Wall Street bull to trot on

- {{x.value}}

{{ twilioFailed ? 'SMS Code Failed to Send…' : 'Enter verification code' }}

{{ completedStep1 ? 'Authentication & Security' : content.trialHeading.replace('{0}', user.FirstName) }}

{{ content.upgradeHeading.replace('{0}', user.FirstName) }}

The email address you entered is registered with InvestSMART

Please login to continue

We have sent you an email with the details of your registration.

Looks you are already a member. Please enter your password to proceed

{{ upgradeCTAText }}

Updating information

Please wait ...

Your membership to InvestSMART Group recently failed to renew.

Please make sure your payment details are up to date to continue your membership.

Having trouble renewing?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

You've recently updated your payment details.

It may take a few minutes to update your subscription details, during this time you will not be able to view locked content.

If you are still having trouble viewing content after 10 minutes, try logging out of your account and logging back in.

Still having trouble viewing content?

Please contact Member Services on support@investsmart.com.au or 1300 880 160

Please click on the ACTIVATE button to activate your Intelligent Investor 15-day free trial

Please click on the ACTIVATE button to finalise your membership

Unsuccessful registration

Registration for this event is available only to Eureka Report members. View our membership page for more information.

Registration for this event is available only to Intelligent Investor members. View our membership page for more information.

- You are already registered for this event.

- This event is already full.

- Please select a quantity for at least one ticket.

- {{ i }}

Forgotten password

Please enter your email address below to request a new password

- Verify your email address by clicking on the link we sent to {{user.Email}}

- You now have free access, we look forward to helping you on your financial journey.

Summary: Ten strategists surveyed by Barron's have predicted gains for the S&P 500 in 2016, but remain concerned about a number of trends in the year ahead – including the effects of interest rate rises, strength of the US dollar, and scarce profit growths across several sectors. Analysts appear measured in their predictions for the coming year, but favour financials and technology for 2016. |

Key take out: Analysts' mean forecast predicts the S&P 500 will finish 2016 at 2200, a 10 per cent increase compared with the closing price of 2012 on December 11 - though they predict many stocks will be negatively affected by a strong US dollar and falling commodity prices. |

Key beneficiaries: General investors. Category: Shares. |

Stay positive about the third-longest bull market on record—but curb your enthusiasm. That's the memo from Wall Street's top investment strategists about the prospects for US stocks in 2016. With the Federal Reserve expected to start raising interest rates as soon as this week, and earnings growth likely to be restrained, the 10 strategists Barron's surveyed this month see moderate gains for the market in the year ahead.

Based on their mean forecast, the Standard & Poor's 500 index will end next year at 2220, an increase of 10 per cent from Friday's close of 2012. An advance of that magnitude is more reflective of the market's rout last week, however, than undue exuberance among our prognosticators. To the contrary, the strategists were more cautious in their comments than in recent years past.

