Income results wrap: AHG, Tatts and Flexigroup

Flexigroup (FXL)

Flexigroup Limited announced a 7.25 cent fully franked interim dividend. Shares will trade on an ex-dividend basis on the March 9, 2016, and proceeds will be paid to eligible shareholders on the April 15, 2016. This dividend amount was very close to our expectations for 7 cents, but is lower than that paid in previous years.

The reason for the lower dividends in FY16 has been well flagged to the market and relates to the need to pay dividends to additional shareholders as a result of the rights issue associated with the acquisition of Fisher and Paykel Finance (FPF), which is expected to be completed in a few months' time. FXL management were clear to emphasise that the reduced dividend is seen as temporary, and a reversion to a higher level will be expected in coming periods as earnings from FPF begin to contribute to cash profits.

Despite this timing issue being a slight negative, the longer term opportunity and growth prospects for FXL remain in place, and the completion of the FPF acquisition will be a key catalyst for both earnings and dividend growth. There are still challenges at FXL with funding markets tightening, and volumes in some segments weakening. That said, the share price reaction to the result was quite pronounced, and in my view unwarranted.

Highlight and key challenges

FXL grew cash net profit after tax (Cash NPAT) by 4 per cent when compared to the first half last year, from $42.5 million to $44.3m. The growth was driven by a 5 per cent lift in sales volume with the highlights being the Interest Free Cards business, and the NZ leasing business (though this was driven by the acquisition of TRL). The Australian Leasing business (a combination of the divisions previously reported as Consumer, SME and Enterprise) was a clear laggard for the company, as the business restructures its team, and saw declines in both volumes and receivables. In particular, the Rent smart product runoff, and a slightly weaker than anticipated performance in the Enterprise business led to lower volumes, receivables and Cash NPAT contribution. In my view this division may take some further time to recover back to previous volumes and profit contribution, and is a key area of challenge for the business.

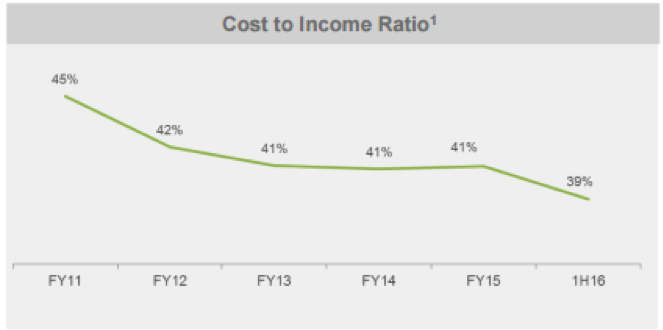

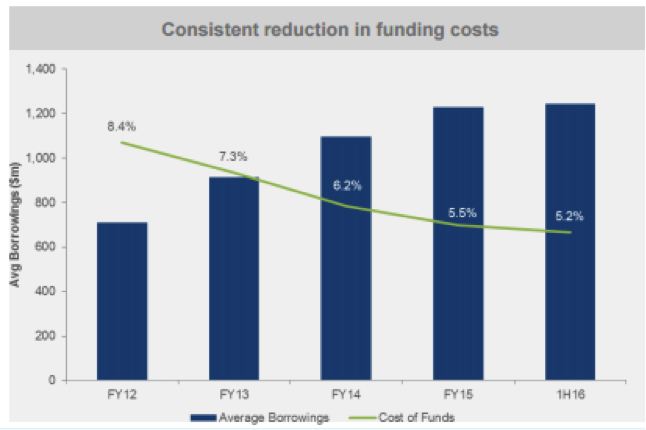

Aside from this, there is some macro risk emerging for FXL. The company's cost to income ratio was very well managed in the first half at 39 per cent, down from 41 per cent in FY15. However, this could be attributed not only to good cost control but to the absence of a chief executive salary – something which will not continue with the appointment of Symon Brewis-Weston. Despite this, the market appears to have funding cost concerns as securitisation markets have tightened in recent months. With FXL likely to need to securitise some Certegy receivables later in the year, there is an expectation that the cycle for lower funding costs is near a bottom. Here are two charts of FXL's cost to income ratio and funding costs over recent years:

Source: FXL 1H16 results presentation

In my view, these two metrics are likely to be near a bottom, leading to the conclusion that profitability may be more challenged in coming periods. However, the market response to these concerns has been overly emphasised. The group still continues to grow in terms of top line, and with the acquisition of FPF expected to produce a minor second half contribution and strong lift to earnings and dividends in FY17, these concerns appear overdone at current price levels.

