Why markets are tuning out

The Week in Review by Shane Oliver (AMP Capital)

Investor Signposts by Ryan Felsman (CommSec)

One of the best signs that you are not in a bear market and have every prospect of moving to a bull market is when bad news does not completely shatter the state of play. And so in Australia, with the Commonwealth Bank, while there is a real threat of indeterminate severity hanging over the stock, after its initial hammering it has recovered ground.

The world is watching in amazement at the exchange of threats between US President Donald Trump and North Korea leader Kim Jong-un. This is increasing the risk of war, but stock markets in both South Korea and the US keep on rising.

Earlier this year, US stock markets got really excited about the promise of tax reform, but then the chances of this were slashed, and there was an initial adverse reaction across markets. Nevertheless, interest rates as measured by the bond markets fell as a result, and that boosted shares again.

We are now seeing bond rates edge higher once again as the expectation of tax cuts gathers momentum. Trump’s tax bill is coming to a very crucial stage and he is clearly optimistic he will get this through as support for the bill gets stronger. But there are no certainties. US markets seem to be edging up on the basis that, whatever happens, shares will win — typical of a bull market.

Now, I emphasise that these are trends that ignore inevitable day-to-day fluctuations. Another threat to the trend is, if there is a sustained marked rise in global interest rates, then asset prices will fall.

Bad news isn't hitting hard

In a bear market, when there is uncertainty and bad news, the stocks involved are really hammered. At this moment in time, this is just not happening.

Why is that so? While I don’t have the genius of American physicist Julius Sumner Miller, we can use his key question to guide us around the world and unearth positive forces underpinning markets.

My first selection will probably surprise you, the One Belt One Road Initiative, a massive infrastructure operation being planned by China to link itself with Europe.

Nothing like One Belt One Road has ever been contemplated in the world before. It is going to absorb a vast amount of commodities, engineering expertise, and building capacity.

Australia is currently caught up in a series of China-related morasses, such as the long-time South China Sea dispute, and freedom of speech being thrust into the spotlight at Australian universities because of Chinese study abroad students who are affiliated with the Communist Party.

We will miss the main game of One Belt One Road but we could still be a big long-term beneficiary based on the synergy this could bring.

Both the US economy and the European economy are performing reasonably well and interest rates are very low, which is now starting to increase economic activity.

We see that in a number of metal markets, the standout being iron ore, there has been steady progression upwards. Iron ore has been getting a boost from China switching its steel output from dirty steel blast furnaces using low-grade Chinese iron ore to much less pollutant furnaces that rely on high-quality ore from Australia and Brazil. But the iron ore price could now have risen too far.

One of the very best indicators of industrial strength is the copper price. On any one day copper can move sharply up or down, but in the last few months we have seen a very steady rise in copper. It is a clear indicator of better economic activity. It is also directional – copper is one of the great beneficiaries of the move to electrification of energy. For example, renewables, which are still in their infancy on a global basis, are fuelled by re-engineered power grids that require copper. Similarly, the electric car is going to require a lot more power transmission, and again, a lot more copper.

BHP has been predicting a sustained rise in copper for some years but only now can you see the emerging forces that led to that prediction. There’s now rising demand and fewer opportunities to increase supply.

Olympic Dam is BHP’s next major project, and while it won’t be anywhere near as big as the original BHP plan, it will still be a substantial expansion. There is also movement afoot at the Kambalda mine, thanks to the much greater use of nickel in batteries. Nickel is looking better thanks to batteries, and both copper and nickel are set to trigger substantial investment in Australia by BHP.

A tailwind after the unwind

And so we come back to broader Australia stock market. At first we watched with horror the big fall in mining investment as the boom ended, bracing ourselves for a recession that didn’t happen. The banks, however, flooded the housing market with loan money, and combined with an avalanche of Chinese money, this created not only much higher dwelling prices but a dwelling building boom particularly in Sydney and Melbourne.

But the housing market is being subjected to a very severe squeeze as investor loans are being limited and their interest rates increased. Banks are also placing tougher criterion on those who want to buy dwellings to live in.