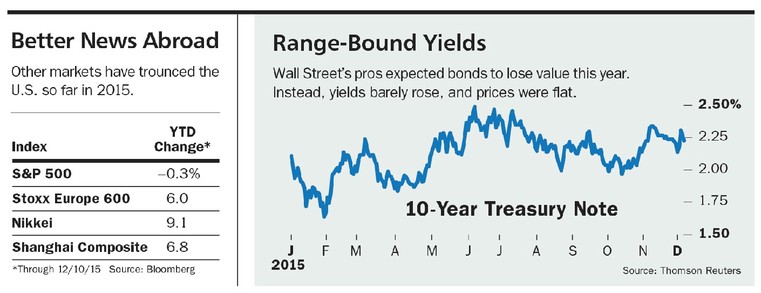

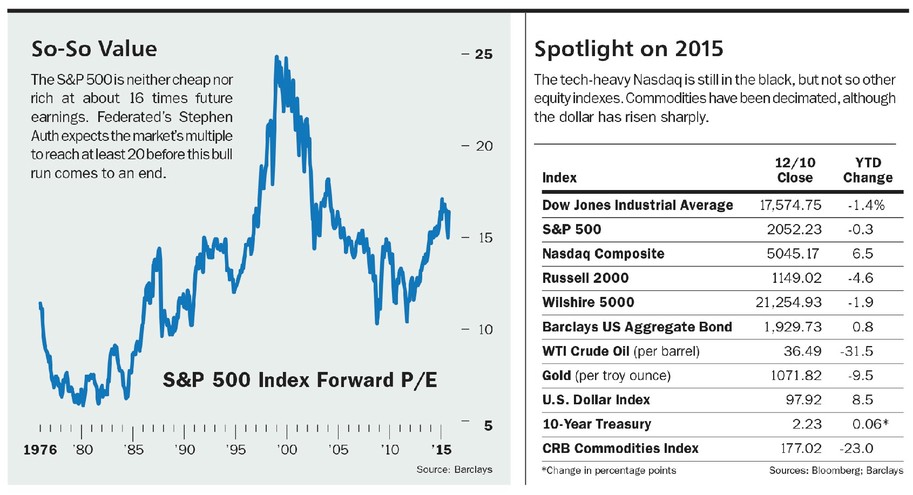

Any advance would be superior to this year's 2.3 per cent loss (through to December 11). A year ago, the pros predicted stocks would rally 10 per cent in 2015; that target seems far-fetched today, with just 13 trading days left in the year.

Barron's surveys a group of prominent market strategists at big banks and major investment firms each September and December, to gauge their outlook for stocks, bonds, and the economy in the months and year ahead. Our latest inquiry came just ahead of this Wednesday's near-certain rate hike, and amid increased market volatility, in a year that has yielded few rewards for investors across multiple asset classes.

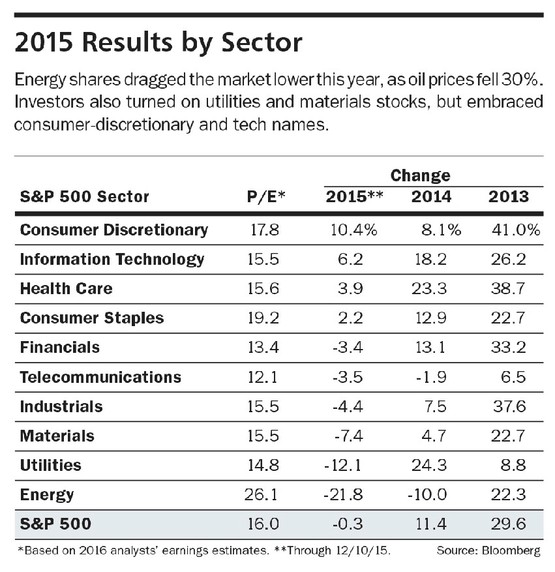

The S&P 500 reached an all-time high of 2131 in May, and the Dow Jones Industrial Average, a peak of 18,321. Stocks suffered a correction of about 12 per cent in August and September—the first in four years—when China took steps to devalue its currency to counter decelerating economic growth. The averages have regained lost ground this fall, but the strategists see few catalysts that could push the market sharply higher, especially with a three-decade slide in interest rates coming to an end. The outlook for energy, metals, and mining shares is particularly bleak, unless and until the bear market in commodities ends.

The strategists' individual year-end targets for the S&P 500 cluster around 2200. Remove the single forecast for a 2500 close—a statistical outlier of sorts—and the group's mean prediction for 2016 falls to 2190.

The Street's seers expect S&P 500 earnings per share to rise just 5 per cent next year, from this year's estimated $118. Their mean forecast for 2016 is $US123.50. Last December, these seers were more upbeat, expecting earnings to climb 8 per cent in 2015. Industry analysts typically are more optimistic than strategists, and that is the case this year, as last. The analysts anticipate S&P earnings of $US128 in 2016, representing an 8.5 per cent increase over current-year targets.

On an aggregate basis, corporate earnings are flat this year, and could turn negative when all of the data are in. Profit gains haven't looked so punk since the bad old days of 2009. Excluding the hard-hit energy sector, S&P earnings could rise 5 per cent to 6 per cent in 2015. Even so, that isn't much to brag about.

The strategists expect earnings growth to be the key driver of stock prices in the new year. Few foresee an expansion of the market's price/earnings multiple, and some think the P/E will contract. The S&P 500 currently trades for 15.7 times analysts' consensus 2016 estimate, on par with a forward P/E of 15.8 a year ago. Stocks aren't cheap; nor are they rich, given a long-term forward P/E of 15 and today's low interest rates.

