Why banks are still attractive

Summary: Bank share prices have failed to lift this year despite attractive dividends. Lingering question marks for the sector include whether the FSI will recommend banks hold more capital, how far the Australian dollar will fall and what impact competition from new payments systems will have. But these concerns distract from positive fundamentals for lending. |

Key take-out: Our banks certainly face challenges but to the retail investor they offer very good value and a fantastic yield. |

Key beneficiaries: General investors. Category: Bank shares. |

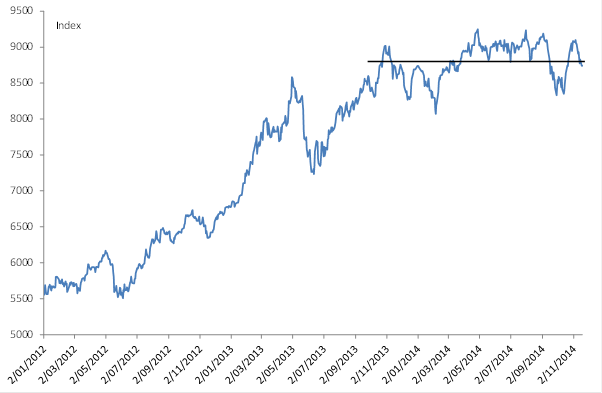

Bank stocks, having just recovered from a rout in September, again appear to have fallen out of favour. Over the last couple of weeks the bank index is down about 4%, with little to suggest at the time of writing that this momentum was set to wane.

Chart 1: Banks losing their appeal?

On a broader time frame, banks have done nothing over the last year in terms of capital gain, and the only way to have made money on them was to buy on the dips. On an accumulation basis you're doing better with a 7% gain over the last year and if you've topped up on dips, then you haven't done too badly at all with a 14.1% gain since the February lows (accumulation) or a 7% gain from the mid-October low.

It's not that banks aren't making money – KPMG highlights that in 2014, the banks made record profits of $28 billion, cash profits up 5.7% from 2013. Indeed on UBS figures, underlying earnings look even more impressive, rising 9.7% over the year, which is the strongest growth since 2010.

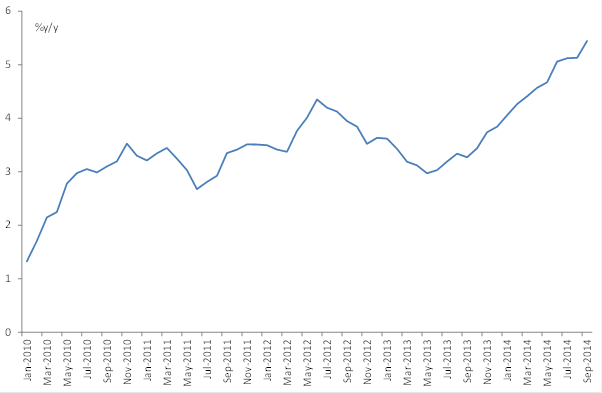

This is a point I've repeatedly highlighted. With the credit cycle turning, even if slowly, bank profits were on the up – and the cycle is turning. Total credit growth is 5.4% higher over the year which is the best growth in about five years. However, this is still about half the historical average, and three to five times below peak rates, which suggests this credit cycle still has some way to run as well.

Chart 2: System credit growth is rising

I'd suggest now that the credit cycle has turned and is accelerating, that profits are on the up and putting in an impressive performance, which suggests that banks are now offering value – indeed I would say firm value. So for instance on a one-year forward earnings basis, banks are currently at a P/E of about 13.4 which compares favourably to the historical trailing average of about 14.4.

Remember that in an environment where cash is at 2.5% and bond yields aren't much above, it wouldn't be out of order to see that P/E trading closer to previous peaks – which is about 19. Banks do after all pay a grossed up dividend yield of over 8%. On that basis our banks are very cheap and on paper should be very attractive to investors.

So what's the problem? Why have stock prices failed to lift this year?

The problem is that there are lingering question marks hanging over the sector and brokers, investment banks et cetera are very quick to talk prospects down. There are several issues of particular concern:

First, when it reports this month, the David Murray-chaired Financial System Inquiry is widely expected to recommend that banks raise capital. There are disparate views as to what that would actually mean for investors though. Some suggest that any move to lift capital adequacy would lead to higher interest rates or lower profit margins – or both. Others suggest that the move would mean little – largely because any lift would be gradual and phased over many years – allowing plenty of time for banks to meet the higher requirements. This is what happened when Basel III was introduced and banks have largely met these requirements without raising rates or lowering dividends. Moreover, and as we learned this reporting season, there has been little adverse impact – certainly nothing noticeable on profits. The uncertainty weighs though.

Then of course there are concerns over competition provided by new payments systems and peer-to-peer lending. Not to mention the negative publicity surrounding ANZ-linked Timbercorp and CBA's problems with a rogue financial planning unit. It is interesting also to note the Senate may well disallow recent attempts to roll back the Future of Financial Advice reforms if it has its way in the coming days.

Not to be forgotten are the concerns held by foreign investors. Primarily that includes the issue of the weakening exchange rate. There is a concerted effort by policy makers to lower the Australian dollar, which of course exposes foreign investors to a significant amount of foreign exchange risk. Remember we're not talking about 5% or so at the margin. We have very loud calls for a further 14% to be lopped off the currency. That's a lot in the way of losses if you're a foreign investor. All the other news flow doesn't help either – talk of recession, or of a housing bubble.

So as far as investors, domestic or foreign are concerned, there isn't a lot of positive news flow on our banks at the moment. All of these concerns weigh and distract from what are otherwise very positive fundamentals for lending in this country.

The bottom line? Our banks are challenged, certainly, but to the retail investor they offer very good value and a fantastic yield. Investors will have to be patient though and learn to look through the temporarily negative news flow and incessant calls to sell them, when investment banks and brokers want to pick them up on the cheap.