AHG is stronger than ever

Initiation of coverage with a buy call

Automotive Holdings Group (ASX: AHG), Australia's largest owner of car dealership businesses, has performed well in recent years, posting consistent growth in underlying profits and dividends. It is this solid base of earnings and track record for delivering returns to investors that has made AHG such an interesting prospect for income seeking investors. Thus we initiate coverage of AHG with a buy call on the stock and an intention to include it in our Income First model portfolio.

A strong cash generator with earnings upside can create growing dividends

AHG is Australia's largest car retailer. The company has been around some 63 years executing its aggregator strategy by buying dealerships as they become available and consolidating the market. It is a large business by revenue but operates with high volume and low margin. The Auto segment of the business, which includes an auto parts and servicing business, accounted for 82 per cent of revenue in FY14, and has been a strong path for the company since its establishment back in 1952. Our view is that this part of the business will continue to grow above trend through acquisitions and the benefits of economies of scale. However the more exciting growth for AHG will come in the company's Logistics division, which accounted for the remaining 18 per cent of revenue in FY14.

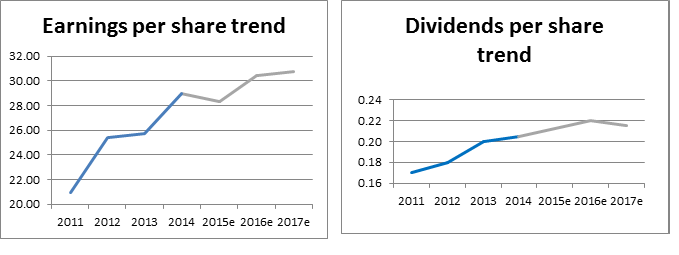

The company historically pays a strong dividend stream, and has continued to generate strong operating cash flow. In fact AHG has held close to, or above, $100 million in cash on its balance sheet at the end of each of the last four financial years. This track record is further emphasised by the below graphs showing that AHG has grown both underlying EPS and DPS in each of the last four years.

As can be seen AHG has grown its dividends over the recent past in line with growth in earnings. The outlook for the business remains promising, and our expectation is for this trend to continue (as evidenced by our forecasts in the above chart).

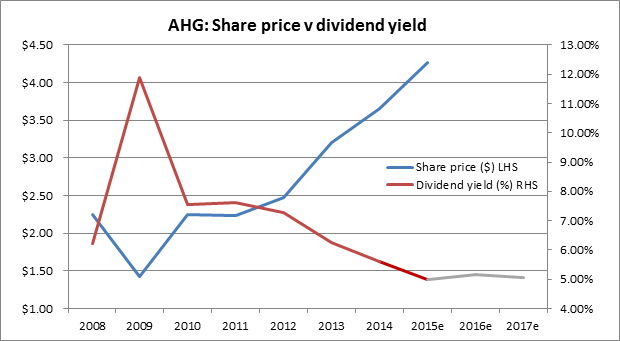

From a dividend yield perspective, AHG is trading with a cash yield of around 5 per cent (which is a touch over 7 per cent for those who gross up the yield to account for franking credits). This is a good income stream from a solid business. That said, the draw card here is that the business is expected to continue to pay a yield in this vicinity as the share price grows with the company's earnings. For example, the company has grown earnings and developed a strong track record between FY11 and FY14, leading to a share price lift of some 73 per cent (20 per cent pa). This rapid share price rise has somewhat diluted the yield to the end investor, but the company's propensity to increase dividends has supported an income stream that remains attractive.

This combination of share price momentum through track record, and dividend increases, strikes a good balance for income investors. It is particularly useful for those looking to diversify away from the dangers of unsustainably high payout ratios, and annuity-style investments that trade as a proxy for the bond market. Pleasingly for AHG the dividend yield is attractive, and recent history suggests that should the yield be eroded, the cause is likely to be a strong share price.

Balance sheet management: the key is stock turnover

There are some challenges facing the business that are intrinsic to its operations. Firstly the retailing of autos requires huge working capital to fund inventory. AHG funds this through floorplan leasing, a form of working capital financing that attaches to the stock, and is more bailment financing than debt in a traditional sense. Nonetheless, this is a form of debt, and creates obligations on the balance sheet that need to be considered, and potentially serviced.