The strategists' measured view is apparent, as well, in their newly narrow focus on just two industry sectors—financials and technology—that seem poised to outperform in the coming year. Worries about a persistently strong dollar, sluggish global growth, and plunging commodity prices have weakened the attraction of most other sectors.

Wall Street's experts see little likelihood that the US economy will reach “escape velocity” in the months ahead. Instead, they think industry and investors will have to learn to live with relatively meager annualised growth of 2.5 per cent in gross domestic product.

“Investors are more saturnine than sanguine,” compared with 12 months ago, says Adam Parker, head of US equity strategy at Morgan Stanley, who has an S&P 500 index target of 2175 for 2016. The recent correction is fresh in investors' minds, and they are worried the Fed's tightening will cause more volatility, he says.

Tobias Levkovich, chief US equity strategist at Citigroup's Citi Research, notes the presidential election also could produce a “wobbly market” next year. Levkovich has an S&P target of 2200 for 2016.

In many ways, the Fed's final act of 2015 could call stocks' tune all through next year. The US central bank's policy-making committee is widely expected to nudge its federal-funds target rate up this week to 0.25 per cent to 0.50 per cent from a longstanding 0 per cent to 0.25 per cent. The fed-funds rate, or the overnight lending rate that banks charge one another for funds maintained at the Fed, helps shape the short end of the bond-market yield curve.

Although incremental, the move would represent the first step in the normalisation of US interest-rate policy after years of quantitative easing and near-zero rates—policies designed to spur economic growth following the financial crisis of 2008 and the ensuing recession. The strategists expect that the fed-funds rate will climb to 1 per cent to 1.25 per cent by the end of next year, as the Fed follows its first hike with successive increases.

What higher rates might mean for equity valuations is a matter of debate, however. David Kostin, Goldman Sachs' chief US equity strategist, says the market is underestimating the number of rate hikes likely to follow next year. Goldman looks for four increases in 2016, bringing the fed-funds target to 1.25 per cent to 1.5 per cent. If that forecast is right, he says, the market's P/E multiple will contract as others come around to this view.

Kostin expects the S&P to wind up next year at 2100, just 4 per cent above Friday's close; that's the lowest forecast in the group. He thinks the benefit of a decent rise in earnings will be offset by higher interest rates and tepid economic growth. While higher rates present a “clear risk” to equity valuations, they are only a modest threat to corporate profits, he notes.

Jeffrey Knight, head of global asset allocation at Columbia Threadneedle, also thinks that rising rates could lead to a compression of the market's P/E multiple. A 25-basis-point (25 hundredths of a percentage point) increase “isn't terribly significant economically, but it matters as a psychological marker,” he says. “The Fed is saying to the market, ‘You are on your own.' ”

The monetary punch bowl—that is, the combo of Fed asset-buying and ultralow interest rates—has been an important catalyst for higher stock prices, says Knight, who has a 2016 S&P target of 2200. “Even if it is the most gradual removal ever, it matters,” he says.

How does the market perform after the interest-rate cycle turns and rates begin rising anew? Kostin notes that after the initial rate hikes of 1994, 1999, and 2004, the S&P 500 averaged a gain of 6 per cent in the succeeding 12 months. Yet, the forward market multiple contracted by an average of 10 per cent.

History is only a partial guide to current circumstances, however, as the Fed isn't planning to tighten monetary policy so much as “normalise” it after a long period of abnormally puny rates. That distinction might be lost on some investors, says John Praveen, chief investment strategist at Prudential International Investments Advisors.

“It's a very different rate cycle,” adds Russ Koesterich, global chief investment strategist at BlackRock. Of most importance, the current round of policy tightening is likely to end with short-term rates at around 3 per cent, not the 4 per cent or 5 per cent seen in prior cycles, he says. Although the market's P/E is lower than at previous peaks, a reversal of monetary stimulus creates “a world where higher P/E multiples are hard to come by,” he adds.

Koesterich expects the S&P to round out 2016 at 2175.

Stephen Auth, chief investment officer of Federated Investors, was last December's most optimistic forecaster. Although the market failed to cooperate, he remains so today. Auth expects the fed-funds rate to end next year at 1 per cent, after which Fed Chair Janet Yellen and her team will pause. He thinks the Fed eventually will stop at 3 per cent. Yet, unlike Koesterich, he says “lower for longer” means stocks are cheap now.