This combination of actions, driven by the regulators, has already started to impact the rate of building and it will continue to do so. But just as we start bracing ourselves for the downturn it’s now becoming clear that, particularly in New South Wales and Victoria, there is a huge build-up of infrastructure investment. Macquarie estimates planned investment of around $221 billion that’s spread over four years; the figure could rise beyond $300 billion if a few projects not yet bedded down see the light of the day.

The definition of infrastructure goes beyond roads, bridges and railways, and includes hospitals, aged care facilities, and other health assets. There is a very good chance that unless the housing market completely collapses then increased infrastructure investment will absorb most of the economic impact of the housing downturn.

The biggest problem holding back the economy is the fact, even though employment is rising, wages and spending are not. That is not going to reverse overnight.

Government as the decider

But step-by-step, the Federal Government is making tough decisions in a number of key areas. You may not agree with the decisions, but at least they are decisions.

In superannuation, again, a series of decisions have been made. In education, a whole new matrix of government support has been announced that at least provides some certainty in a key industry. In health, the government is actively trying to stop the rapid fall in private health insurance which threatens the hospital and medical industries — it may not work, but at least it is a carefully considered decision.

And then in energy, the government has developed a policy that has a real chance of working because the emphasis has swung from pure environmental issues to help for the community including individuals and businesses. Of course, it may get stalled because of state governments, but because it is very well argued there is a good chance states will agree. And, at least it has passed through the Coalition party room, which is no easy task.

In terms of shares and employment, the fact there is a Federal Government making decisions helps boost inner confidence – even if some of these decisions may prove to be the wrong ones. And, of course, a lower Australian dollar can always help.

The Week in Review

Investment markets and key developments over the past week

- Share markets mostly rose over the last week helped along by continuing good economic data. Eurozone shares were flat though with Spanish shares falling as the Spanish Government looks to me moving towards taking over the Catalan Government. Australian shares are continuing to play catch up after underperforming significantly year to date with utilities, financials, consumer staples, IT, resources and health stocks all seeing good gains over the last week. Bond yields rose in the US and Spain, were flat in Germany and fell in the UK and Australia. Metal prices rose, oil prices were flat and the iron ore price fell and the $A was little changed.

- Given the 30th anniversary of the 1987 share market crash, this note provides a comparison to today: the prior 12 month gains have been far more modest today and valuations are now far more reasonable once lower inflation and bond yields are allowed for. All of which suggests the circumstances are very different now. The 1987 crash was also a bit of an oddity because it was unrelated to any economic downturn at the time or afterwards. While it may have been triggered by rising inflation and tightening monetary conditions in the US, its severity owed much to 'portfolio insurance' which saw declines trigger more selling and further declines. While circuit breakers introduced after the 1987 crash are designed to limit vertical falls the growth of high frequency trading, ETFs and possibly investment programs driven by artificial intelligence all mean that we can’t rule out another crash like 1987 at some point. At the end of the day though we also have to bear in mind that crashes and bear markets are part and parcel of share investing and ultimately the price we pay for higher long term returns from the asset class compared to say bank deposits.

- Chinese President Xi Jinping’s opening address at the Communist Party Congress referred to “a new era of socialism with Chinese characteristics”. However, it sounded more likely a continuation of the recent direction in policy rather than a big shift in direction. More focus on quality growth, less on growth for growth’s sake, ongoing reform and more emphasis on pollution and equality (both global themes). While there may be less emphasis on growth targets the objective to double 2010 GDP by 2020 implies GDP growth of 6-6.5% pa. So expect growth to remain solid, albeit we may see a bit of fine tuning towards more economic reform.

- Progress continues – albeit in fits and starts – towards tax reform in the US with the Senate close to passing a budget (with a 2018 budget necessary to allow tax reform under the budget reconciliation process as it would allow Republicans to pass tax reform in the Senate with 51 votes as opposed to requiring 60). The House will need to adopt the Senate’s budget which is likely. The main risks relate to the Republicans’ making sure they lose no more than 2 senators in terms of support for tax reform (as it would still pass with Vice President Pence’s vote) - an Alabama Senate special election presents some risk on this front as it shows the GOP and Democrat candidates tied (in Alabama of all places! – not so good for Trump). We remain of the view that tax reform or tax cuts will get up (with a 60 per cent or so probability). The poor performance of high tax paying companies suggest that tax reform is not priced into US shares.

