Dick Smith's decent dividend

Since hitting the ASX boards in late 2013, Dick Smith Holdings (DSH) has seen its share price pretty much stagnant. This is despite a strengthening outlook for the retail sector and a seemingly strong start to life as a listed entity when the company beat its FY14 prospectus guidance.

Pleasingly, DSH is a business that runs with minimal ongoing capital requirements. Its growth strategy will necessitate some cash spent on new store openings, but the general ongoing business produces strong operating cash flow that can be utilised to pay dividends to shareholders. Our forecasts anticipate that DSH will be in a position to pay a 5 cent final dividend, taking the full year payout for FY15 to 12 cents. We note that this is reflective of a payout ratio in the middle of the company's indicated 60 per cent to 70 per cent range, but that the first half dividend is larger than the second due to seasonal factors that impact profits and cash flow (Christmas shopping).

Earlier this week media speculation started to circulate that DSH was potentially going to lose its contract to embed itself in David Jones stores. While we believe this is only a rumour, we also believe it would be an immaterial change to the business, with DSH CEO Nick Abboud suggesting the impact would be less than 3 per cent of total DSH sales. As such, the recent share price stagnation and weakness could be providing a good entry opportunity. The company pays a strong dividend stream and holds a promising outlook. Thus DSH will be one of our first stock inclusions in the income first model portfolio.

Eureka Report originally called Dick Smith a general purpose 'Buy' back on March 16 this year when the stock was trading at $2.05. We reiterated that call on May 18 when the stock rose to $2.70.

A shrewd dividend policy, but there are risks to franking credit balances

DSH management outlined in its prospectus that it would pay 65 per cent of pro forma net profit as dividends. It did just that, and intends to continue to support its 65 per cent payout ratio into the future. We think this is a prudent level given that there is a need to fund the capital expenditure associated with new store openings over the coming few years. Once the business has reached a point of saturation, and maturity, the payout ratio may be lifted. But for now, a payout ratio much higher than 70 per cent would lead to questions around growth opportunities. Given our forecasts, we are expecting at least a 5 cent dividend to be paid to investors with this result. This places DSH on a trailing dividend yield of around 5.8 per cent. As at the company's last annual report, DSH had a zero franking credit balance. For us investors who value the additional tax benefits of franking credits this has the potential to be a little disappointing.

We recently spoke to DSH about this issue, and noted that the company is expecting to frank the final dividend. We would expect that this can be achieved through a reach into the future to utilise franking benefits. This may sound odd, but Telstra did exactly this only a few years ago. For now, we are comfortable in our expectations that DSH will generate the profits and pay the tax necessary to frank future dividends. That said, the company's franking balance is a point that will need ongoing monitoring.

Refining our view

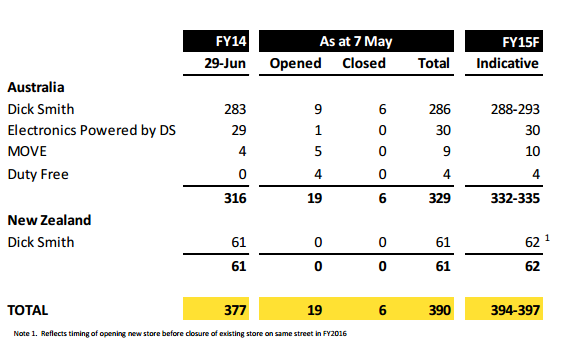

We remain comfortable that the outlook for DSH is bright, and retain our buy call on the stock. The company is expanding its footprint, with an anticipated 390 stores at the end of FY15, likely to expand to a more aspirational 420 to 430 by the end of FY17. But there are more movements in the landscape that make this buy call all the more interesting.

The budget in May was a potential catalyst for a strong fourth quarter to FY15. Thus we think this coming financial report (the full year results for the 2015 financial year) could be boosted by a strong finish. In addition, the press is awash with talk of attaching a GST to foreign retailed goods. This could increase the competitive relevance of companies like DSH and its competitors (namely HVN and JBH) when we consider the online portion of the business. It is these exciting potential price catalysts that combine with a solid business outlook to provide us with the confidence to make DSH our first inclusion in the Income First portfolio.

Store roll outs the key to growth in the near term

DSH is achieving decent like-for-like sales growth, around the 2 per cent – 3 per cent mark when compared to last year. We believe that the near term catalyst for additional growth is the company's new store roll out strategy, targeting 420 to 430 stores by FY17. This strategy, and its execution, will be critical to the company delivering on our expectations. The returns on invested capital for new store roll outs are attractive, and should continue to add value to the business in the short to mid-term. However, as with all retail expansion strategies, maturity will not be far away. We will continue to monitor this, with a keen eye on the marginal profitability of each new store. For now, we expect growth to be generated, and for that to translate into both cash flow and dividend growth in coming years.

