Why the euro won't hurt you

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Verify your email address by clicking on the link we sent to {{user.Email}}

- You now have free access, we look forward to helping you on your financial journey.

Summary: European equities have performed well over the past years, especially for Australian investors when the weaker Australian dollar is taken into account. But for those who haven't yet taken the plunge, Europe doesn't look terribly attractive at the moment. The short-term boost to equities from the ECB printing money needs to be balanced against the downside pressure the move puts on the euro. |

Key take-out: It's unlikely that currency moves against Europe will wipe out returns for Australian investors over the medium term. The euro is cheap historically, with a lot of bad news – such of talk of deflation – already priced in. |

Key beneficiaries: General investors. Category: Economy. |

Back in 2012 I suggested that investors should look for investment opportunities overseas, especially in Europe, given the strength of the Australian dollar. While many lamented is purchasing power, for investors it presented a great investing opportunity.

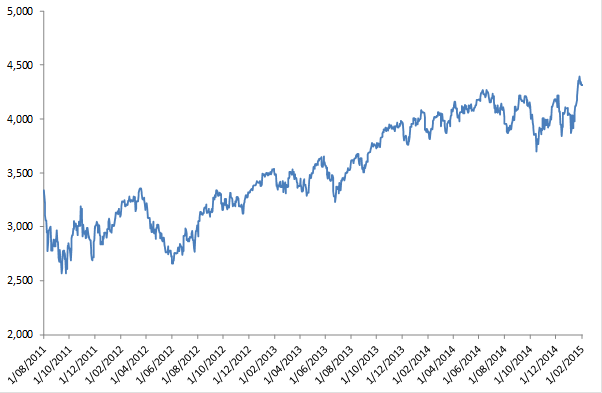

Since that time, European equities have surged 43% and 94% when you take into account the weaker AUD. It's been a very successful investment strategy as chart 1 highlights.

Chart 1: Euro stoxx in AUD terms

For investors who already hold European stocks or for those thinking of getting in, the question is now: Is it still worth it?

Part of the problem is that, on the face of it, Europe doesn't look terribly attractive at the moment. The European central bank is printing money and there are renewed concerns about Greece. While the former may give a short-term boost to European equities, for Australian investors, this needs to be balanced against the downside pressure such a move puts on the euro. Indeed both of these events trigger a very bearish euro.

It's then a question of currency risk – of whether ongoing weakness in euro will wipe out gains for Australian retail investors.

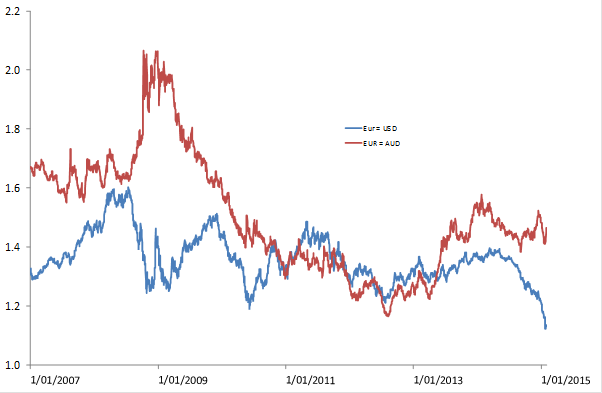

Well, the first thing to note is that investors need not panic. Or, rather, there is nothing in market pricing to suggest investors need be concerned. Chart 2 shows that while euro has been declining against USD – the euro slump is real – it has been broadly steady against the AUD even as the ECB announced its own quantitative easing program.

That's very telling. If the EUR/AUD cross rate can remain steady as the ECB prints (and during Greek political turmoil) even appreciating to a high of 1.52 in December, then I don't think investors need to be overly concerned that a weaker euro will wipe out investment gains. What we've seen over recent months was incredibly bearish for the currency, and yet on currency alone, Australian investors held onto their European gains.

Chart 2: EURUSD v EURAUD

That fact alone, while a good omen, isn't reason enough to continue holding any European investments, however. For that we have to look at the other, more structural issues over the medium term. When we do, they all suggest that over that time period, the euro is more likely to continue to strengthen against the AUD.

Firstly, while the euro may be up by 24% against the AUD (at 1.42) from its lows in 2012, it is still quite cheap comparatively. On average, since the inception of the euro area, each euro has bought $A1.6. This implies a further 10% upside to average levels, or if you want to look at the upside – a further 34% to previous peaks.

Secondly, remember that a lot of bad news has been priced in to euro at the moment. There are lingering fears that the Eurozone will dissolve, led by Greece or perhaps even Germany. This may no longer be the consensus and thinking has certainly evolved from the heady days when some claimed a Grexit was a 95% probability within a year (Citigroup back in 2010). Even so, the talk now is of deflation, ‘secular stagnation' and the lost decades not too dissimilar to what Japan has experienced.

While they gain a lot of press, both viewpoints are equally as alarmist as the Grexit notion – and just as false. It's at this point that I reiterate my view – in the strongest of terms – that both deflation and secular stagnation are either implausible or very low probability events.

Secular stagnation was a theory that was debunked in the 1930s, while deflation is simply impossible under a flat currency system – without policy support. That is, deflation cannot manifest unless policy makers, with clear intent, want it to. Past episodes of deflation have only occurred when currency was backed by something (either gold or other precious metals) and so the money supply couldn't be expanded as needed, which then caused deflation.

We clearly are not in the same world, and so while much bad news is priced in, the probability of any of it occurring is very low. This means that at some point, the euro will appreciate again – providing a good boost to a European portfolio.

It may take some years, but eventually all the fear and loathing over Europe will ease. That leaves an economic region with some of the best economic metrics in the world: A current account surplus, modest debt and smaller deficits than you see in either the UK, the US or Japan.

Economic growth will remain low – it always is in Europe – but there is nothing new in that. The structure of the economy means that European earnings growth can be solid without necessarily experiencing strong economic growth.

To conclude then, I think it's unlikely that currency moves against euro will wipe out returns for domestic investors. It's more likely that currency effects will be either neutral or upside further upside over the medium term.