- While the first round of NAFTA talks have ended with no agreement and Mexico and Canada seemingly at loggerheads with a now protectionist US, the fear that the US will just withdraw has been eased by an extension of the talks into next year. So it looks like the US would still prefer a deal. So trade wars still yet to happen under Trump. Our base case remains some sort deal will be reached.

- While some have interpreted the Austrian election (where the far right Freedom Party saw support rise to around 26 per cent and likely to be a junior partner in a government with the centre right People’s Party) as another threat to Europe, I wouldn’t read too much into it. The centre left Social Democrats did better than expected, Austria has already taken a harder line on immigration, Austria has been here before with the Freedom Party (in 1999) and the Freedom Party dropped its anti-Euro stance. So yes Austria may slow European integration but there is nothing in the election outcome suggesting a new threat to the Euro.

- New Zealand has a new coalition Government with NZ First agreeing to support Labour and the Greens. The risk is that it will take a bit of a populist bent in contrast to the rationalist National Party Government it replaces, reflecting similar pressures to those seen in recent elections in the UK, US and Australia, putting downwards pressure on the $NZ.

- The Australian Government unveiled its long awaited energy policy with a focus on both reliability and emissions reduction. This is designed as a way out of the surge in prices that has occurred in response to gas shortages, unsettled climate change policy and a surge in intermittent renewable power without storage. Although I am a bit unsure as to why it should necessarily drive lower prices, the dual focus does make sense. It still must pass Federal parliament though (with bilateral support essential if industry is to take it seriously) and needs state agreement. So a way to go yet.

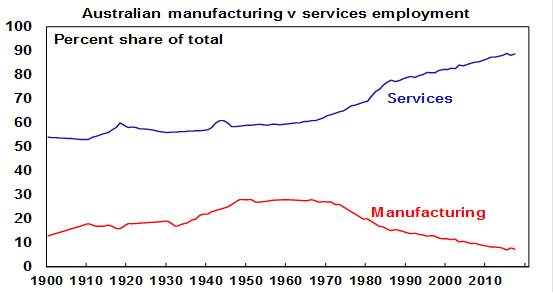

- The last Holden – a sad day, but hard to see a significant macro-economic impact. October 20 is the end of the road for mass car production in Australia with the last Holden rolling of the line at Elizabeth in South Australia. I grew up in a Holden family and my best friend’s family had Fords. I always thought that if we want an Australian car industry we should not rely on government protection as it will just result in museum pieces but rather we should put our money where our mouth is and buy Australian cars. Which I have done - being so impressed by the style, quality and value for money of Australian made cars since the mid-1990s that I have bought four of them - first a pleasant trip to the dark side with a Ford and then three Holdens, including one of the last to be made which I got in June. But it’s clear that not enough Australians agreed and opted for foreign-made SUVs instead. So it’s a rather sad day for me, and more significantly the 950-odd workers in Elizabeth and all those who worked in or around the Australian car industry (maybe around 15,000 workers in total). But putting my rational economist hat back on it would be wrong to exaggerate the negative implications of this for Australia. Car plant closures are certainly a big negative for the affected, but the industry has been shedding workers for years as automation took over and market share fell. Holden recently sent me a photo of my new car on the production line and I could see robotic arms but no people. More broadly, manufacturing employment has been in steady decline since the 1960s (when it was around 25 per cent of the workforce) to now below 10 per cent. Growth in services jobs has, and will continue to, make up for the loss. The loss of say, 15,000 auto industry jobs, also compares to 20,000 new jobs in Australia in September and 372,000 over the last year. It’s still a sad day though.

Major global economic events and implications

- US data remains solid. While housing starts and permits remained depressed by the hurricanes in September a bounce back in the home builders’ conditions index points to a rebound this month. And the lowest level in jobless claims since 1973 and strong regional manufacturing conditions index readings for October point to strong underlying economic growth. With US Federal Reserve chair Janet Yellen expressing ongoing confidence that inflation will rise, the Fed remains on track for another hike in December (with the money market seeing a 77 per cent probability) and likely another three hikes next year (whether its Powell or Taylor or whoever appointed to be the next Fed Chair). Meanwhile, although consensus profit growth expectations for September quarter earnings growth are relatively subdued at 4.3 per cent year-on-year (weighed down by insurers after the hurricanes), results to date have been solid with 81 per cent of results beating on earnings and 79 per cent beating on sales. That said, only 79 of the companies listed on the S&P 500 have reported so far.

