Why house prices will keep surging

It's been confirmed! Far from slowing, the property market is accelerating, and that's despite the considerable jawboning efforts of the Reserve Bank of Australia.

The actual result is a little lower than what RP Data's daily index implied, but it's still impressive. Taking that result, it looks as though house prices surged an annualised 11.4% in the second-half of 2014, a marked pick-up from the 6.6% rate we saw in the first half of 2014.

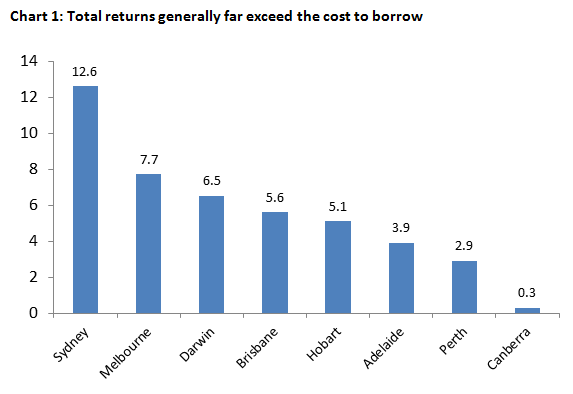

Now, while it's probably true to say that there is a sizeable difference in performance between the major capital cities, it's not all that helpful to obsess about that. As chart 1 shows, total returns, outside of Canberra perhaps, are very attractive relative to the cost of debt. I mean you can borrow at less than 5%, and while property prices in, say Perth, may not be going gangbusters – down 0.1% in the month and only 3.4% higher annually – your total return (which includes rent) is still nearly 3% above what you pay to borrow. That's the benefit of a 4.2% rental yield. You can't even get that on a bank deposit!

Looking elsewhere, the spread of your total return to borrowing costs (i.e. the difference between what it costs to borrow and the return you get on that from property) is much more favourable and rises to 12.6% in Sydney. This is important, because left unchecked house price inflation creates its own momentum. That's especially the case when:

- Interest rates are on hold and;

- Household debt servicing is low – the lowest in about a decade.

Low debt servicing means that households can take on more debt -- there is no point in highlighting record debt levels when the cost of servicing that debt is so low. It's meaningless.]

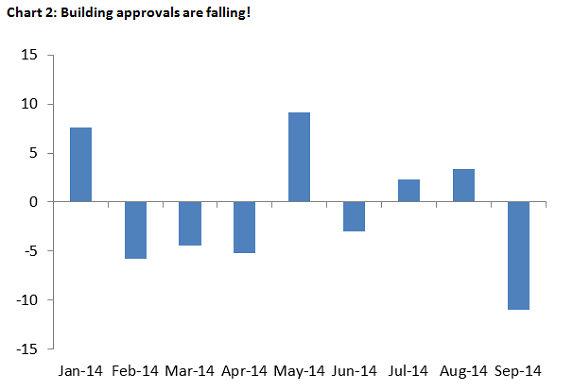

At the same time all that's happened, there is another concerning development. Building approvals have slumped. Numbers released by the ABS show approvals fell 11% in September, which is the biggest fall in over two years. Ok, the numbers are lumpy and the 11% fall we saw in September follows two months of gains – around 5.6% on a cumulative basis.

Yet over 2014 so far, approvals have declined, on average, by 0.8% per month. Don't forget that this is a market that the RBA's Head of Financial Stability [Luci Ellis] described as being a long way from excess (in building) -- a long way. Yet the approvals numbers suggest housing construction is already set to ease.

That's not a trend we can put down to volatility, notwithstanding the fact that the 11% fall was driven by a 22% drop in approvals for apartments. That may correct next month, but even if it does it's unlikely to change the direction approvals are heading. Even prior to the September result it was clear that approvals for apartments were waning: with an average lift of only 0.5% per month, down sharply from 3.6% growth we saw in 2013.

For detached housing the results are even worse. Approvals here have declined in three of the last four months (six of the last nine) -- for an average fall of 0.7% per month. There is a clear downtrend in place here, with approvals for this component down nearly 5% from a peak in January.

On that basis, I think it's a little flippant to regard housing as an ‘irrational obsession'. On current policy it is entirely reasonable for would-be owner-occupiers to be concerned about missing out -- while for investors, the math is obvious. There is a clear failure of policy here -- interest rates are at their lowest in a generation and we're still not building enough houses. Worse, what construction activity we have seen is already showing signs of slowing. Indeed, the only success policymakers seem to have had in trying to jawbone the investor market is to spook developers.

For would-be owner-occupiers there is only one thing to consider. In Sydney and Melbourne, you're going backwards waiting for the housing market to crash in the hope of buying in at cheaper levels.

You need to save $88,000 per year in Sydney just to keep up. In Melbourne, that's about $50,000. Yet, in both cases, that's well above the capacity of most. The average annual wage is roughly $75,000. While the other capital cities appear to be lagging somewhat at this point, it's only a matter of time before they catch up (in terms of price growth).

Debt servicing is low, debt levels are low for most households, and the labour market is improving. Relative value ensures that investors will soon cast their gaze to the other capitals.