Although the averages are down slightly this year, the market's resilience in the face of 2015's heavy blows is impressive, Auth says. “Land mines,” including proof of China's slowing economy, plummeting oil prices, a rising dollar, and the coming Fed hike, will “soon be behind us,” he says.

Auth, who has a 2016 S&P target of 2500, says corporate earnings and the market's multiple will both head higher next year, resulting in a big move in the index. He expects the P/E ratio to drift up to 18 from 16, and reach 20 times forward earnings “before this bull market is over.”

Auth believes that S&P earnings growth is “almost built in to increase substantially,” perhaps by 15 per cent or more, due to “solid 2.5 per cent to 3 per cent GDP growth and a dramatic improvement” in the earnings of the decimated energy sector. In the oil patch, heretofore huge declines in earnings, and in many cases, losses, will be rolling out of quarterly comparisons next year. Indeed, without the energy sector, S&P 500 earnings would be up 6 per cent this year, instead of flat to down.

Prudential's Praveen sees earnings growth of 8 per cent, fueled by an expanding economy. He, too, is a longstanding bull, and has an S&P forecast of 2250. But he has pulled in his horns a bit, predicting a slight contraction in the P/E multiple because of impending rate hikes. “Measured and modest” moves in the fed-funds rate will result in similar moves in the S&P 500, he predicts.

Stocks are cheap relative to bonds, Praveen says, citing the earnings yield gap. The earnings yield, the inverse of the P/E ratio, is now 5.9 per cent on a trailing 12 month basis, compared with a yield of 2.14 per cent on the 10 year Treasury bond. The spread, at 3.76 percentage points, has narrowed from roughly four points a year ago, but is still much wider than the 1.2-point average of the past 20 years.

Jonathan Glionna, head of U.S. equity strategy at Barclays Capital, is less exuberant about the market's prospects than many peers. Both Glionna and Goldman's Kostin predicted a year ago that the S&P would end this year around 2100, and are looking pretty prescient.

Although the market's P/E is slightly elevated, it isn't inconsistent with an expansionary environment, Glionna says. But certain other valuation metrics, such as the price-to-sales ratio, suggest the need for caution. The S&P 500 is currently selling for 1.8 times trailing sales, compared with 1.7 times sales a year ago. It has been above 1.5 times for more than a year, but rarely stays there long term. It is no coincidence, he says, that the market has been unable to gain much in the past 12 months.

Glionna, who carries an S&P target of 2200 for 2016, says greater inflation is likely to aid revenue growth next year. At the same time, the dollar's strength could act as a drag. With the Fed lifting interest rates, the dollar could continue to rise against other currencies, albeit at a slower pace than in the year about to pass.

Dubravko Lakos-Bujas, chief US equity strategist at JPMorgan, lists a stronger dollar as one of the biggest risks facing the market next year. A 5 per cent to 6 per cent change in the dollar's trade-weighted average price is roughly equivalent to a 3 per cent change in the S&P 500's earnings per share in the next 12 months, he says.

Even if the dollar doesn't rise another 10 per cent to 11 per cent, as it did in 2015, it will cause erosion in per-share earnings growth through transactional effects, he says. That will prevent the P/E multiple from rerating higher. Lakos-Bujas expects the S&P to rally to 2200 next year.

Wall Street's strategists have long favored technology shares, but financials are first in their hearts for 2016. In large part that's because banks' net interest margins will widen if interest rates rise, while loan growth could improve as the economy grows. Financials are inexpensive compared with other sectors, and are a good hedge against the risk that the Fed raises rates more aggressively than expected, says Lakos-Bujas.

Among financials, Goldman's Kostin likes Visa (ticker: V) because the company's Visa Europe acquisition will help it capture the accelerating shift toward electronic payments on the Continent, and drive up earnings estimates for 2016 and 2017.

Morgan Stanley's Parker prefers Capital One Financial (COF), and says the company could deliver robust credit-card growth with low charge-offs. He is also the lone fan of consumer-discretionary shares, which he says will benefit from rising employment and wages. That should help Ross Stores (ROST), an off-price apparel and home-fashions retailer that Parker expects to reward investors in 2016.