- Chinese economic activity data for September provided no surprises with a fractional slowing in GDP growth to 6.8 per cent year on year, slight lifts in growth in retail sales and industrial production but a slight fall in investment growth. It basically tells us that Chinese growth has stabilised at a solid rate. Monetary policy will not be eased much going forward but nor will it be tightened. Rather it remains a case of continued fine tuning with maybe a bit more post Congress emphasis on reform, bringing credit growth under control and more property cooling measures but only to the extent growth remains solid.

Australian economic events and implications

- Australian jobs data surprised on the upside yet again in September with annual jobs growth of 3.1 per cent. That's the highest level since 2008. Unemployment is continuing to trend down. Our jobs leading indicator remains strong pointing to continued solid jobs growth. This is all good news and should lead to faster wages growth eventually – but the US experience (with still low wages growth despite 4.2 per cent unemployment) along with ongoing high levels of job insecurity suggests we may have a way to go yet. So while the strong jobs data taken in isolation points to the risk of an earlier than expected RBA rate hike, the ongoing weakness in wages growth along with risks around the consumer and the still high $A argue against a near-term rate hike. On this front the latest RBA minutes add little that is new but the central bank did reiterate there is no mechanical link between higher interest rates overseas and Australian interest rates, with domestic economic conditions being the key driver of local interest rates. Out of interest: looked at Tasmania lately? – its unemployment rate has fallen below that of Queensland!

Investor Signposts

Inflation in focus

- Inflation readings dominate in Australia in the coming week. The Consumer Price Index is issued on Wednesday with trade prices (exports and imports) on Thursday and business inflation – producer prices – to be released on Friday.

- But the week kicks off on Monday with CommSec releasing its quarterly assessment of economic performance across the Australian states and territories – the State of States report.

- Also on Monday, the Australian Bureau of Statistics (ABS) releases a host of Census results including employment, providing a check on the accuracy of the monthly labour market surveys.

- On Tuesday, ANZ and Roy Morgan also release the weekly survey of consumer sentiment.

- On Wednesday the ABS releases the much-anticipated inflation report for the September quarter. The headline consumer price index is forecast to increase by 0.7 per cent to be up 1.8 per cent on the year due to increasing power and gas bills and housing and tobacco prices.

- The key underlying or ‘core’ measure of prices (excluding volatile components such as energy and food prices) is forecast to rise by 0.5 per cent. As a result, annual growth may struggle higher from 1.8 per cent to 2 per cent.

- On Thursday the ABS’ trade price indexes for the September quarter are released. Base metals posted hefty gains in the quarter with gold also higher. The general recovery in hard commodity prices continues to support Australia’s export-orientated sectors. In terms of import prices, there was a sharp 12 per cent rise in crude oil prices in the quarter in response to OPEC production restraint.

- The data on import and export prices provides an early guide to the terms of trade during the quarter. After a 6 per cent fall in the June quarter, some rebound in the measure of income is tipped in the September quarter.

- Also on Thursday the Reserve Bank Deputy Governor, Guy Debelle, delivers a speech entitled ‘Uncertainty’ at the Warren Hogan Memorial Lecture in Sydney.

- On Friday, data on producer prices for the September quarter are released. Prices of manufactured goods and services in Australia have remained subdued this year, despite the pick-up in business conditions. Final product prices may have risen 0.5 per cent in the quarter and 1.7 per cent over the year.

Overseas: US inflation and economic growth in focus

- There is a packed schedule of economic data releases in the coming week including data on US GDP growth, inflation and housing activity, as well as Chinese house price data.

- The week kicks off on Monday with the release of China house prices data for September.

- On Tuesday in the US is the closely-watched Richmond Federal Reserve manufacturing survey.

- Also on Tuesday across the US, Japan and Europe “flash” readings on manufacturing activity are issued in the shape of the Markit Purchasing Managers indexes (PMIs).

