Flexigroup is still a buy

Silence on the numbers

Over the past few months, consumer-lending business Flexigroup (FXL) has announced the completion of its acquisition of Fisher and Paykel Finance (FPF) and another securitisation of receivables from its Certegy business. While the completion of the acquisition is a positive – in that it occurred a couple of weeks before our expected completion date – the company has yet to provide the market with an update to its cash net profit guidance. While a successful debt issuance through a securitisation is a mild positive as well, we are keenly awaiting any updates to company guidance in order to understand the expected earnings contribution and integration benefits of the FPF acquisition. For now, we are comfortable in our recommendation on FXL, but note that the longer the wait is for the company to provide an update, the more we see risks building.

What are the risks?

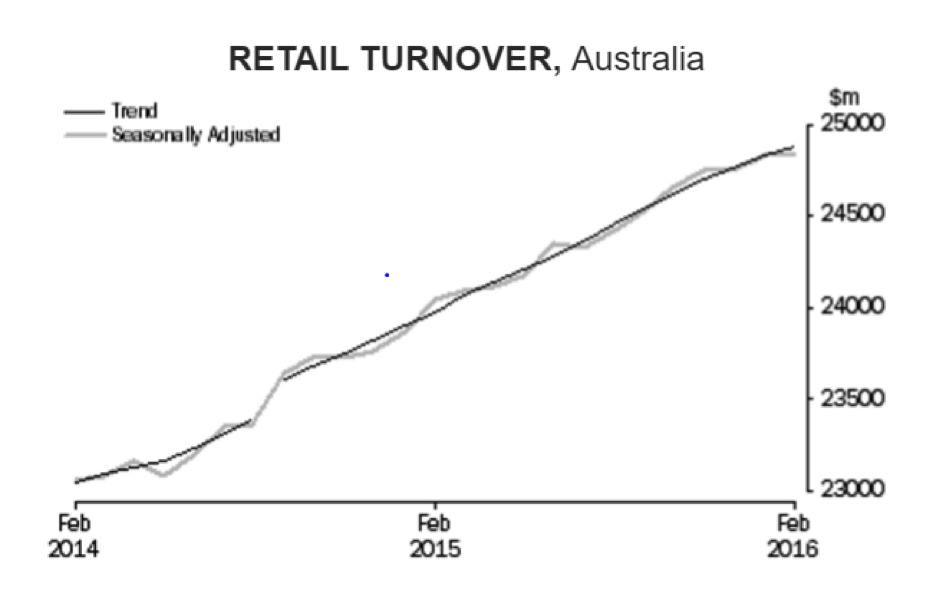

Consumer behaviour and regulatory risks are the two major concerns for Flexigroup. Despite uncertainty in the macro economy, retail sales data from the ABS has been relatively stable. Consumer behaviour is a concern and there is a pessimistic level of expectation built into the share price at current levels. FXL's exposure to this key risk is significant, but given the recent trends we are comfortable that the price is factoring in more than the current data implies on the downside. Here's the recent sales data:

With the market concerns about the potential impact of weaker retailing, there is an additional underlying regulatory uncertainty. The media has been picking up on potential legislative changes to cap the earnings made on certain consumer loans, as an extension to recent reviews of payday lending. The proposal is a theoretical extension of the small amount credit contract (SACC) law changes that are being investigated at present. While we acknowledge this is a risk, we note that the review is more likely to target payday style lending than the structured finance and longer term financing provided by FXL.

Nonetheless, the uncertainty will continue to plague the share price.

Waiting for an update

FXL announced another securitisation of its Certegy receivables, and continued to provide an innovative approach to lowering funding costs with a “green tranche” to its latest debt issue. This is a welcome announcement and shows that the business still has capacity for growth on the funding side.

However, FXL has yet to update the market on its cash net profit guidance for FY16. Upon completion of the FPF acquisition, the company notified the market that it would provide an update on cash net profit after tax (NPAT) expectations to include the FPF acquisition, but we are still waiting.

Summary

FXL is a strong innovative business, operating in a niche space. There are pressures building. However, the acquisition of FPF and the strength of the company's core operations leads to the conclusion that the stock is very cheap at present. In our view the share price factors in the key risks, and offers shareholders the potential for strong returns. We retain FXL as a buy recommendation, noting the high risk nature of the call. Our valuation is unchanged at $3.22 ($2.39 today).