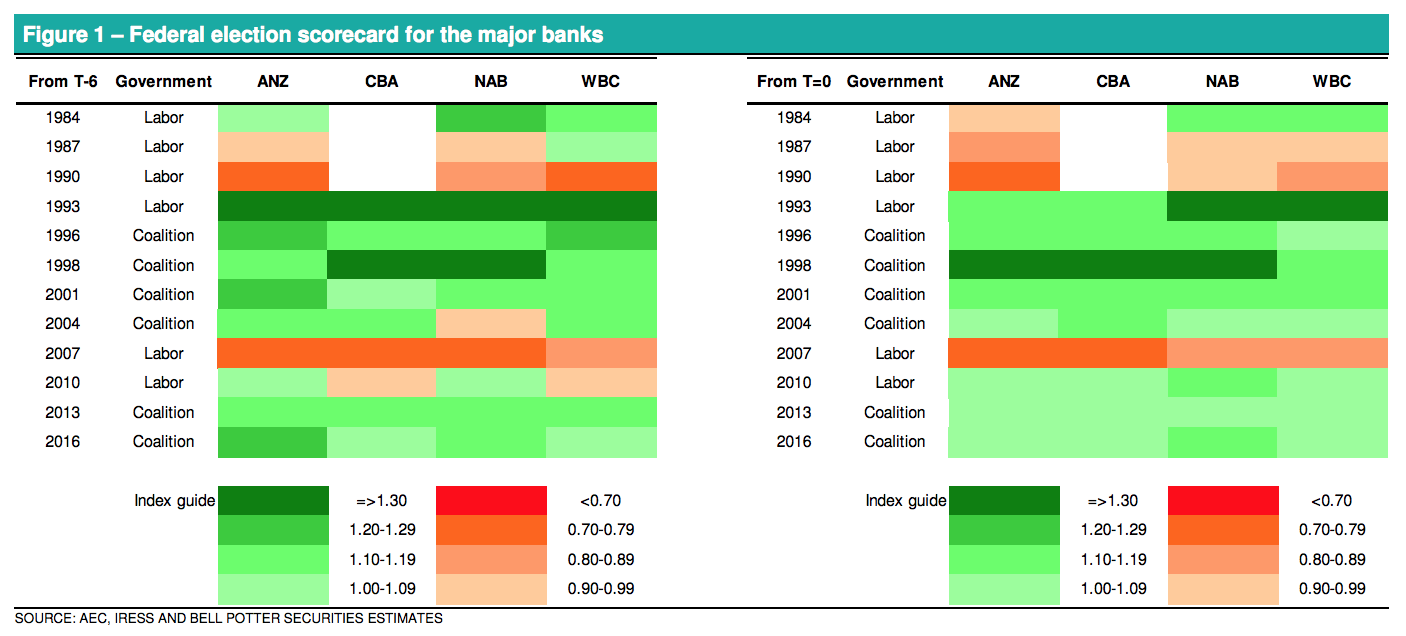

Are banks 'bull' steam ahead?

‘Don’t get carried away’ is the message for investors now expecting a sustained housing recovery.

With the Coalition returning to power, it’s more or less ‘business as usual’ — a modus operandi that Australians backed with conviction. Importantly, that means no changes to negative gearing or capital gains tax, among many other things.

To cap it off, a couple of days after the showdown, the Australian Prudential Regulation Authority (APRA) has scrapped its 7 per cent serviceability buffer for home loans. Now the banks will no longer have to assess would-be borrowers against an interest rate floor of 7 per cent. They can once again set their own minimum rate floor, with the advice of incorporating an interest rate buffer of 2.5 per cent.

The Big Four are currently averaging around a 7.25 per cent serviceability floor. The head of Australian economics at ANZ, David Plank, says this will come down to "something with a 6 handle on it".

It may seem like the property sector, and its constituents, are back in the clear.

In the immediate aftermath, the market has bounced, with housing-related shares among the biggest leapers. From SMSF administrators to retail banks and household consumer names, many of these stocks had been sold down in anticipation of a different result.

Bank shares on Monday more than doubled their post-Royal Commission single-day gains in many cases. The rally had enough mettle to break the decade's record for single-day bank share price rises, with Monday making history as one of the best days for the banks, ever.