Key take-away and outlook

This result was well flagged by management, and in my view was of little surprise. The Australian leasing business was perhaps slightly weak than anticipated, impacting the overall cash net profit. Additionally, volume was soft in Certegy (the no-interest ever lending business), which accounts for around 40 per cent of revenue.

That said, the company reconfirmed its guidance for full year cash NPAT between $92m and $94m excluding any contribution from the FPF acquisition. With a first-half result of $44.3 m in cash NPAT, achieving this guidance would suggest an expectation for a stronger second half. All in all, the result was solid, but uninspiring. The real catalyst will come in the FPF acquisition, and we remain comfortable with our buy recommendation. We have adjusted our expectations for organic growth in the existing FXL business downwards. With building cost pressure and a chance that macroeconomic influences will provide challenges, it is the prudent assumption. This leads to a lower valuation of $3.13, down from $3.22. Once the FPF acquisition is complete, we expect that FXL management will provide a further guidance update to the market, which is expected at the beginning of April. Investors should watch for interest rate and unemployment data for further potential influences to the outlook.

Tatts Group (TTS)

Tatts Group announced a 6.2 per cent growth in underlying net profit to $147.9 million for the first half of FY16. This was accompanied by the announcement of a 9.5c fully franked interim dividend, with shares to commence trading on an ex-dividend basis on March 26, 2016. This dividend represents a payout ratio of 94 per cent, and is consistent with the company's past delivery of a 90 per cent payout ratio. Cash flow remained strong and the business has a stable balance sheet. The key concern is the pending outcome of the long run litigation regarding the Victorian pokies license that is expected to be handed down this half. Nonetheless, the dividend is strong and growing and the business has put in a solid half. We remain comfortable with TTS, maintaining our buy call and lift our valuation from $3.97 to $4.13.

The standout of this result was the lotteries franchise. This has benefitted from a higher number of jackpots in the half, and pleasingly this trend has continued into the first six weeks of the second half. The newly launched “set for life” product is doing well after commencing in August, and is the company's first new game in 20 years. This product is targeting a younger demographic, and pleasingly has seen strong digital sales at 22 per cent through the digital channel. As a segment result, Lotteries was the standout with earnings before interest and tax (EBIT) lifting by 11.3 per cent, from $148m in the pcp to $164.7m this half.

The wagering side of TTS business has seemingly turned a corner; with strong growth in turnover suggesting that the increased marketing spend in Ubet is gaining traction. We note that margins in this division are decreasing as the mix shifts further towards fixed price wagering, which is lower margin. This is a trend that is expected to continue, though chief executive Robbie Cooke was keen to note that Tatts remains one of the highest margin operators in the industry. The wagering business's margins have stabilised at around 23.5 per cent, based on earnings before interest, tax depreciation and amortisation (EBITDA). This is a positive after margin volatility in previous halves was caused by increased spend on the Ubet launch. Despite some positive undercurrents, we continue to believe that there are risks in this area of the business with a highly competitive industry landscape.

The gaming division provided a robust performance, with Maxgaming providing a solid contribution and Telarius showing promising growth. The combined EBIT contribution for this segment was $33.8m, up from the $28.3 recorded in the pcp.

Litigation uncertainty

As discussed, TTS is involved in litigation surrounding the loss of the Victorian pokies license back in 2012. The matter has proceeded through the courts system and is with the High Court under appeal by the state. TTS has booked a current liability for the cash it received via judgment at a lower court and this is providing a near term interest cost benefit. Management has flagged that should it be successful, the proceeds will be returned to shareholders in the most efficient manner considering interests of all shareholders. For now, we will await the decision, but it is worth noting that this decision will potentially have a material impact on the TTS share price. Investors should consider the risks associated with this in the short term.

Key take away and outlook

The key thing to take away from this result is that the Lotteries business is strong. This part of TTS accounted for 62 per cent of EBIT and remains the key driver, so this is a clear positive. The strong start to the second half in terms of jackpots is a good sign, and the early successes of the Set for Life product are encouraging. Somewhat offsetting this is the margin decline expected in the wagering business as the mix shifts further towards fixed price wagering. Wagering is a material part of the business at a 26 per cent EBIT contribution, and this could drag slightly on future earnings growth.