Source: Dick Smith Holdings

FY15 financial results expected August 18

DSH will announce its financial results for the financial year ended June 30, 2015 on August 18 before market open. At this stage, we believe that DSH has provided very clear indications of what to expect. Guidance to the market has indicated that sales revenue will lift by around 9 per cent, with net profit and earnings per share to have lifted by between 3 per cent and 5 per cent each. For us, this guidance is achievable given that the company's update in May indicated the business was ahead of the curve on a pro rata basis. As such we are expecting the result to achieve near or just above the higher end of the range indicated by the company. A summary of our forecasts for this result is set out below:

Dick Smith Holdings | FY15e ($m) |

Revenue | 1341.92 |

Cost of Sales | -1009.79 |

Cost of doing business | -250.94 |

EBITDA | 81.19 |

EBIT | 64.25 |

PBT | 63.80 |

Net profit | 44.66 |

I think it is worth noting that our forecasts are slightly more bullish than a consensus of peers in the analyst community. That positive disposition stems from the belief that DSH may have had a better fourth quarter than previously expected, resulting from better consumer confidence, and a potential post-Budget boost.

Inventory management and cash flow timing

DSH has provided the market with some further information as to cash flow timing this year. The company took advantage of a higher Australian dollar earlier in FY15, purchasing inventory earlier than is otherwise normal. This will cause a blowout in working capital in the company's FY15 result, leading to a poor reported operating cash flow number. While this is a concern and should not be treated lightly, we are of the view that the cash flow drag will unwind in FY16, providing that the company does not employ the same inventory timing policy again. It is evident that this type of scenario is one that creates risk, and is probably our largest reservation when assessing the company's propensity to pay growing dividends.

Allaying those fears is the company's conservative balance sheet. With guidance for between $35 million and $45m of net debt at the end of June, the company's gearing will remain near the conservative 25 per cent level. So, we aren't panicking just yet. But the reason that this is concerning is that the cash flow timing excuse is a notorious one, and can be a precursor to future problems. For now, this scenario has created a situation where one could argue that the company is borrowing to pay dividends. We prefer to give DSH the benefit of the doubt on this, and acknowledge that the working capital management in consumer electronics is a key driver of profitability, despite the temporary cash flow issues it can cause.

Potential issues always lurk in retail

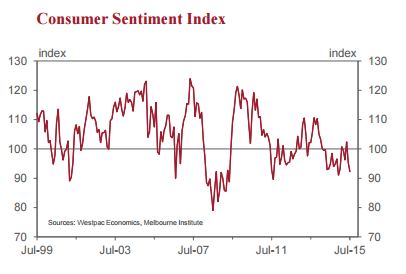

Unfortunately, retail stock investment never seems simple. We know this from experiences monitoring MYR, DJS, and the raft of now ‘cheap' or even delisted businesses that failed to move with the times. Relevance is a key risk at present as there are differing signals emerging from consumers and from businesses. There has been a recent divergence in consumer and business sentiment. In fact the Westpac consumer sentiment survey showed that in July consumer sentiment fell to a low for 2015, highlighting some of the risks in retail associated with an often fickle consumer:

Source: Westpac economics research

Aside from this risk, we believe the other challenge facing DSH is that associated with competition and technological change. Consumer electronics is, in our view, an extremely competitive space. The need for a company to stay in touch with trends is increasing. We are pleased that DSH, particularly with the expansion of the Move by Dick Smith brand, is addressing this. DSH recently partnered into a duty free store in Sydney airport, and is pleased with how this store is faring. This is a strategy in which we see significant potential, and we would not be surprised if the company invested further in its presence at International airports.

Finally, it is our view that DSH appears to be faring well in the competitive landscape, with private label products and the ability to attract customers continuing to assist gross profit margins. The strategy of presence through multiple brands and location types (Move, Dick Smith and department stores), coupled with investment in the online business, is allowing the company to address a broad market and access new potential customers.

Income First portfolio exposure

DSH will be one of our first stock inclusions in the Income First model portfolio. As outlined above, the company is in the midst of a growth strategy that should bear fruit in the form of higher earnings and higher dividends. At current prices the business is inexpensive; a FY15 price to earnings ratio of around 11 is undemanding. Additionally, this lower share price has provided an attractive dividend yield. Our valuation of $2.63 indicates there is a reasonable level of upside should the company execute on its growth strategy as planned. The company will report financial results on August 18, which has the potential to drive sentiment in the short term.

To see DSH's full forecasts and financial summary click here.