Retail investors returned to the bank trade, a move seemingly supported by long-held tradition (see below), but those monitoring the markets day-to-day still look to be taking a different view.

Saxo Bank Australian market strategist Eleanor Creagh is approaching the recovering bull with caution, claiming not a lot has materially changed. The banks are suddenly on a tear, despite the fact their fundamentals remain much the same.

“It’s putting a heavy bid under the banks, but I wouldn’t be too sure how long it would last — the outlook is still pretty challenging,” says Creagh.

“Banks are still going to continue under pressure, there are headwinds from decelerating housing credit growth, particularly in the ANZ and NAB interim reports — ANZ credit growth year-on-year actually slowed — and the property market is still sagging.

“Bad debts are creeping higher, maybe not a material worry at this stage, but they are edging higher, and the banks are still going to have ongoing remediation and regulatory expenses.

“I think the outlook for earnings growth is still pretty challenged. Mortgage growth is still going to remain pretty weak. I don’t think the Morrison Government win is going to stop the banks from recalibrating their lending standards. There is increased scrutiny on the capacity to service debt at the moment, and expense verification, going through people’s expenses with such a fine-tooth comb, even with items such as Uber Eats.”

“A Coalition win won’t change that.”

Heading into the election, Morgan Stanley analysts examined the Big Four to be at ‘equal weight’, which is the research house’s relative stance of ‘neutral’.

Out the other end, NAB has been promoted to overweight, while the other three majors have seen their price targets lifted yet retain their neutral rating.

Equally, behind the rating, equal weight is not necessarily a positive position. In this instance, Morgan Stanley has in fact taken a “negative stance on the major banks”.

Given the timing, and the prevailing election coverage, the upgrade may appear a result of NAB having greater exposure to the housing sector. Under a Morrison Government, the picture for property may look clearer.

But that’s not the case. Westpac has relatively more exposure to the mortgage market. (Research house Bell Potter has just reinstated Westpac as a 'buy' on the back of perceived value returning to this market, while investment bank Citi prefers Westpac over Commonwealth Bank, and NAB over ANZ.)

Morgan Stanley upgraded NAB on the basis of “potential for better business conditions, lower tail risk on credit quality and more valuation support”.

Plus, investors may consider the fact that ANZ, Commonwealth Bank and Westpac were all trading at or above historical averages on a price-earnings basis ahead of the election, even under less than certain conditions.

There may have been talk the sky would fall, but on the stock market, shares were tracking higher even in the face of looming change. On the ground, cracks had clearly appeared already around housing, but the credit squeeze has also been a heavyweight in the equation, and it’s hard to isolate the two. Housing lending is down 18 per cent on the year.

Some of the downside risk to housing may have been averted, however, incentives can’t fuel fundamentals. Analysis suggests that first-home buyers may not support the market any more than before. The Coalition’s First Home Deposit Guarantee will be limited to 10,000 loans per year, representing less than 9 per cent of first-home buyers and 2 per cent of total new lending. For now, the unknowns outweigh the knowns on this, and no other country has pulled off a similar measure for comparison sake.

“It’s probably not a game changer at this stage,” says AMP Capital chief economist Shane Oliver.

“That said, I suspect it will morph into a far more attractive home buyer grant at some point (which is something we have seen in most major housing downturns in recent times) and will add to confidence along with RBA rate cuts, improving affordability and a slowing in new supply next year to help the property market bottom out short of the worst case falls some are putting out there.

