Week in Review: June 29, 2018

A strong year, but tensions are high.

Investment markets and key developments over the past week

- The past week saw geopolitical concerns around trade, and particularly the US-China relationship, continue to dominate investment markets. This saw most share markets fall, with the Chinese share market falling particularly sharply, but the Australian share market held up pretty well with higher oil prices boosting energy stocks. Bond yields continued to fall on the back of safe haven demand, except in Italy. Commodity prices were mixed with oil continuing to move higher after OPEC's decision to raise production by less than feared, iron ore prices little changed but metal prices down. The US dollar continued to move higher and the $A rose slightly.

- Another strong financial year for investors. While the December half year was strong as global share markets moved to factor in stronger global growth and profits helped by US tax cuts, the last six months have been messy for investors – with US inflation and Fed worries, trade war fears, uncertainty around Italy, renewed China and emerging market worries and falling home prices and the Royal Commission in Australia. Despite this the 2017-18 financial year has seen pretty solid returns for well diversified investors. Global shares look to have returned around 14 per cent in Australian dollar terms, Australian shares returned around 13 per cent (including dividends) and unlisted assets have continued to see double digit returns. While bond and cash returns have been more constrained this still points to balanced growth superannuation returns of around 9 per cent for the financial year which is pretty good given inflation of around 2 per cent. We expect returns to slow a bit over the new financial year but they should still be reasonable as the global and Australian economies are likely to keep growing and this will help profit growth at a time that monetary policy still remains easy. However, global inflation, Fed tightening and trade war fears are the main risks and they will help keep volatility high.

- US trade related tensions with China remain high. President Trump's decision to support a strengthening of the Committee on Foreign Investment in the US (CFIUS) process so it can prevent foreign investors from violating US intellectual property rights, rather than declaring an economic emergency in relation to Chinese investments under the International Emergency Economic Powers Act (IEEPA) is less provocative towards China than had been feared. But ultimately the proof will be in the pudding and in the meantime, there is still no sign of the US and China restarting trade negotiations ahead of the July 6 start date for tariffs on $US34bn of Chinese imports. So, it's looking very likely that the first round of tariffs will be implemented. Our base case remains that some form of negotiated solution will be reached but things are likely to get worse before they get better.

- The European leaders summit looks to be seeing ongoing plodding towards greater Eurozone economic integration and an agreement on an EU wide “Australian” solution to its migration problem focussed on beefed up external border security (stopping the boats) and holding centres (possibly offshore) to process immigrants. The progress on immigration looks to be enough to keep Italy onside and probably to keep Merkel's coalition government in Germany together for now. All of which is a positive for Eurozone assets, albeit the Italian budget issues remain for the months ahead.

- What's up with Chinese shares and the Renminbi? Is it a bad sign for global growth? From its high in January the Chinese share market has fallen around 22 per cent and the Renminbi has fallen around 6 per cent from its April high. These sort of moves are naturally inviting comparisons to the 2015-16 plunge in Chinese assets. The weakness has been triggered by signs of slowing growth in China, worries that this will be made worse by a trade war with the US and with the shift to Chinese monetary easing weighing on the Renminbi. However, it's very different to 2015 when Chinese shares plunged nearly 50 per cent (after previously more than doubling in value to a forward PE of around 19 times) amidst an unwinding of margin positions, government moves to support the market and a shift to a new way to manage the currency that led to capital outflows. This time around the share fall started from low double-digit PEs and the PE is now only around 10.5 times, there has been no panicky unwinding of margin positions, economic data is arguably more stable, there is more confidence in how the currency is managed. In fact, the fall in the Renminbi is a mirror image of the rise in the value of the $US which against a basket of currencies is up nearly 8 per cent since April. For these reasons the fall in Chinese shares and the Renminbi is less worrying for the global and Australian economies than it was in 2015-16, which is why Australian shares have not been falling at the same time.