Overall, the result was ahead of our expectations, albeit only slightly. TTS is a solid business with defensive attributes and a high dividend payout ratio that make it a clear fit for our Income First model portfolio.

Following the result we have revised our forecasts slightly higher, leading to a lift in our valuation from $3.97 to $4.13. In line with this, we maintain our buy recommendation.

Automotive Holdings Group (AHG)

Car dealership aggregator and logistics business AHG delivered a solid first half result, with net profit after tax (NPAT) climbing by 7.3 per cent to $49.4m, from $46.1m in the previous corresponding period (pcp). The result was predictable and delivered an impressive rate of growth for a business of this size. Margins were flat at 3.3 per cent in terms of earnings before interest and tax (EBIT), but top line growth translated into growth of 11.6 per cent to $94m in EBIT for the half.

With the result, AHG announced a 9.5c fully franked interim dividend. Share will trade on an ex-dividend basis on March 17, 2016. Given that the company recorded earnings per share of 16.1 cents in the period, this dividend payout remains well within the company's profitability levels and represents a payout ratio of approximately 59 per cent.

Divisional performance

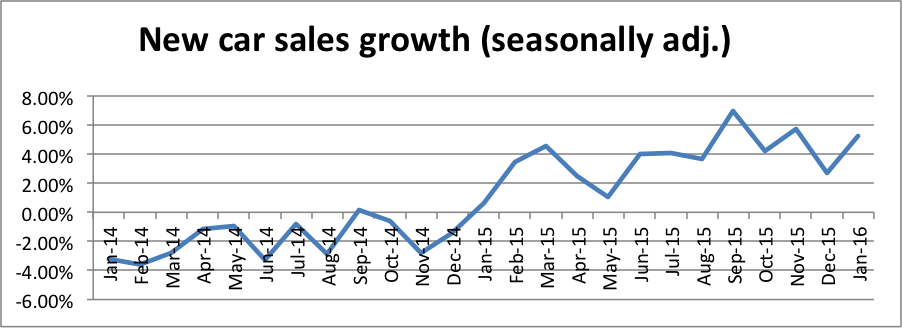

Once again, the Automotive division led the business and contributed the lion's share of both earnings and growth. Pleasingly, the Auto sector is experiencing positive headwinds, with low interest rates and lower petrol prices providing a catalyst for a strong underlying demand for new vehicles. This can be seen in the retail auto sales numbers released by the ABS over recent months:

These healthy growth levels led to growth in the Automotive division of 15.2 per cent in terms of EBIT contribution, from $61.7m in the pcp up to $71.1m this half, and profit before tax of $61m, up 18.5 per cent. This was driven by strong organic growth in NSW, QLD and VIC operations, a record performance in NZ and additional contributions from acquired dealerships. The growth in this division is encouraging and appears sustainable for the full year.

Refrigerated logistics was a weaker result, largely due to increased depreciation and weaker transport volumes. That said, the division still made a material contribution to EBIT at $16.6m, down 9.6 per cent on the $18.4m delivered in the pcp. This division has since been the subject of a review and management restructure, as the company looks to continue to invest in its growth. We remain confident that the refrigerated logistics part of the business will offer meaningful growth to the group, but acknowledge that this may take longer to materialise than previously expected.

Finally, the “Other Logistics” division of the business delivered a slower result as well. EBIT was down from $4.2m to $1.8m as the Covs Parts business contributed less, and a downturn in mining impacted demand. We expect that this division will continue to underperform, but note that it is becoming an increasingly smaller part of the overall group.

Key take-away and outlook

AHG is well placed. The key takeaway from this report is that the company continues to deliver, and is operating in a market that is showing strength across a weaker underlying economy. In our view, this should see AHG trading at a higher premium than currently seen in the share price. However, the positive side of this is that the shares are providing a strong stream of growing dividends. The outstanding long-term track record of the business has continued this half, and the company is now well positioned for the future.

AHG do not provide guidance in terms of expected profit or earnings. That said, commentary from the company's management team and board was quite bullish in terms of the demand side. Given this, we are comfortable with AHG remaining a buy recommendation, and lift our valuation slightly from $4.57 to $4.74.