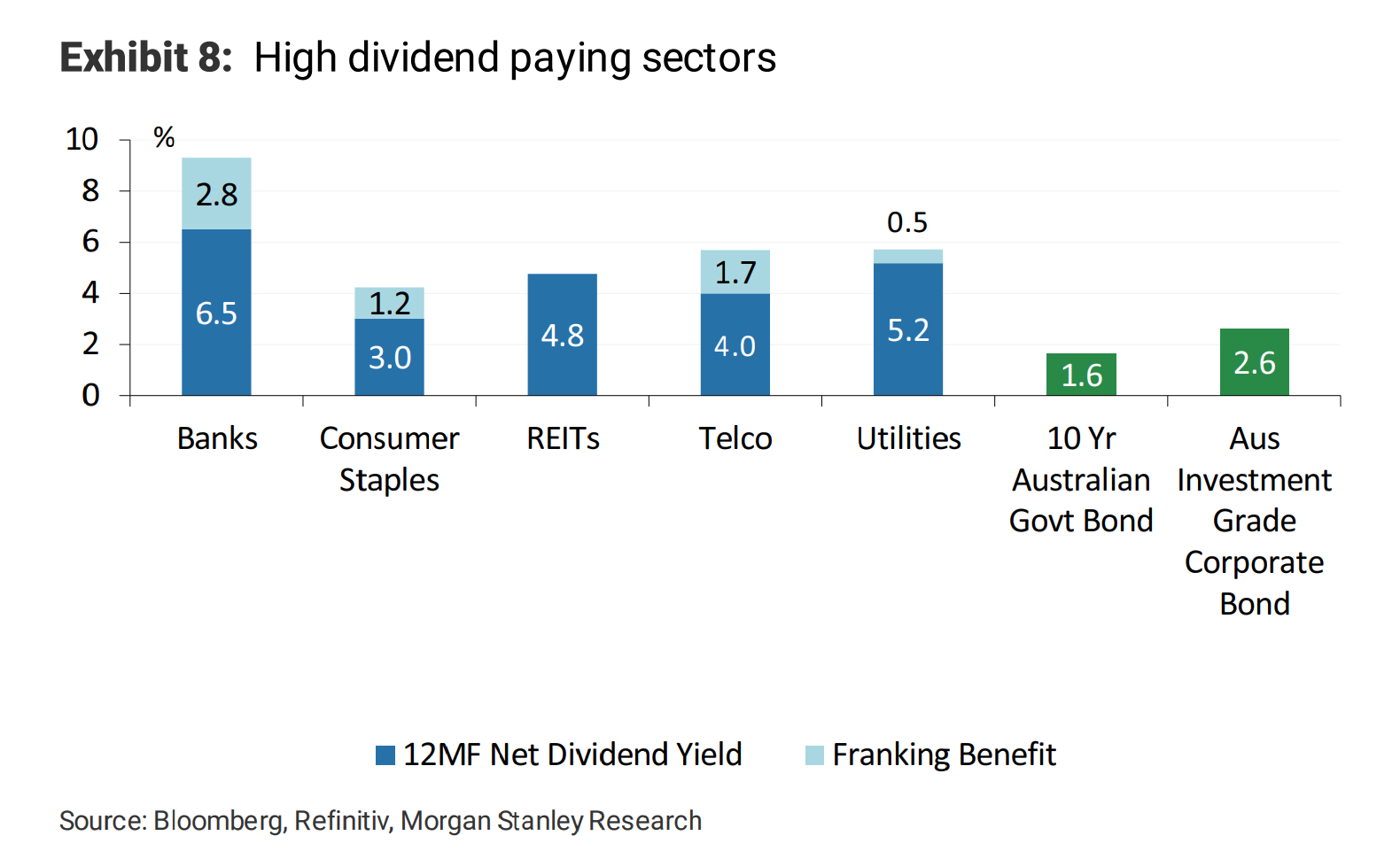

Investors may observe a “meaningful rotation” back to blue-chip yield stocks, reports Morgan Stanley, with some of the sectors below standing the biggest chance as beneficiaries.

However, on the banks, we’re more likely to see a “neutralisation” where investors close out underweight positions. The chance of sustained upside “seems limited”.

Of course, with some of these names, it’s hard to say what part of the catalyst was consumption/property to yield — or negative gearing to franking credits, in election terms.

“The other part, these moves are probably magnified by short-squeezing and sectoral rebalancing, as there were a lot of investors heavily underweight the banks,” says Saxo Bank’s Eleanor Creagh.

“It’s probably a bit of a short-squeeze on traders that were expecting a Labor win, as there would have been a few people positioned in the market ready for that, with everyone thinking it was a done deal.”

Looking forward, the next item to watch on the housing front may be auction clearance rates one week on, next weekend. This is real activity on the ground, more than switching out of stock positions.