Healthscope, and how to spot a salmon

Recommendation

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Indepth analysis of ASX listed shares

- BUY, Hold and Sell Recommendations

- Ideas Lab

- Special Reports

- Alan Kohler’s Weekend Briefing

- Interviews with CEO’s & top influencers

- Money Cafe and Talking Finance

- Super Advice and Q&A with Ask Alan

Booms, busts, fashions and fads have been part of the investing landscape almost since the beginning. Today it's all about dividend yields, ‘Trumponomics', and a second wave of dot-com bubble hysteria. When it comes to the healthcare industry, few stocks have as much glam as Australia's two largest hospital operators, Healthscope and Ramsay Health Care – and there are plenty of good reasons for that, which we'll get to in a moment.

Healthscope's share price, however, has fallen around 30% since the company warned of slowing volume growth in October. Is this an opportunity or a time for caution?

The Bull case

Key Points

-

Strong tailwinds from pipeline

-

Debt, cash flow, CEO add risk

-

Lowering price guide; Hold

Let's start with a helicopter view of the sector. The number of Australians over 65 is expected to double over the next 40 years, and that cohort currently accounts for a third of healthcare spending despite representing just 14% of the population. What's more, by 2055 some 5% of the population will be over 85 compared to just 2% today – an increase of almost 1.5 million people. As far as writing in stone goes, increasing demand for hospital care is as deeply etched as it gets.

Private hospital operators have a formidable ally: the Government is doing all it can to offload people from the strained public health system and is cutting public hospital funding by almost $50bn over the next 8 years. The need to outsource more services to private operators is expected to increase and the Government already spends $3.7bn a year on subsidising private in-hospital specialist procedures.

Healthscope, which owns one in six private hospital beds, is well placed to take advantage. Many of its hospitals are regional monopolies and the industry itself offers plenty of barriers to entry: the cost of building and accrediting a new hospital is immense. Healthscope's market position isn't impregnable but we expect it to gradually increase its share of the private market from today's 16% at the expense of smaller operators.

Between now and late 2018, various expansion projects are expected to add almost 1,000 new beds and 50 theatres to Healthscope's network – a 20% increase in capacity – which should ensure faster revenue growth than the overall market as these projects come online. To put sizzle on the steak, Healthscope's new billion-dollar Northern Beaches Hospital is (miraculously) three months ahead of schedule.

Since 2011, increasing demand and utilisation has helped lift Healthscope's revenue by 17%, yet costs have increased by just 12%. That 5% difference may not sound like much but, with hospitals operating on thin margins, this seemingly small improvement helped boost net profit by 66% from $106m to $176m over the past five years.

With a backdrop like this, it's no wonder the company has filled its pews with believers.

The Bear case

US private equity giants TPG and Carlyle bought Healthscope for $2.6bn in 2010, did some fiddling, then re-listed the company for $3.8bn in 2014. If David Attenborough was telling the story, this is the moment the hungry bears waiting on the riverbank look up and spot the salmon.

If there's one mob that can control costs, it's private equity, so all that margin expansion since 2011 came to an abrupt end in late 2015. The low hanging fruit had been taken.

Furthermore, an old private equity trick is to juice up earnings using tax losses crystalised during the business's reorganisation to offset profits earned down the track. Healthscope had $248m of these ‘deferred tax assets' in 2014, but that has been whittled down to $120m as of the most recent interim result.

The effect is two-fold: while the losses are being used, Healthscope pays almost no tax. In 2016, the company handed just $13m to the ATO despite pre-tax profits of $252m – a tax rate of just 5%. This is why Healthscope's dividends are unfranked and, with $120m of deferred tax assets still up its sleeve, this is likely to go on for another couple of years.

The lack of taxes also artificially boosts the company's current free cash flow but, when the rate normalises, we expect cash flow to fall by $60m or so.

Unfortunately, Healthscope is already in a precarious free cash flow position because the bills are flooding in for the various construction projects mentioned above. In the 12 months to December, the shortfall between cash coming in and cash going out was some $160m, and this has been a recurring trend for the past few years.

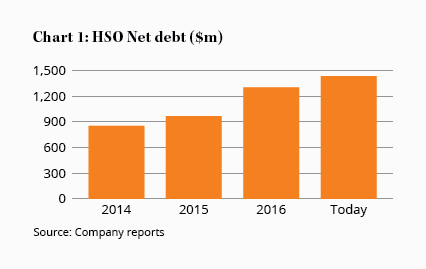

To compensate, the company has borrowed heavily: net debt has risen from $854m in 2014 to $1,423m today.

Red flags

Hospitals are high-quality, stable assets and can handle a decent chunk of debt. However, in February, Healthscope flagged slowing growth in admissions. Its hospital division only increased revenue 3% due to poor volume growth in the six months to December, despite the overall Australian private hospital market growing 5% during the period – and Ramsay increasing revenue 9%.

Healthscope is losing market share, which may suggest operations aren't running all that smoothly under the hood. Its expansion projects hold a lot of promise – and should claw back the lost market share and more, eventually – but a lot depends on whether these projects live up to expectations. If they don't, the company's leveraged balance sheet could come back to bite.

The private health insurers won't make life any easier and they're already being more aggressive in pricing negotiations with private hospitals. It is taking longer to agree on terms and they're tending to be stricter.

To combat declining affordability, over the past decade the proportion of private health insurance policies with exclusions like obstetrics has increased from 8% to 36% so, to avoid high out-of-pocket expenses, more and more patients may favour public hospitals. With a large proportion of Healthscope's costs being fixed, a margin squeeze is a real possibility if volumes go backwards, though the odds of that seem low.

There are other red flags, too. After six years in the role, chief executive Robert Cooke stepped down earlier this month and was replaced by Gordon Ballantyne.

When a captain heads for the life rafts, it always gives us pause. More attention-grabbing, however, is that his replacement has barely any experience in healthcare, let alone experience running a network of hospitals. Ballantyne's most recent role was as an executive of Telstra's Australian retail business, with previous jobs at Hewlett Packard, T-Mobile and Dell.

None of this guarantees that there's trouble on the horizon, but history sets a good precedent: new chief executives often air any dirty laundry at the start of their term so that they can work with a clean slate – and private equity reorganisations tend to accumulate mud. This upcoming full-year result would be the perfect time to ‘reset' expectations.

Price guide

Healthscope's management expects growth to be slow in the second half of the financial year with the Hospital division likely to achieve earnings before interest, tax, depreciation and amortisation (EBITDA) growth similar to the first half (up 2.2%).

The stock sports a price-earnings ratio of around 20 based on consensus estimates for 2017. Can Healthscope meet the growth expectations embedded in that figure? Given its economies of scale, expansion projects and an aging population, we wouldn't bet against it.

Nonetheless, we're getting increasingly twitchy eyebrows with how the story is unfolding and we don't want to be caught upgrading too early. On that basis, we're lowering our maximum portfolio limit for Healthscope from 7% to 6% and our Buy price from $1.80 to $1.50 to give us a wider margin of safety. We're still a long way from where we'd Sell the stock – which itself falls from $3.50 to $3.00 – so, with several competitive advantages and stable revenues, we're sticking with HOLD.

Recommendation