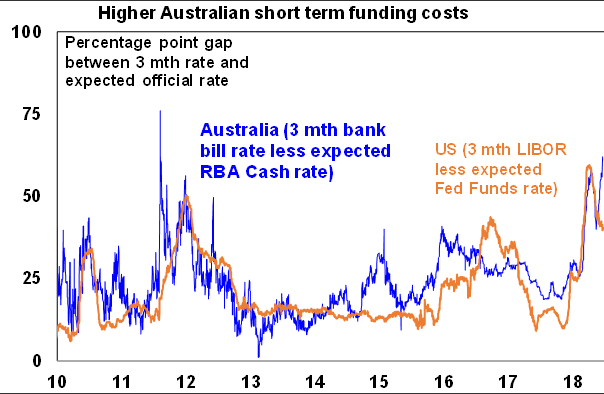

- In Australia, some small banks have raised mortgage rates in response to a blowout in short term funding costs and others may follow. As noted several times in this Weekly Report lately the gap between bank bill rates and the expected RBA cash rate has blown out relative to normal levels (by around 0.35 per cent) in recent months and it was only a matter of time before banks started to pass this on given they get about 20 per cent of their funding from this source (more so for the smaller lenders which have been the only ones to move so far). Initially the blow out was driven by the same thing occurring in the US (which was partly driven by US companies returning cash held overseas in US dollars back to the US) but it has continued in Australia possibly reflecting a desire to lock in funding ahead of the financial year end (after the squeeze into the March quarter end), the Westfield takeover and regulatory reforms including the impact of the Royal Commission.

- However, there are a few things to note. First, the increased cost of funding for banks only amounts to less than 0.1 per cent if it's fully passed on to all rates so it's small. Second, banks so far seem to be focussing the pass through on rates other than traditional owner occupiers on principle and interest loans – given the desire to avoid more adverse publicity - which will reduce the impact on households. Big banks which are yet to move, but likely, will are expected to do the same. Finally, it's not a sign that the RBA has suddenly lost control – apart from the small nature of the rise banks have been doing out of cycle moves for a decade now and yet the main driver of the big picture trend in rates remains what the RBA does…and right now they aren't doing anything. So don't expect big changes in traditional mortgage rates. What the latest mortgage rate hikes do though is provide a reminder to households (if one is needed) that rates can go up and at the margin along with tightening bank lending standards they make it even less likely that the RBA will hike rates anytime soon.

Major global economic events and implications

- US economic data was mostly strong. Regional business surveys mostly rose in June, pending home sales fell but new home sales surged and home prices continue to rise, core capital goods orders slipped in May but were revised to be very strong in April pointing to a strong quarterly gain in capex, jobless claims remain very low and consumer confidence slipped in June but remains around as high as it ever gets.

- Eurozone economic sentiment fell only marginally in June with business sentiment actually stabilising and overall sentiment remaining strong. Meanwhile money supply and credit growth picked up a bit in May.

- Japanese data was a bit better than expected with the jobs market remaining very strong (helped by a falling population of course), industrial production falling less than expected and core inflation in Tokyo rising to 0.4 per cent year on year in June…albeit that's still way below target so the BoJ will remain pedal to the metal.

- China's central bank delivered the foreshadowed further cut to bank required reserve ratios – which looks designed to help bolster the economy as credit from shadow banking slows and given the threat of trade wars. Meanwhile profit growth remained strong in May.

Australian economic events and implications

- Australian data was a bit light on over the last week but job vacancies continued to rise very strongly into May according to the ABS suggesting the labour market remains strong. Meanwhile, credit growth is continuing to slow with lending to investors stalling and the downtrend in new home sales continued in May.

- The ABS should forget about a monthly CPI. It says it's apparently close – maybe for mid-2020. This would be great for economists, market commentators and economics journalists as it will mean more to talk about. But as we all know monthly data just means more noise - that the ABS always encourages us to look though using its trend estimates. Which is just what the RBA will do so it won't make any difference to what happens on monetary policy. But it will mean more volatility in investment markets and more meaningless chatter about what interest rates should do. The ABS should spend the extra resources required to create a monthly CPI on stats with wider economic and social value.

Shane Oliver is the Chief Economist at AMP Capital

Share this article and show your support