iCar Asia delivers record receipts

Recommendation

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

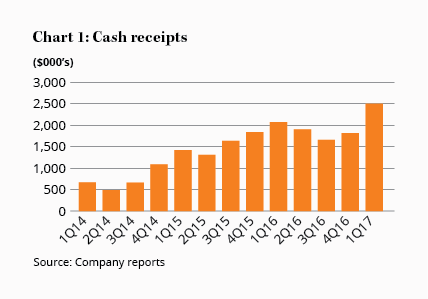

After the period of declining cash receipts that bedevilled iCar Asia in 2016, the 2017 year has started with a bang. First quarter cash receipts were $2.5m, up 21% on the same quarter last year (or 29% ignoring foreign currency movements, which was of course the figure management preferred to highlight). Chart 1 shows the trend of cash receipts in recent years.

Operating metrics also continue to move in the right direction, as we noted in iCar Asia: Result 2016. What's particularly pleasing is the performance from Malaysia, which is both iCar Asia's most important market and the most commercially developed of the three countries in which the company operates (the other two being Thailand and Indonesia). March listings and leads in Malaysia grew by 51% and 64% respectively.

It's obviously pleasing to see improvement in iCar Asia's financial and operating metrics. And the share price has responded, rising 18% today. So was last year just a bad dream?

Key Points

-

Cash receipts growing again

-

Improvement driven by marketing spend

-

Capital raising still looks likely

No. iCar Asia's problem remains the same – it probably does not have enough cash to get through to break even. As happened last year, the company could be forced into raising capital at an inopportune time. Regular capital raisings mean shares on issue have surged – up 46% since we first upgraded the stock in iCar Asia's road to riches back in April 2015 and more than 500% since listing in 2012.

Indeed, the problem is getting worse because iCar Asia's costs continue to rise. Marketing and staff costs are forecast to rise sharply in the current (second) quarter as iCar Asia accelerates its growth in the new car market and moves into ‘offline' event management (it is involved in a new car exhibition in Kuala Lumpur next month).

By 30 June, we forecast iCar Asia's cash balance will have dwindled below $19m (from $24m at the end of March). As we said in iCar Asia's bright side, it will probably need to raise more cash in 2018. The company is probably best owned by a larger classifieds company with deep pockets.

Should the share price excitement continue, our trigger finger will be getting itchier. However, as this was always a speculative situation - and there is some definite improvement in the operating metrics - we're content to HOLD for the time being.

Note: The Intelligent Investor Growth Portfolio owns shares in iCar Asia. You can find out about investing directly in Intelligent Investor and InvestSMART portfolios by clicking here.