Why the kids are not alright

It smacks of wishful thinking to hope that a generational decline in wealth and living standards for younger Australians won't become a reality, as the Grattan Institute warns in a new report.

The growing inequality between young and old that has become apparent in the UK over the past decade, and in the US though for slightly different reasons, is exactly the future that lies ahead for Australia if there are no changes in policy settings.

The risk, as outlined in 'The wealth of generations' report and elegantly discussed by Rob Burgess (The fiscal storm confronting young Australia, December 12), is that younger Australians will have a lower standard of living than their parents did.

That is already the case for young Britons.

The causes of the disparity are similar: slower income growth for the young; the unlucky timing of missing out on the surge in house prices over the past 20 years, fuelled by low interest rates; and a sharp increase in government payments to older citizens.

Despite higher levels of education, younger Britons are generally paid less than their predecessors were at the same age.

Income growth has been stagnant in the UK for the past decade, just as economists here are warning about an income recession in Australia after the collapse in the terms of trade.

In the UK, median incomes grew by less than a tenth of one per cent each year between 2001 and 2011, down from an average of 1.5 per cent growth over the prior 25 years.

Incomes have stagnated for young Americans too. As a result, Americans aged between 25 and 34 earn about as much as the same age group did in 1965, the study found. By contrast, those aged 55 to 64 earn about 40 per cent more today than the same age group did in 1965.

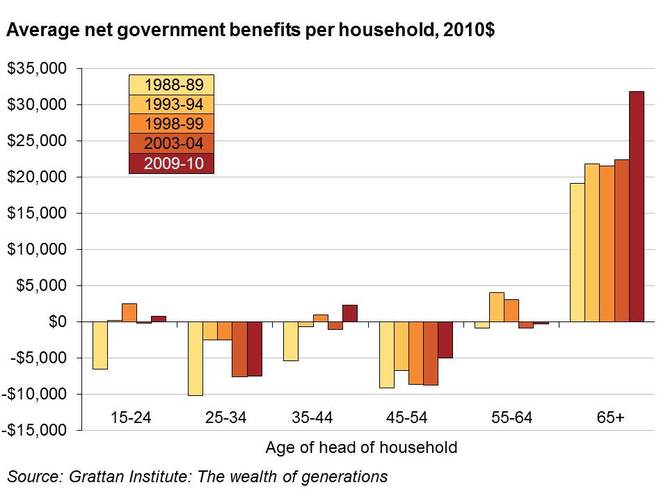

In Australia, the study found household incomes for those aged over 55 grew at the fastest pace of any age group over the past nine years, at a 3.9 per cent annual pace.

Part of the shift in wealth to older generations has to do with the housing boom of the past 20 years, which has put median house prices beyond the reach of many younger Australians and massively added to the wealth of households that already owned property -- by and large, those over 50. Most of those born after 1965 have missed out on growing wealth from house values.

In the UK, younger people are much less likely to own their homes, with only 20 per cent of those born between 1983 and 1987 owning a home at the age of 25, compared with between 40 per cent and 50 per cent for those born before 1972 at the same age.

The figures are similar in Australia. Home ownership is increasingly diverging by age, with the biggest decline among 25 to 34-year-olds. In 1981, more than 60 per cent of this age group owned their own homes, which fell to 48 per cent by 2011. For people aged 35 to 44, ownership declined 10 percentage points.

The Grattan Institute warns that an increasing proportion of Australians born after 1970 will never get on the property ladder at all.

More surprising than housing wealth is the dramatic increase in government spending on the aged, driven by increased health spending. Net benefits to older Australians have jumped, with the government in 2010 spending $9,400 more per household headed by someone aged over 65 than in 2004.

In the UK, the fiscal crisis and budget cuts have hit earlier and harder, and older Britons have had substantial cuts in benefits.

But this will barely put a dent in the figures that Daley quotes showing that a 65-year-old in Britain today will take out £220,000 more from government coffers than he puts in over his lifetime.

Yet a 25-year-old today will end up paying £120,000 more in taxes to the exchequer than he ends up receiving. (There have not yet been any comparable studies based on generational accounting out of Canberra.)

“The UK provides a cautionary tale for older age groups here,” says Grattan Institute chief executive John Daley.

“There are two ways we can deal with this. We can hope it goes away, give in to older lobby groups, don't touch age pensions, minimise asset taxation, and end up with a significant budget crunch. Or we tighten up super and asset taxation, and get budgets onto a sustainable footing.”

An index of intergenerational fairness in the UK recently found that young people were like “overloaded packhorses”, becoming increasingly burdened by other generations' debts while also loaded down with student loans that their elders did not have to pay.

In the US, economist Laurence Kotlikoff estimates that younger generations will inherit such large fiscal deficits that they would need to pay taxes of close to 60 cents in the dollar to pay off government debt. He says intergenerational inequity is the “moral issue of our day”.

Perhaps one of the ways to move forward is to ensure that our political candidates are preselected by younger people, rather than by entrenched and ageing interests.