract. It can be seen that it would add $0.70 to $2.15 (mid-point $1.43) to our prior $0.95 valuation. Conservatively we are going to assume there is a 30 per cent chance of winning the contract. 30 per cent of the mid-point value ($1.43) from AT&T adds 43 cents to our prior $0.95 valuation, combining to $1.38.

Our 30 per cent assumption is based on NTC being shortlisted from an initial 13 competitors down to the final three. NTC is the only company in the world to have supplied the devices for a rural NBN, which potentially provides an edge against competitors who are just competing on price.

So as long as you are comfortable with the assumption that NTC is a 30 per cent chance to win AT&T, then the share price can be justified by our risk-weighted valuation of $1.38. Then if this contract comes through the valuation range will increase to $1.65-$3.10.

But this approach is not considering the read-through for future wins. Rural broadband is considered an $80bn global opportunity, and AT&T is a huge global telco with over $130bn in revenue. Therefore a win with AT&T would just about guarantee other global opportunities.

At $1.37 the stock has a market cap of about $175 million and is trading on a price-earnings ratio of 15 times FY16, with strong growth locked in for FY17 and FY18 from the domestic rural NBN. As well as the earnings impact in the table above, the contract win would enable the company to trade on higher multiples due to a more diversified earnings base and greater prospects of global scalability.

Domestic rural NBN

Weekly activation rates continue to rise and are now above 1500 per week. We are at around a 20 per cent take-up rate and in FY15 29,656 homes were activated. NTC actually sold 45,000 devices in FY15 because NBN Co order devices ahead of demand.

Conclusion

At current prices a global contract (preferably AT&T) needs to be announced by the end of the year or there is the potential for 30 per cent downside from current levels. As shown above the upside is certainly there if the contract comes through. Our valuation range would increase to $1.65 – $3.10.

But until announced there is always the risk that that the company either misses out completely or faces competitive pressure on pricing and ends up with a lower than 20 per cent margin.

Other than rural NBN, there are multiple other M2M opportunities that the company is pursuing. Smart meters also have global potential, with NTC having the advantage of completing work in Australia.

Our risk-weighted valuation increases to $1.38 and we maintain our hold recommendation. Given the current weak market conditions and NTC's very strong recent few months it may be worth waiting for share price weakness and a material discount to our $1.38 risk-weighted valuation before buying.