Disney hits light speed

This company needs no introduction. Most of us and our kids have grown up with the iconic Disney characters. What some investors might find surprising is the scope, scale and profitability of Disney's US and global media properties.

Walt Disney has four distinct business segments: Media Networks, Parks and Resorts, Studio Entertainment and Consumer Products.

Media Networks includes cable and broadcast properties ESPN and the ABC Television Network. In the last quarter it represented over 46 per cent of revenues.

Parks and Resorts operate The Walt Disney World Resort in Florida and the Disneyland Resort in California as well as “Disneylands” in France and China. It represents 30 per cent of total revenues.

Studio Entertainment is 13 per cent of revenues. It produces and acquires live-action and animated motion pictures for distribution to the theatrical, home video, and television markets.

Consumer Products licenses the name Walt Disney, as well as the group's characters, visual, and literary properties. It is 7.7 per cent of total revenues.

Disney, in my view, should be considered a core holding for investors who want a broad exposure to global media. Disney generates consistent top line revenue growth and can still grow earnings at a mid-teens rate. A reacceleration of growth from its Parks expansion and the Lucasfilm acquisition (Star Wars/Indiana Jones) could well provide upside surprise going forward.

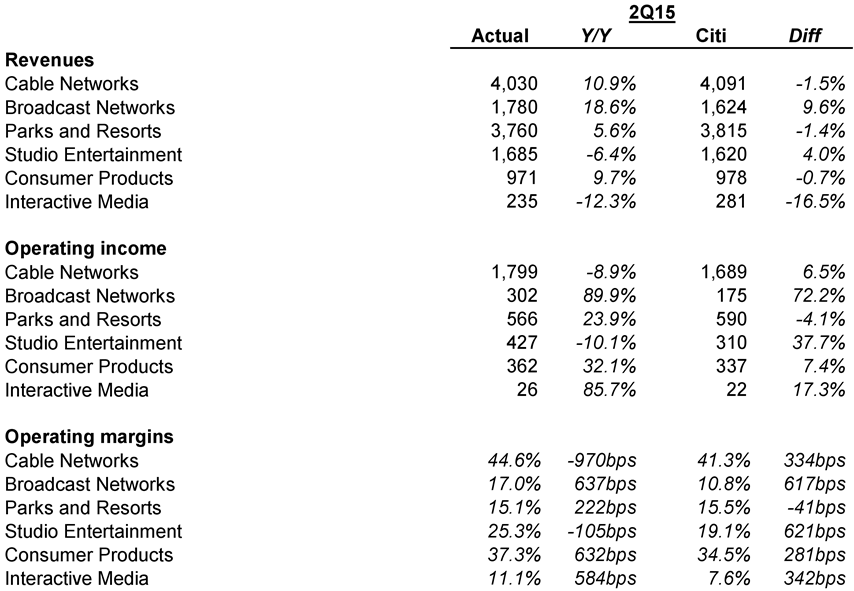

Disney reported second-quarter earnings on May 5, 2015. The segment breakdown is illustrated below.

Total revenues were up 7 per cent to 4US12.46bn, slightly above consensus. Earnings per share (EPS) of $US1.23, however, beat consensus of $US1.10 – a wide margin.

Studio Entertainment, Broadcasting, Consumer Products, Parks, and Interactive were all ahead of expectations on better-than expected operating income growth. The outlier was the Cable Networks division, which saw operating income down more than expected owing to one time cost pressures at ESPN which nevertheless saw advertising revenue up 18 per cent year-on-year.

Second-quarter studio outperformance was driven in part by strong Cinderella box office results. Given Disney's calendar year 2015 release slate (two Marvel films, two Pixar films versus none last year, and Star Wars), studio results are very likely to impress going forward.

Operating income growth at Parks of 24 per cent year-on-year was due to MyMagic (the new mobile interactive reservation, scheduling, and ticketing system), which drove 7 per cent growth in per-capita spending. With roughly 50 per cent of Disney's park guests now opting for the Magic band, I expect continued park revenue and margin growth as MyMagic achieves higher penetration rates and we move into peak holiday season in the third quarter.

Consumer Product (CP) revenue growth year-on-year of 10 per cent was a bit better than consensus. Licensing growth was driven by Frozen and to a lesser extent Avengers. Given the upcoming content catalogue, I expect licensing growth to have an ongoing favourable margin impact for the CP business.

The investment case for Disney is based on a consistent continuation of the trends, not just seen in the most recent earnings release, but also in the last six consecutive quarters where Disney has been able to beat consensus on the basis of being in front of media trends and displaying operating excellence.

The next leg for Park earnings will come from the almost completed Shanghai Disneyland and Avatar Land (opening early 2017 in Florida). Consumer products will benefit from further incorporation of Frozen and upcoming Star Wars properties as well as the recent opening of Disney's largest retail outlet in Shanghai.

Disney's studio pipeline (in spite of the Tomorrowland disappointment) remains one of the best in Hollywood. Its ownership of Pixar, Marvel Entertainment, Disney Animation, and Lucasfilms is a huge competitive advantage.

The 2015 and beyond release chart shown below, as one industry commentator commented, is “an embarrassment of riches”.

Media Networks revenues are set to accelerate as well with ESPN well positioned with its almost total dominance in sports broadcasting and the ABC network beating expectations on retransmission fee growth and higher ratings as well as the uplift for owned and operated stations (O&O) from the upcoming presidential elections.

Valuation and recommendation

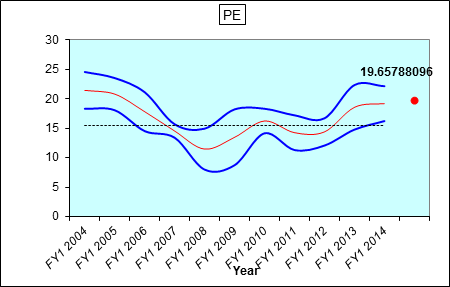

Disney currently trades at 18.3 times 2016 EPS.

Disney is a “buy” at current prices. My target price is $US135.00, based on 22 times 2016 EPS of $US6.15.

That's at the upper end of the ten-year PE range but I believe that Disney deserves a premium multiple.

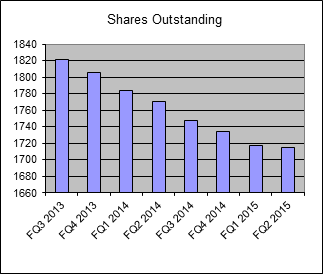

Disney's balance sheet is strong and somewhat under levered leaving plenty of room for acquisitions. Strong FCF generation allows for continued share buybacks and return of cash to shareholders. Note decreasing share count below:

Street view

23 analysts have a buy recommendation on the stock and another 14 have hold calls. There are no sells.

Risks

Risks include the following:

- A worsening economy could hamper results in several areas, notably in theme parks and ad-based areas like TV and cable networks.

- A weaker-than-expected Studio slate could hurt earnings growth.

To see Disney's forecasts and financial summary, click here.