Why the $A has further to run

Summary: The Australian dollar is likely to push higher, with the market seeing a large contraction in short positions and global factors being supportive. The US Federal Reserve is showing a reluctance to hike interest rates and most likely won't move until 2016, while the euro, which is highly correlated to the $A, is being bid higher amid a recovering economy. |

Key take-out: While a weaker Australian dollar has failed to bring about the desired changes, a stronger one presents no threat – as a whole – to the economy or the equity market. Rather, it draws in global investors, increases income and in general makes the country wealthier. |

Key beneficiaries: General investors Category: Shares. |

The big question on everyone's lips is whether the Aussie dollar will continue to push higher and, if so, what that'll mean for the economy and the stock market.

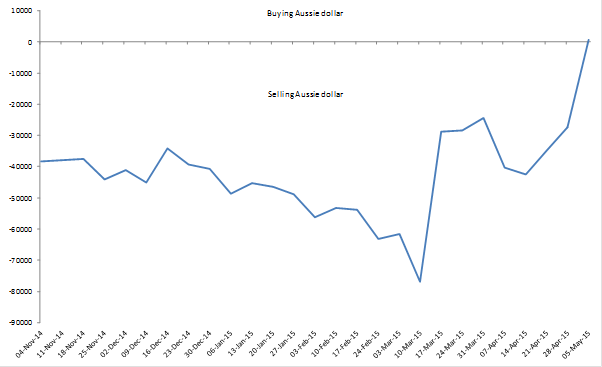

While noting how difficult the forecasting environment is at the moment, it does seem more likely at this point that the Aussie dollar will push higher. Short positions on the currency (people selling Aussie dollar futures) have slumped 35 per cent over the last couple of weeks – the biggest drop on record as far as I can tell. Certainly the biggest drop in over 20 years, in any case.

So far then, the market currently has a modest net long position (buying the Aussie dollar) for the first time since about September last year. The fact that this is driven more by a drop off in short positions, rather than a surge in long positions, doesn't suggest the market has a strong conviction on it. But neither is there appetite to sell.

Chart 1: There has been a large contraction in short Aussie dollar positions

That's fair enough. As we know, the outlook for the currency depends on global factors. The US Federal Reserve for one – and whether they'll hike rates this year or not. It's looking doubtful, that we know. For a start, some of the key US dataflow has moderated. GDP growth slowed markedly in the first quarter and is expected to remain weak in the second. Inflation remains well below target and, of course, we know that the key Federal Reserve voters have publically shown a reluctance to hike. Markets for their part are increasingly pricing in a move in 2016.

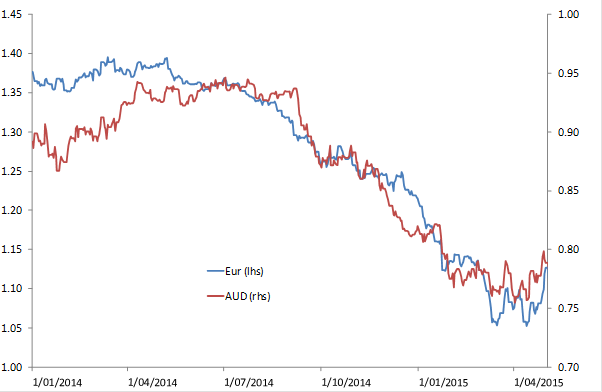

The other side of the equation is obviously Europe – well, the euro, specifically. That currency is up 8.5 per cent since a low in April and there are many supporting factors for continued strength, notwithstanding the European Central Bank's quantitative easing (QE) program.

Firstly, the European economy is picking up and is at a two-year high. Then, recent inflation outcomes show that the process of disinflation has run its course and, in response, European bond yields are rising; the spread between the US 10-year Treasury yield and German bunds is down nearly 40 basis points. That is, the gap between them is narrowing as European bond yields rise more than in the US.

This process takes some wind out of the US dollar's sails. It boosts the euro and, indirectly, the Aussie dollar. That's not to forget that the Australian 10-year bond spread is higher against the US as well.