We note that AHG, as is industry practice, reports this debt service cost as a part of its cost of sales, similar to the way costs of trade payables would be treated. While this is an area that is in our view slightly grey in terms of the nature of the debt and the potential impacts to AHG should a significant downturn eventuate, we acknowledge that the company should not be penalised from a gearing assessment perspective for working capital finance.

Given that AHG's dealership stock of cars is financed in this way that is unique to the auto industry, it is important to pay special attention to the company's inventory turnover as a measure of operating efficiency and operating margin. It is clear that the profitability of a unit of sales (one car) diminishes as the car stays on the lot accruing financial interest. Pleasingly, this is an operating metric that has been long established and is well managed by AHG.

Drivers of growth, and indicators to watch

The obvious indicator for AHG is to look at the ABS data for new car sales. Pleasingly, the auto retail sector has been quite resilient in recent months, and longer term has provided AHG with a stable industry dynamic within which to grow. Our expectations are for this stability to remain. Potentially, we will see some industry catalyst to the company's fourth quarter result with the May budget allowing some small businesses to tax deduct up front purchases up to $20k in value. While this is not going to be a material driver of a meaningful long-term growth trend, it is still a positive as we near the company's August financial statement announcement. AHG did provide us with some thoughts on this, commenting that the $20k limit isn't really of a size that is expected to impact decisions on purchasing.

Overall, the AHG auto business is quite stable, and is growing its market share by around 1 per cent per decade to a current share of around 6 per cent. The market for auto dealerships remains highly fragmented, and the slow and steady growth is expected to continue for now. Longer term risks to this model are clearly structural and will likely be driven by technology. For now, we believe that industry trends and shifts to a less fragmented selling environment favour larger aggregator operators such as AHG and its nearest competitor AP Eagers Limited (APE).

As mentioned, the company has invested in cold storage logistics in recent years. This is an exciting business with mid-term growth potential, as businesses like ALDI use more modern logistics chains to increase efficiency in the fast moving consumer goods market. We will monitor this part of AHG with great interest as the strategy develops, but for now believe most of the story remains promise rather than bankable earnings.

Ownership structure

AHG is 19.9 per cent owned by rival business AP Eagers (APE). APE is also listed on the ASX and executing a very similar aggregation strategy to AHG. It is our view that this stake is interesting to APE in a number of ways.

First, it allows APE to access market share that would otherwise potentially not be available. Why? Well, the auto dealer market is controlled by the auto manufacturers who have strict guidelines on dealer market share, most of which cannot exceed 10 per cent in one defined area. So, the APE stake in AHG allows exposure to a higher market share via the lookthrough on earnings.

Second, it is a blocking stake that it gives APE and its influential majority owner, Nick Politis, a seat at the table should anything change at AHG. From the perspective of AHG, it is not really a point of concern. However investors should be aware that this type of holding could lead to industry change and is a potential risk for the fortunes of AHG.

Risks: currency and consumer behaviour

AHG is a large scale operation, and thus exposed mostly to the macro drivers of automotive consumer behaviour and the margins available in the supply chain. Thankfully, the industry is a long established one that operates with accepted discipline in order to make operating margins rather consistent. While products are sourced from manufacturers abroad, AHG is not involved directly in the import process (except in the cases of Husqvarna and KTM), thus takes on no direct currency exposure. It is believed that in the long term, manufacturers and importers are less concerned with margins when assessing currency, but more focused on market share. As such, AHG's margins tend to have maintained stability through periods of increased volatility.

Income First portfolio inclusion

It is our intention to include AHG in the Income First model portfolio at its inception. The company will provide an interesting exposure to a business that has shown resilience through cycles, and earnings that are defensive in nature, despite a cyclical appearance. AHG's current dividend yield is compelling, and the company holds a large cash and franking credit balance giving us confidence in the sustainability of dividends. In fact it is our expectation that dividends will continue to grow with earnings as the business continues to execute its aggregation strategy. In light of the strong case, we initiate coverage of AHG with a Buy call on the stock, an initial valuation of $4.57 and an intention to include the business at the inception of our Income First model portfolio.

To see AHG's forecasts and financial summary, click here.