Weekend Economist: Crude figures

The Reserve Bank of Australia board meets next week on February 3. Since we changed our view on December 4 last year we have consistently argued that the board will decide to cut the cash rate by 25 basis points at this February meeting. In the discussion below we set out the reasons why we have retained that view.

In last week's note we highlighted the relevance of the December quarter inflation report as an important input to the policy decision. The report showed a slightly higher quarterly print on both headline and underlying inflation.

We expected 0.1 per cent on the headline and 0.6 per cent on the underlying measure (the average of the two core inflation measures, the 'trimmed mean' and 'weighted median'). In the event they printed 0.2 per cent and 0.66 per cent respectively. That is not enough of a difference to change our view around the likely downward revisions to the inflation outlook which the bank will release on February 6 in its quarterly statement on monetary policy (SoMP).

As we anticipated, annual headline inflation still eased back sharply from 2.3 per cent in September to 1.7 per cent in December. Similarly annual underlying inflation eased back from 2.5 per cent in September to 2.2 per cent in December.

This means that the bank is likely to significantly revise down its inflation forecasts.

Recall that the bank's last set of forecasts in November were based around a crude oil price of $US86/bbl (Brent) compared to the current price of $US49/bbl. That fall in the oil price has markedly affected the print for the December quarter CPI and expectations for the March quarter CPI.

In November the bank forecast underlying inflation for the year to June 2015 at 2.5 per cent and 2.75 per cent for the year to December 2015. We expect those forecasts will now be cut to 2.25 per cent and 2.25 per cent respectively. The lower core measures will incorporate a markedly weaker growth outlook (see below) which will further increase Australia's negative output gap – recall that Australia's growth has been below trend for six of the past seven years and that 2015 is expected to be another below trend year for growth, putting further downward pressure on core inflation.

The indirect effect of lower fuel prices on components such as holiday travel, and on the cost bases of companies, particularly with respect to transport costs, will also impact the RBA's core inflation forecasts. Most importantly it should be reasonable for the bank to assume a lowering of inflationary expectations which will also impact on its core inflation forecasts.

This expected lowering in the RBA's core inflation forecasts for 2015 means that the bank would be changing its inflation narrative from expecting a move to the top half of the target band to prospects of remaining in the bottom half of the band – a significant turnaround.

We also expect the bank to lower its growth forecasts in the February SoMP. The bank is likely to adjust its forecasts for the soft spot in activity that it did not anticipate in its November forecasts, and to include the ongoing drag from the terms of trade on nominal incomes. These negatives will dominate any positive effects from lower fuel prices and a lower Australian dollar.

It is reasonable to assume that having moved through that negative shock the economy will take more time to build momentum. That would see the soft momentum we saw in the September quarter extend through the December quarter and into the March quarter of 2015 with the expected lift nearer the end of the year taking longer to come through.

This expected delay is likely to see growth rates revised down from 2.5 per cent (2014); 3 per cent (2015); and 3.5 per cent (2016) – which were the November forecasts – to 2.25 per cent (2014); 2.5 per cent (2015) and 3 per cent (2016) in the February SoMP. That is, a 0.5 per cent cut across the entire forecast period. This would be a material change and, accordingly, as with the lower inflation forecasts, justifies, indeed demands, a policy response.

Last week I noted that a feasible barrier to cutting rates was the low probability given to such a move by the market. The RBA does not have a history of surprising markets. Market pricing at the time gave only a 25 per cent probability to the cut. That has now lifted to a 'respectable' 65 per cent; indeed, arguably a level that would pressure the bank to explain itself if it chose not to move.

That 'surprise aversion' argument may not be as strong a reason as in the past We have seen a stream of central banks surprise markets with dovish policy moves: India; Canada; Denmark; and Singapore. Even the doggedly hawkish Reserve Bank of New Zealand raised the possibility of cutting rates in its latest Statement.

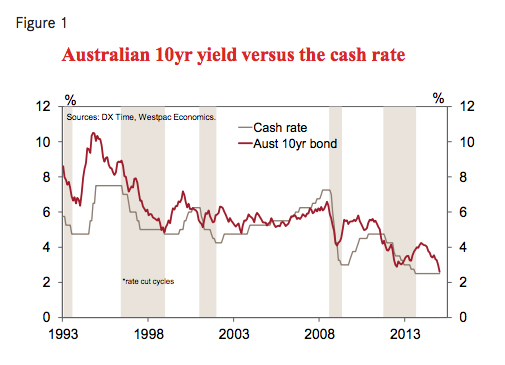

Finally we have the signal from the yield curve. Figure 1 shows that the past four easing cycles have all been coincided with the 10 year bond rate moving close to the overnight cash rate. Long bond rates around the cash rate indicate that policy is unnecessarily tight.

Central banks could argue that in the era of QE the bond rate is not sending reliable signals about the outlook for growth and inflation although that would be a risky approach given the time honoured reliability of the yield curve shapes in that regard.

In conclusion, we remain comfortable with our view that the bank will cut rates by 25 basis points next week.

Bill Evans is chief economist with Westpac.