Chart 2: The AUD and Euro are highly correlated

So it doesn't look good and it's probably fair to say that, on balance, the Aussie dollar will be higher over the next 12 months than lower – even should the RBA cut again. This isn't necessarily as bad as people have come to think though.

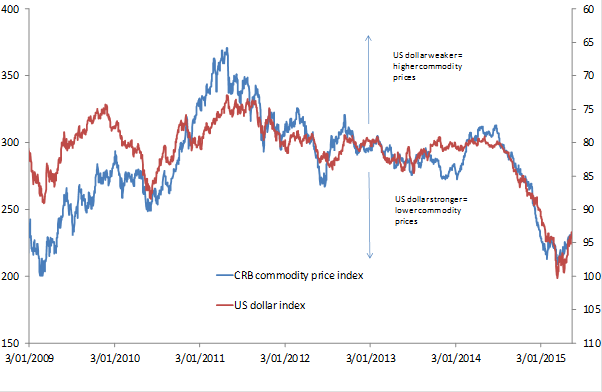

For a start, a weaker US dollar is usually supportive of commodity prices. That's because commodity prices are priced in US dollars, so the weaker it goes, the higher commodity prices usually go to offset it, as you can see in the chart below.

Chart 3: A weaker US dollar leads to higher commodity prices

Read that way, the weaker US dollar is a great signal that, at a minimum, commodity prices have stabilised or, even better, that a rebound may be due. Remember, there is little in the way of fundamental drivers otherwise to explain the commodity rout – something the Bank for International Settlements has noted itself.

Naturally enough, higher commodity prices are good for our commodity exporters and, in theory, government revenues. Either way that is the perception and it's good for confidence. This is why the Aussie dollar and our share market have usually enjoyed a strong positive correlation. As the economy strengthened and the currency pushed higher, investors bought our equities and the market moved higher.

This correlation has broken down more recently as the dollar has dropped and stocks have either increased marginally or not done much. Then again, Aussie shares have also been a perennial underperformer for some years, so the relationship hasn't gone disappeared altogether. Overall, the weaker currency can't be said to have helped the market much nor the Australian miners (since it's closely correlated with lower commodity prices).

The greater impact is that a weaker currency scares off global investors, lowers national income and weakens confidence. If global investors can have a little more confidence that investment returns won't be whittled away by exchange rate depreciation, then they may be more inclined to buy Australian stocks. In that sense, the stronger currency is a positive.

For the economy more broadly, a stronger currency acts to lift national income and generally makes the country wealthier. Retailers can import their goods at a much cheaper rate, input costs go down, etc. Think of it this way: from 2003 to 2008 the currency appreciated by 45 per cent without any detrimental effect on the economy. The country was growing at a very strong rate – as we were when the currency was hovering closer to $US1.05 in 2011.

So it doesn't have to be bad news. At the very least a weaker currency has failed to bring about the changes widely proclaimed by many economists, in any case. It hasn't helped the manufacturing sector, hasn't seen a decline in the number of outbound tourists and hasn't encouraged more foreigners to come and visit over and above what we were seeing when the currency was stronger.

Otherwise, a weaker currency has still seen our miners belted, the equity market underperform and growth remain lacklustre. The truth is a weaker currency does not help the country.

Noting this, how can a stronger currency hurt? It doesn't. It presents no threat to the economy or to the equity market – as a whole. Obviously stocks unlinked to commodity prices that derive a substantial proportion of their sales in US will face some headwinds. But, again, these need to be measured against sales and growth prospects.

What investors do need to watch out for is how policy makers behave in the wake of an Aussie appreciation. If they panic, further downgrading growth forecasts and slashing interest rates, they may prove to be a significant – but temporary – headwind to the market, as has been the case these past few years.

I'd only put it as an uncertainty though. What I'm left wondering is whether further RBA moves might be overwhelmed by the sheer magnitude of the US dollar decline. If that's the case, they may simply give up trying to move the currency – as they should. Australia's foray into the currency wars has been a failure – and that would be a very positive development indeed.