The strategists still like tech stocks, especially as the tech industry continues to offer top-line growth in a world with otherwise muted prospects. Valuations are reasonable, profit margins are high, balance sheets are strong, and the stocks tend to do well in a rising interest-rate environment, Koesterich says.

Avago Technologies (AVGO) is one of Auth's top picks, as the maker of semiconductor chips for wireless devices will be helped by the proliferation of smartphones. Auth is also a fan of health care, which led the market for the past five years until it recently fell out of favor.

The health-care sector offers long-term growth, and investors need to accumulate shares in periods of disfavor, he says. Gilead Sciences (GILD) is one of the strategist's top picks; the company owns the hepatitis C franchise, he says. It has several other promising drugs in its pipeline, and trades for a mere nine times 2016 expected earnings.

Some strategists expect that value stocks, which have underperformed growth stocks for years, could outrun their snazzier cousins next year. Savita Subramanian, head of US equity and quantitative strategy at Bank of America Merrill Lynch, isn't focusing on conventional sector analysis this year, but says investors should favor value stocks generally, as they are on the cusp of being rerated upward. Big-cap dividend growers are especially cheap, she says, citing Walt Disney (DIS), and 3M (MMM).

If a sector doesn't have macroeconomic risk, or business disruptions, or headline risk, it is crowded and expensive, Subramanian says. She prefers picking individual stocks, based on quality, liquidity, valuation, growth, and dividends.

When profit growth is scarce, she notes, growth stocks rule. But, since 1930, annual earnings gains of 5 per cent or more have coincided with outperformance by value stocks. She expects S&P 500 earnings to rise by 5 per cent in 2016, and the index to hit a year-end target of 2200.

As for the coming hike in interest rates, Subramanian calls it “the end of the Fed put,” which was thought to place a floor under stock prices. “There will be no more IV bag for the patient, and the market will get rational” as rates normalise, she says.

The strategists haven't much changed their view of sectors to avoid in the new year. They are still negative on utilities—the stocks are down 12 per cent year to date—and consumer staples stocks, up 2 per cent. Both sectors are defensive and often regarded as bond proxies. The outlook for growth is poor in 2016.

Barring an eleventh hour rally, the year now drawing to a close could go down in the books as one of the most frustrating for investors. If the S&P 500 ends the year in the black, it probably will do so by a slight margin only, owing to gains in a handful of stocks.

Meanwhile, a recent Goldman Sachs report notes that 74 per cent of large-cap core mutual funds are trailing the S&P 500 in 2015. Granted, that is a notable improvement over last year's 85 per cent that lagged behind, but it's nothing to be proud of.

While stocks delivered little in the way of gains, the bears have also taken a shellacking. Several prominent hedge funds reportedly took big hits when stocks they had bet against rose instead of fell. The Morningstar Bear Market Fund category is down about 6 per cent for the year.

“In a cross-section of assets, very little worked this year, whether stocks, bonds, or currencies”—apart from the dollar, Columbia's Knight says.

The bond market stymied strategists and investors, as well. Although most Wall Street strategists called for bonds to lose value in 2015, they look to be ending the year flat.

The yield on the 10-year Treasury bond was 2.17 per cent at the end of 2014. The 10-year sported a yield of 2.14 per cent last week. (Bond prices move inversely to yields.) The US bond market has been supported by global fixed-income investors, who have sold lower-yielding German and Japanese government paper to invest in Treasuries. Demand for Treasuries has helped to push up the dollar.

More than one strategist extolled US stocks as the best asset class in the world, but Knight is troubled by investors who think the only opportunities lie close to home. With the Fed about to raise rates and only a handful of stocks holding the market aloft, “that's a worry,” he says.

Valuations overseas are generally more reasonable, says BlackRock's Koesterich, and foreign central banks have more room to ease. Also, other nations' weak currencies are advantageous for their exporters. The iShares Currency Hedged MSCI EAFE exchange-traded fund (HEFA) is one way to gain exposure to non-US stocks without currency risk. The ETF has edged up 1 per cent this year, and yields 3.8 per cent.

The year ahead will bring many risks, including the risk that political posturing will slam stocks in various sectors. Already, talk of drug-price reductions by certain presidential candidates has hurt health-care stocks. The Street's strategists are less bullish than in several years. Even so, they expect the old bull to trot on.

*This report is republished with permission from Barron's.