- On Wednesday there is a gamut of economic indicators released in the US with data on new home sales, durable goods orders and the Federal Housing Finance Agency (FHFA) measure of home prices.

- Durable goods – a measure of business investment – may have lifted 1 per cent in September reflecting solid momentum in the US manufacturing sector.

- New home sales are expected to decline to 550,000 in September from 560,000 in August. The FHFA house price index has increased by 6.3 per cent over the year to July, supported by low mortgage rates and strong jobs growth.

- On Thursday, the usual weekly gauge on the job market – new claims for unemployment insurance (or jobless claims) – will be issued together with data on pending home sales.

- On Friday, the first estimate of economic growth (GDP) is released for the September quarter. Growth is expected to moderate to 2.5 per cent due to hurricane-related factors after 3.1 per cent growth in the June quarter.

- Also on Friday, the US Federal Reserve’s key measure of inflation – the core personal consumption deflator for the September quarter – will also be announced. The final estimate for US consumer sentiment in October will also be released on Friday.

Financial markets

- The US earnings season is underway and more ‘household names’ will be reporting results over the coming week. On Monday, Halliburton is due to report.

- On Tuesday, AT&T, Caterpillar, General Motors and McDonald’s report earnings. On Wednesday, Coca Cola and Boeing are amongst those to issue results.

- On Thursday, Amazon, American Airlines, Expedia, Ford, Microsoft and Twitter will issue profit data. And on Friday, Chevron, Colgate-Palmolive, Exxon Mobil and Goodyear are amongst those that plan to issue earnings figures.

Readings & Viewings

We knew it was coming. In fact, we’ve had 30 years to prepare. The anniversary of the 1987 stock market crash passed on Thursday, with Wall Street hitting a new record high. So are we all safe from another market disaster? US Treasury Secretary Steven Munchin, speaking on the eve of the 30th anniversary of the 1987 market crash, predicted stocks will plunge if Congress fails to overhaul taxes.

On the dawn of a film about Tulip mania, historians are claiming the first real market bubble never really happened.

Who’s king of the billionaires’ castle? The clue. He’s been there for 24 straight years, and now has $US89 billion. Forbes has just published its latest list of the 400 richest Americans, who collectively have a net worth of $US2.7 trillion.

He could buy this £17 million mansion with spare change. Or maybe not; it's for sale by bitcoin appointment only.

It's out of reach for almost everybody anyway. Half of the UK population are financially vulnerable with one in six people unable to cope with a £50 increase in monthly bills, according to a survey of Britain’s personal finances by the City regulator.

UK banks may have been used to launder money stolen from South Africa, a former cabinet minister has alleged in a letter to Chancellor Philip Hammond. Times are tough, just look at the crunch on casino profits in the region.

Things could be shaky on the home front. Airbnb’s rival has just scored a pretty sizeable investment, and others are going all in for a Netflix kill.

"The only thing I am comfortable saying is they will all go out of business, all disappear within 50 years" - a New York University academic adds fuel to the fire, and tech market rally, that's been flaming around Amazon, Apple, Google and Facebook.

No mention of Telsa and the Musk family there though. Maybe Elon Musk's brother, Kimbal, will win big with his big bet on container farming.

And Walmart is nipping at the seams of Amazon again, potentially launching an online department store. Toronto has offered to lend a hand and give Amazon stability.

Meanwhile, the UK government's Public Accounts Committee has alleged Amazon, eBay and other online marketplaces have facilitated VAT fraud.

In business, it seems those who fail to adapt to change risk being left behind, or worse. Which is why oil giant Shell this week announced it was embracing electric charging units at its UK petrol station outlets. Expect them in Australian stations in the not too distant future.

Just a hop and a skip over the Pacific, New Zealand’s top court has ruled in favour of 75 international investors, mainly from Singapore, over the return of $NZ8 million in deposits after the developer went bust.

Because of our compromised attention spans, we now actually have ‘more’ hours in a day — 31 hours, experts reckon.

It's a technicality. But speaking to the difference a small change can make, a Canadian man is suing Sunwing Airlines after he was promised champagne service and was instead served sparkling wine.

And while we don't like to run around the rumour mill, does Melania Trump have a body double? It certainly wouldn't be the weirdest thing about this family.